Key takeaways

- The Supreme Court invalidated tariffs under IEEPA but this is not a reset of U.S. trade policy. The Trump administration is imposing global tariffs of 10% with the aim of increasing them to 15%, under non-IEEPA authorities.

- With tariffs being partially reinstated, we would expect a modest boost to growth and a small reduction in inflation.

- We believe that the lower tariff rate would act as a stimulus and be positive for risk assets, creating upside for equities.

What Was the Ruling?

The Supreme Court of the United States (SCOTUS) announced in a 6-3 ruling that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) exceeded the powers of the president. This includes the ‘reciprocal’ tariffs and ‘fentanyl’ tariffs on China, Mexico, and Canada. The decision, issued on February 20, 2026, was widely anticipated.

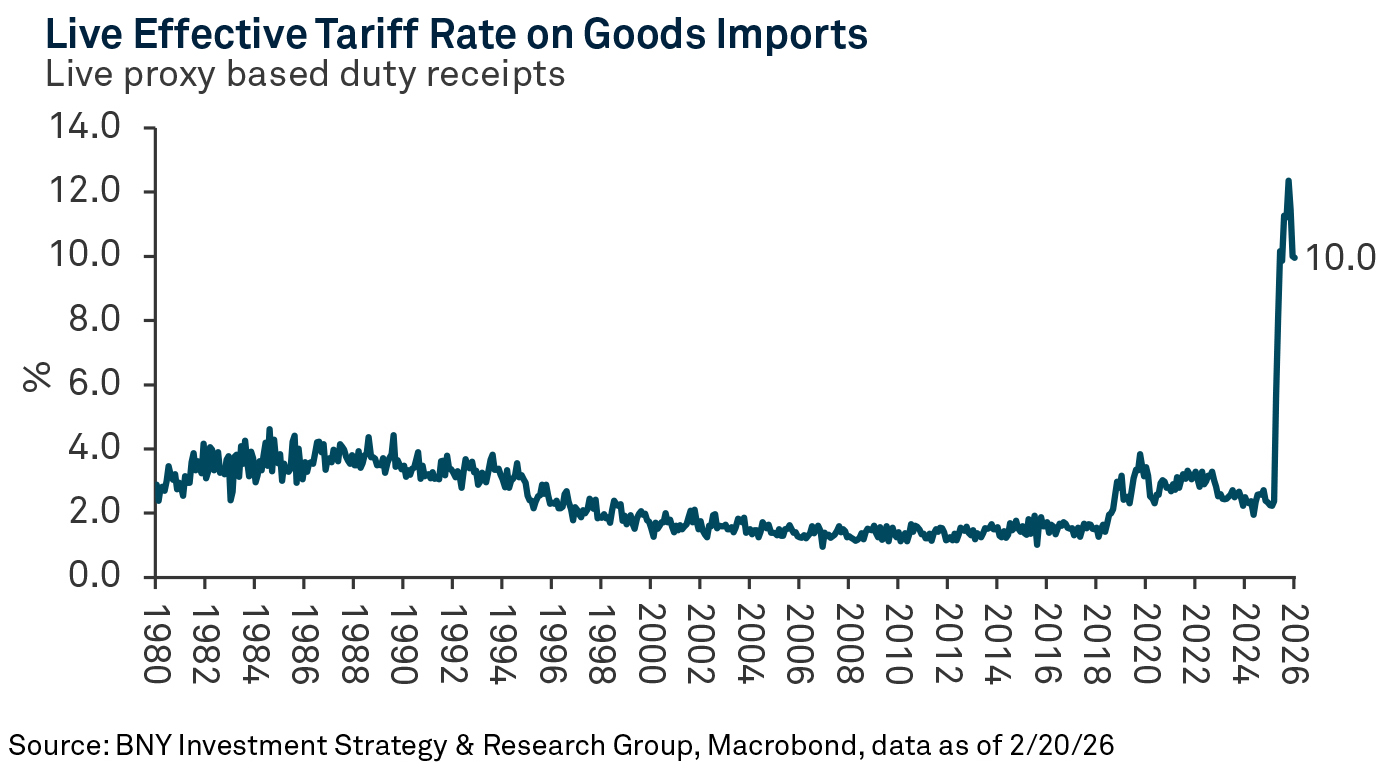

This ruling will not make tariffs disappear entirely. Tariffs imposed under different authorities other than IEEPA will remain in force. The Trump administration is currently pursuing alternative tariff authorities, starting with Section 122 of the Trade Act of 1974, which allows the president to impose tariffs of up to 15% for 150 days to address serious U.S. trade imbalances. At present, 10% global tariffs are in effect, and the White House has stated an aim of increasing them to 15%.

