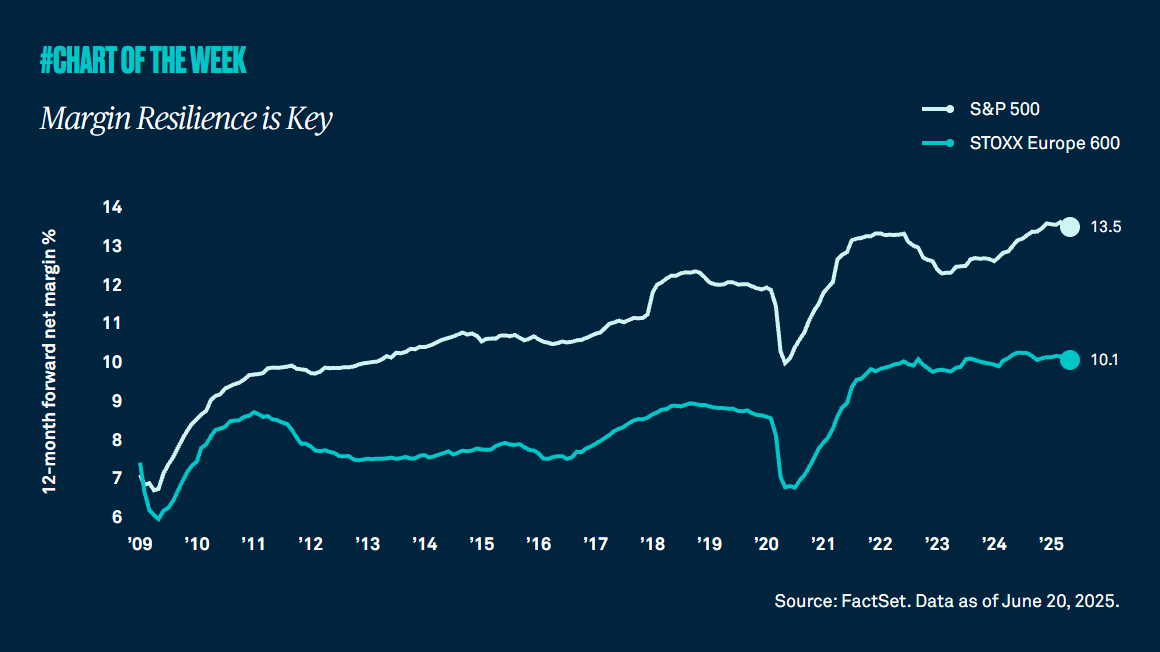

This year U.S. equities have underperformed the rest of the world due largely to policy uncertainty. However, an important driver of U.S. equity outperformance over the longer term has been stronger earnings and profit margins relative to peers, and our view is these factors will continue to drive long-term U.S. exceptionalism.

U.S. equities have had a challenging first half of the year, underperforming the rest of the world. A primary cause of this underperformance has been higher policy uncertainty and concerns about the impact of higher tariffs on growth.

While policy uncertainty can impact short-term volatility and lead to temporary underperformance, what does this mean for returns over the long term? An important driver of long-term returns is earnings and profit margins, where the U.S. has continued to outperform. In fact, since 2010 margins increased 6.4% to 13.5% as compared to a 2.7% increase in Europe to 10.1%. The difference between U.S. and European margins is now 3.4%, near the highest in history.

Additionally, technology leadership and increased adoption of artificial intelligence (AI) across diverse industries will likely support the continued expansion of U.S. margins, allowing them to surpass the rest of the world. Considering the many ways AI can improve profit margins for businesses, we anticipate that 2025 S&P 500 earnings per share will come in at $260-$270, demonstrating positive growth of roughly 8% as strong earnings and margin expansion continue to drive U.S. exceptionalism into the future.