China–U.S. relations are expected to stabilize for the foreseeable future, following the meeting of Presidents Trump and Xi in October. The highly anticipated “trade truce” reaches beyond the chips-for-minerals appeasement and runs the gamut — from soybeans to TikTok.

U.S. President Donald Trump and China’s President Xi Jinping came away from their in-person meeting with a long list of trade concessions. The agreement marked the culmination of tense discussions between the two nations, sparked by Trump’s tariff imposition earlier this year, and recently countered by Xi’s rare earth export controls.

Highlighting the trade arrangement, the U.S. agreed to cut tariffs on Chinese imports to 47% from 57%, while China agreed to tighten oversight of fentanyl distribution to the U.S. China also agreed to pause export controls on rare earth minerals for a year and resume purchasing soybeans from the U.S. for the next three years.

Impact on currency

The “trade truce” allows China to return to a lower tariff rate than before the Liberation Day announcement on April 1. From a macroeconomic perspective, China’s apparent geopolitical resilience should prove beneficial for the Chinese renminbi (CNH) and shield its tech sector from potential future export and investment controls by the U.S.

Over time, these developments could also allow more policy space for the CNH to slowly appreciate — at a pace which may support a gradual rebalancing of its economy without undermining its export sector.

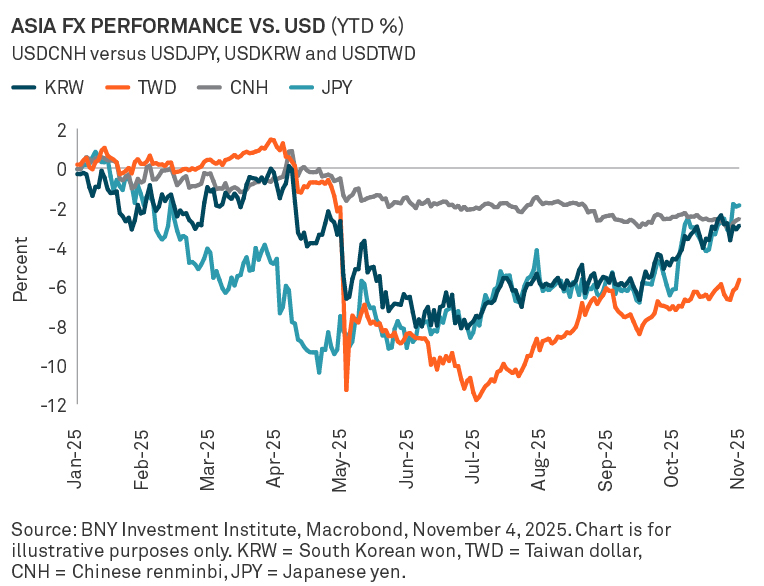

The CNH has appreciated more gradually but is starting to gain ground against a more volatile Japanese yen ( JPY) and other East Asian currencies which led regional FX gains versus the U.S. dollar earlier this year on increased hedging of under-hedged exposure in USD assets.

Expectations for long-term China-U.S. negotiations

Although this recent meeting has driven some optimism in the markets, it’s important to keep in mind that the “trade truce” is based on a mutual understanding and is not treaty-bound or legally binding. We believe long-term decoupling implies flare-ups are likely to recur sporadically.

About the BNY Investment Institute

Drawing upon the breadth and expertise of BNY Investments, the Investment Institute generates thoughtful insights on macroeconomic trends, investable markets and portfolio construction.

Important Information

For sole and exclusive use by Institutional Investors, Accredited Investors and Professional Investors only. Not for further distribution. This is a financial promotion and is not investment advice. Any views and opinions are those of the investment manager, unless otherwise noted. The value of investment can fall. Investors may not get back the amount invested. BNY, BNY Mellon and Bank of New York Mellon are the corporate brands of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally. BNY Investments encompass BNY Mellon’s affiliated investment management firms and global distribution companies. Any BNY entities mentioned are ultimately owned by The Bank of New York Mellon Corporation. In Hong Kong, the issuer of this document is BNY Mellon Investment Management Hong Kong Limited, which is registered with the Securities and Futures Commission (Central Entity Number: AQI762). In Singapore, this document is issued by BNY Mellon Investment Management Singapore Pte. Limited, Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore (MAS). This advertisement has not been reviewed by the Monetary Authority of Singapore.

GU-742 - 4 June 2026