What Is the Impact on Growth and Inflation?

Under the previous tariff regime, before the Supreme Court struck them down, we estimated an implied overall tariff rate of roughly 15%. In practice, however, tariffs have not been fully passed through and actual duties paid have been closer to 10% due to exemptions, shifts in trade flows, and tariff avoidance.

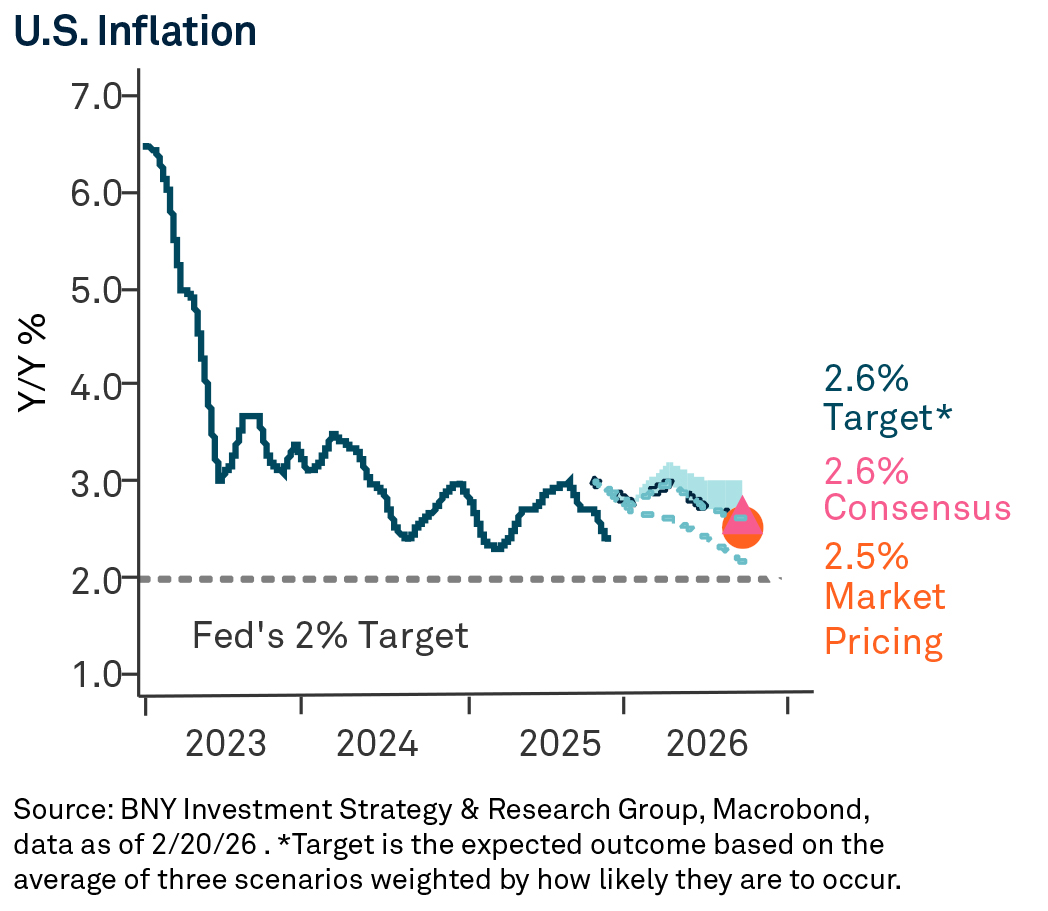

Excluding the newly imposed 10% tariff, the SCOTUS ruling alone would reduce headline tariff rates by roughly 6-7 percentage points and effective rates by about 4-5 percentage points. With tariffs partially reinstated, we would expect a modest boost to growth and a small reduction in inflation, by about 0.1-0.2 percentage points each. Increasing the reinstatement to 15% is estimated to lower overall tariff rates marginally below what was previously announced, suggesting minimal impact to growth or inflation.

It remains unclear whether customs duties collected to date under IEEPA would need to be refunded. If refunds were required, this could provide an additional, one-off boost to growth through cash returned to businesses. However, any refund process would likely be complex and resource-intensive, taking several months or longer.

