Lately, non-U.S. equities are outperforming the U.S. Is U.S. exceptionalism dead? Productivity growth tells a more positive story.

What is productivity and why does it matter to a country or region? For starters, productivity can be defined as economic output per hour of work. It’s one of the most impactful drivers of long-term growth as measured by gross domestic product (GDP), but it doesn’t stop there. GDP growth drives corporate profits, which in turn power higher stock market returns.

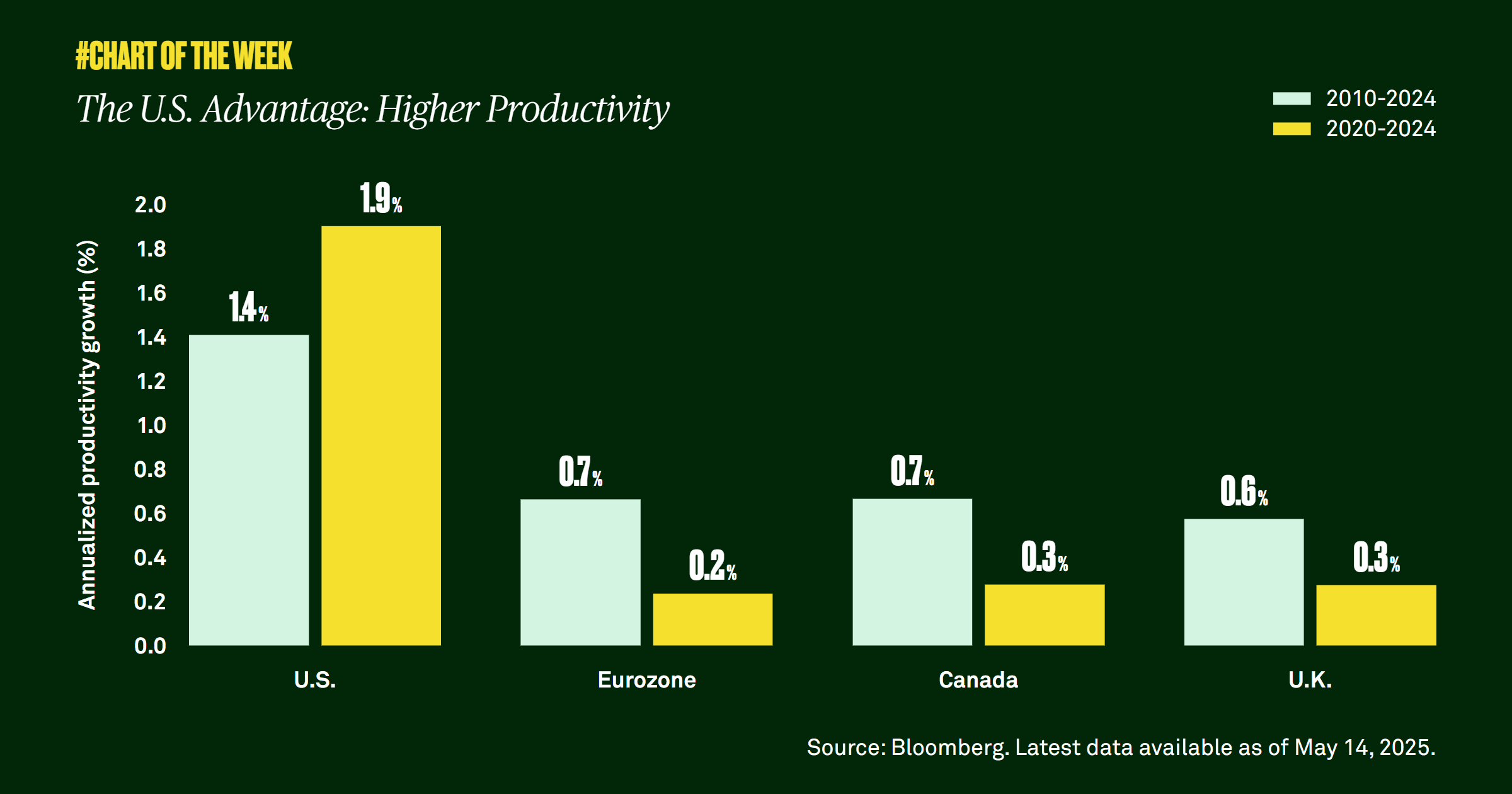

Since 2010, U.S. productivity has grown twice as fast as the rest of the world. Not surprisingly, U.S. economic growth and corporate profits have since outpaced the rest of the world. Stronger productivity and leadership in technology are key drivers of the U.S. equity markets’ outperformance relative to non-U.S. In addition, we believe the U.S.’ leadership in and increased adoption of artificial intelligence should continue to provide support.

What could weaken U.S. exceptionalism though is a reversal of the productivity gap between the U.S. and other major economies. However, since the global pandemic, that gap has only widened in favor of the U.S., and we expect that trend to persist. U.S. productivity and its ability to translate into higher corporate profitability are key reasons why we maintain our overweight to the U.S. equities.