INVESTMENT VIEWS

FROM THE BNY INVESTMENT INSTITUTE

October 2025

Markets are laser focused on this week’s FOMC meeting with expectations of a Federal Reserve (the Fed) rate cut and further signals for another cut in December.

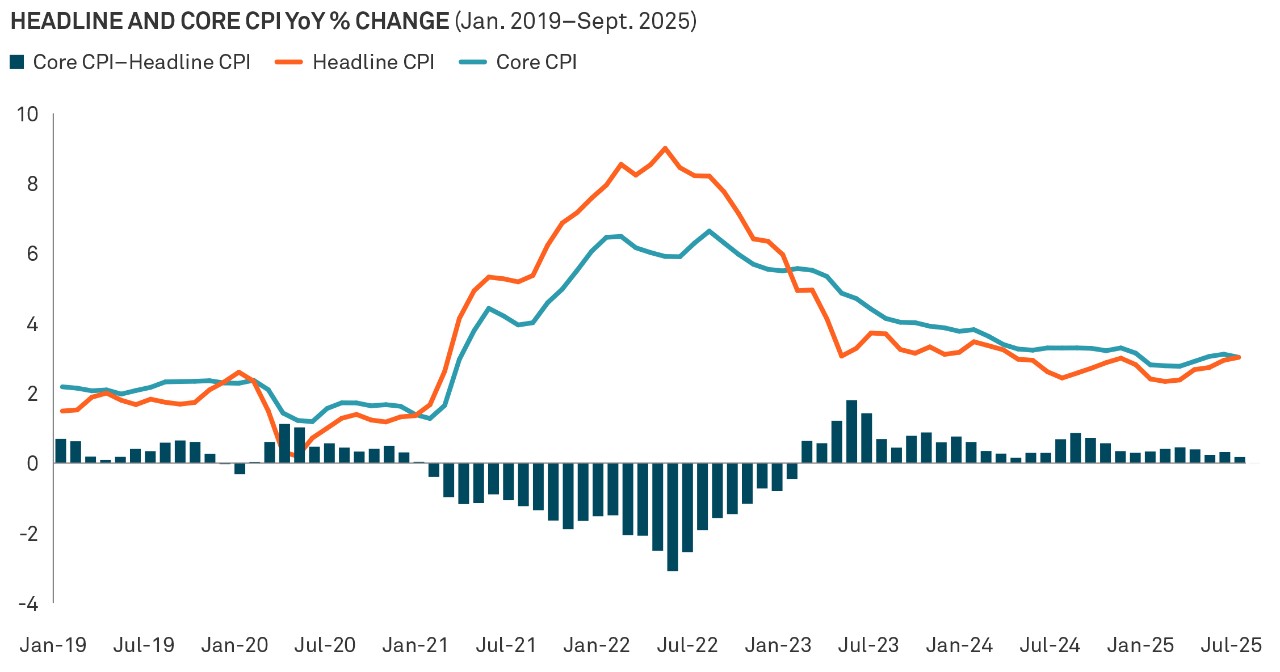

Meanwhile, the September convergence of Headline and Core Consumer Price Index (CPI) at roughly 3.0% year-over-year is yet another sign of potential Fed moves and paints the broader economic picture in two ways. First, it indicates a positive sign that neither gasoline nor groceries are driving unexpected jumps (or declines) in inflation. Second, the data underscores that “core” price pressures remain firmly above the Fed’s 2.0% target, leading to a greater likelihood of a rate cut at the October Fed meeting, and potentially another in December.