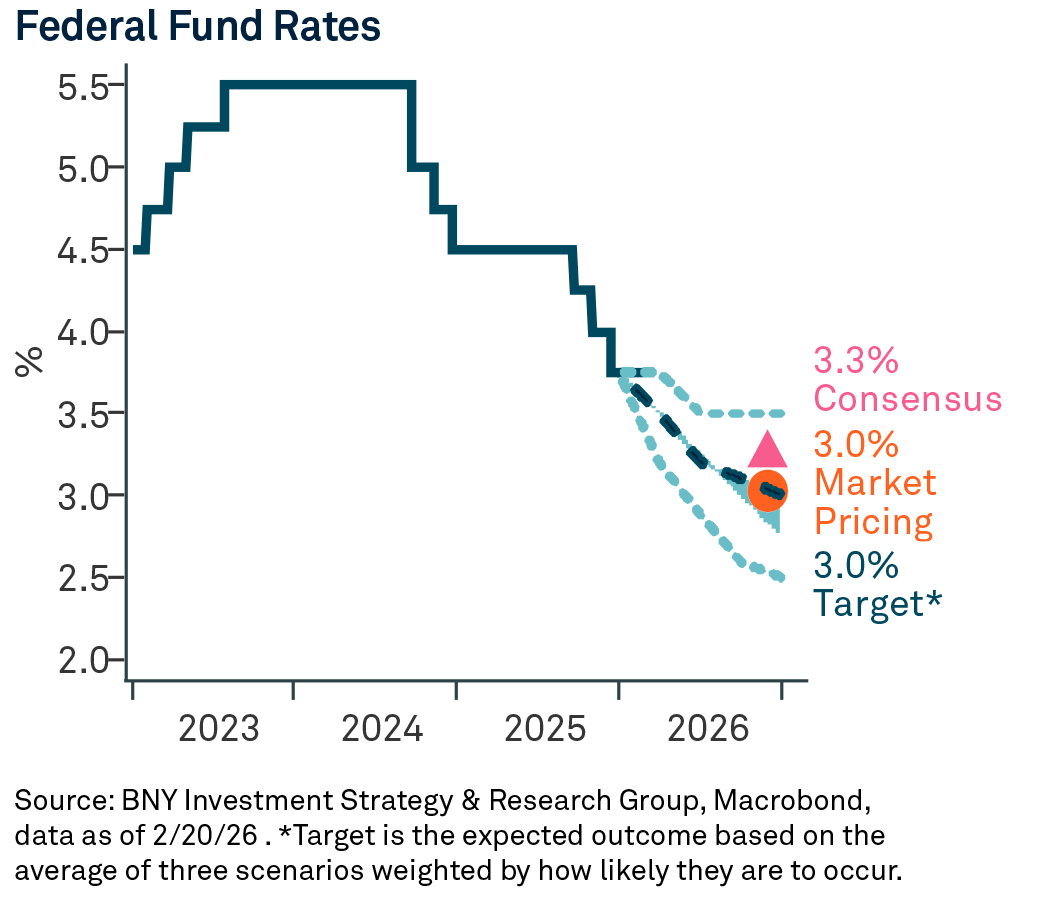

We do not expect these developments to materially alter the near-term path of Fed policy. While lower tariffs could modestly ease price pressures in the short run, they may also support a stronger recovery in economic activity and the labor market. Balancing these effects across plausible macro scenarios, we continue to see policy rates falling to 3.00% to 3.25% by the end of 2026.

What Are Asset Class Implications?

We believe that the lower tariff rate would act as a stimulus and be positive for risk assets, creating upside for equities. Lifting country-specific tariffs could ease pressure for certain trading partners, notably in emerging markets, and specifically, China and India. If the Trump administration pursues tariffs above 15% through alternative means, these actions would prompt a preliminary investigation and potentially delay implementation. This then creates an opportunity for trade to be front-loaded in select regions.

The ruling also implies reduced government funding, putting upward pressure on yields and increasing the likelihood of a steeper U.S. yield curve. In the absence of roughly $134 billion in tariff revenue collected under IEEPA1, about one-third of the estimated annual cost of the One Big Beautiful Bill Act would need to be financed through additional borrowing. Demand for 10-year Treasuries has already been weak over the last year, hovering just below the 25th percentile since 2008.

We will continue to monitor developments closely and provide updates as circumstances unfold. For more views, visit our Insights page.

Disclaimer

Past performance is no guarantee of future results.

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy.

Opinions and views expressed are subject to change without notice.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

© 2025 THE BANK OF NEW YORK MELLON CORPORATION

MARK-890807-2026-02-23

GU-804 - 31 January 2027