Fading cash yields could see a powerful rotation into credit markets, while AI financing and emerging markets could offer new opportunities. BNY Investments' Peter Bentley gives his 6 potential catalysts for credit investments in 2026.

1. Cash into Credit Markets

When cash rates soared, money market funds (MMF) became an attractive investment choice for retail and institutional investors, offering high yields with low risk. Money market fund balances are up by $2.3 trillion since the US Federal Reserve (Fed) began hiking interest rates in early 2022. Now, cash rates are fading – especially in the US – and yield curves are steepening, so we expect investors to move away from cash in search of higher returns elsewhere. That could unleash a wave of liquidity into credit markets.

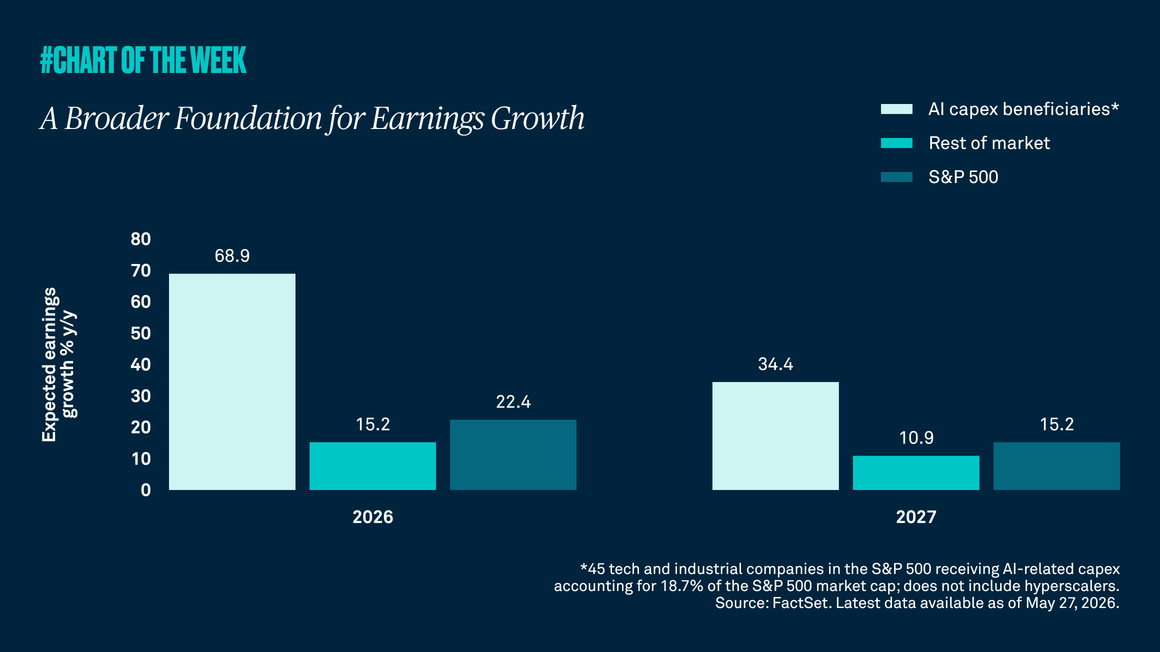

2. The AI Infrastructure Boom Should Keep Growth Positive

US corporate profitability stands at 70-year highs, allowing tech giants to fuel an unprecedented AI-driven spending boom. Even if forecasts are optimistic, the scale of projected spending should remain a significant tailwind for growth in 2026. Together with expected rate cuts, this should keep economic growth in positive territory, though we think it will remain subdued.

3. AI Infrastructure Financing Could Boost Credit Supply

For fixed income investors, the surge in AI spending is a potential opportunity to access attractive, low-risk debt from financially robust issuers. Unlike the dot-com era, many of today’s tech companies have strong balance sheets and diversified revenues. So, they should be resilient even if AI growth disappoints. While increased issuance may temporarily widen credit spreads – especially in the US – we expect demand to remain strong as long as yields remain high. However, as the AI landscape evolves, there will inevitably be winners and losers. This makes rigorous issuer selection critical to fully capture the upside of this opportunity.

4. Global Credit for a Low-Growth Environment

If nominal growth remains comfortably positive, a period of slow growth is not necessarily a problem for credit. It would potentially be a trickier environment for equities because it implies that profit growth will be hard to sustain. However, fixed income does not require faster growth, only the timely repayment of debt. Even modestly positive nominal growth typically provides a supportive environment for credit assets.

5. Eyes on the Emerging Markets

We view the emerging debt outlook positively. Regions like Latin America offer potentially compelling investment opportunities, as companies from emerging markets with strong domestic franchises are largely insulated from global tariff uncertainty.

6. Global Investment Could Be Valuable

We see the potential for significant market divergence in 2026, which could provide investment opportunity for active managers. In Europe, France faces political and fiscal challenges, but elsewhere, the outlook is more constructive, helped by German fiscal stimulus and increased defence spending. Bouts of volatility across various segments of the fixed income universe are almost certain, but they will offer tactical opportunities for those able to respond dynamically to shifting market conditions.

This article is part of our 2026 Outlook series where our financial experts answer 6 key questions facing investors.

The value of investments can fall. Investors may not get back the amount invested. Income from investments may vary and is not guaranteed.

Important Information

For sole and exclusive use by Institutional Investors, Accredited Investors and Professional Investors only. Not for further distribution. This is a financial promotion and is not investment advice. Any views and opinions are those of the investment manager, unless otherwise noted. The value of investment can fall. Investors may not get back the amount invested. BNY, BNY Mellon and Bank of New York Mellon are the corporate brands of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally. BNY Investments encompass BNY Mellon’s affiliated investment management firms and global distribution companies. Any BNY entities mentioned are ultimately owned by The Bank of New York Mellon Corporation. In Hong Kong, the issuer of this document is BNY Mellon Investment Management Hong Kong Limited, which is registered with the Securities and Futures Commission (Central Entity Number: AQI762). In Singapore, this document is issued by BNY Mellon Investment Management Singapore Pte. Limited, Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore (MAS). This advertisement has not been reviewed by the Monetary Authority of Singapore.

MC684-12-01-2026 (6M)