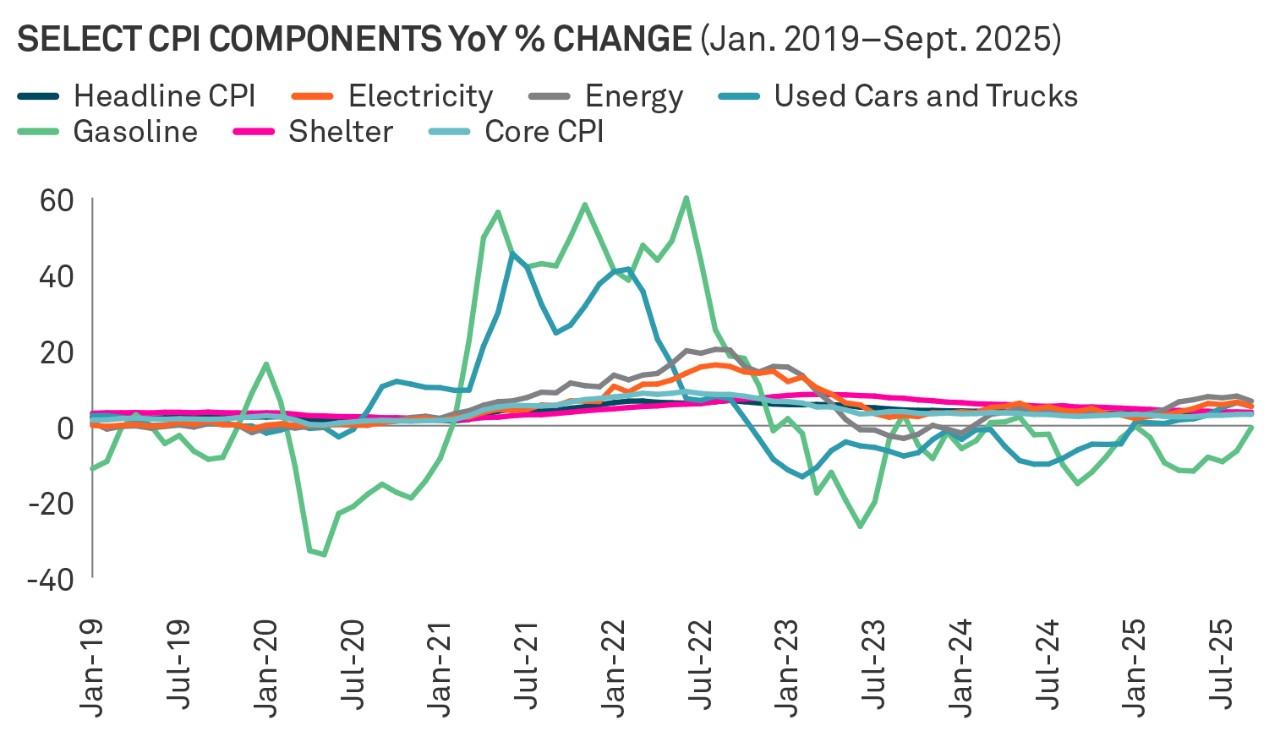

Context is everything and even inflation levels at 3.0% are low compared to components like energy, gasoline and used cars and trucks, which skyrocketed following Covid.

Source: BNY Investment Institute, Macrobond, October 2025. Chart is for illustrative purposes only.

CPI numbers in focus

The September CPI convergence tells a deeper story:

1. Energy & Food Volatility Has Waned

- The usual gap between headline (which swings with oil, gas and groceries) and core (which strips those out) CPI has narrowed because energy prices are no longer surging or plunging.

- Energy was only +1.5 percent month-over-month in September, and food just +0.2 percent—so neither category is distorting the aggregate.

2. Underlying Inflation Is More Broad-Based

- Core CPI has been the Fed’s go-to gauge of persistent price pressures; when headline drifts back toward core, it means the temporary shocks in food/energy aren’t masking the “real” trend.

- Here, headline = core at 3.0 percent year over year, signaling that both volatile and sticky components are moving in lock-step.

3. Implications for Policy & Markets

- Fed watchers: with no outsized energy spike to worry about, the focus shifts squarely onto core services (rent, wages, medical care).

4. Historical Context

- Over the past decade, the average gap between headline and core CPI has been around 1–1.5 percentage points. A zero gap is unusual and suggests a period of relative calm in the most volatile categories.

Meanwhile the differences between core CPI and headline CPI have normalized.

Source: BNY Investment Institute, Macrobond, October 2025. Chart is for illustrative purposes only.

What’s next for the Fed?

The market is looking for a Fed that doesn’t just cut 25 basis points (bp) this week but one that can also signal that more rate cuts will follow. Given our position, we believe there will be another 25bp rate cut in December.

It would take a de-anchoring of inflation expectations to shift the Fed’s reaction function, which we do not see as likely, due to stable wage growth. That said, market pricing still seems a little optimistic.

Data at a glance:

CPI

- Monthly Change: +0.3%

- Year-over-Year: +3.0%

Core CPI (excludes food & energy)

- Monthly Change: +0.2%

- Year-over-Year: +3.0%

Key Drivers

- Energy: gasoline prices were flat after summer declines

- Shelter: rent and owner's equivalent rent continued to be the largest upward contributor

- Used vehicles: modest price increases as supply constraints persist

- Food: prices rose 0.4% month-over-month, driven by away-from-home dining

- Medical Care: slowed from prior months, adding less to headline inflation

About the BNY Investment Institute

Drawing upon the breadth and expertise of BNY Investments, the Investment Institute generates thoughtful insights on macroeconomic trends, investable markets and portfolio construction.

Consumer Price Index (CPI) measures the overall change in consumer prices based on a representative basket of goods and services over time.

BNY Investment Institute consists of our macroeconomic research, asset allocation, manager research and operational due diligence teams. BNY Advisors is the brand name under which BNY Mellon Advisors, Inc. conducts its investment advisory business. BNY Mellon Advisors, Inc. is an investment adviser registered as such with the U.S. Securities and Exchange Commission pursuant to the Investment Advisers Act of 1940, as amended. BNY Mellon Advisors, Inc. is a subsidiary of The Bank of New York Mellon Corporation.

Disclaimer

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy.

Opinions and views expressed are subject to change without notice.

Past performance is no guarantee of future results.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia: BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE |

©2025 THE BANK OF NEW YORK MELLON CORPORATION

BABR-829463-2025-10-27

GU-736 – 30 March 2026