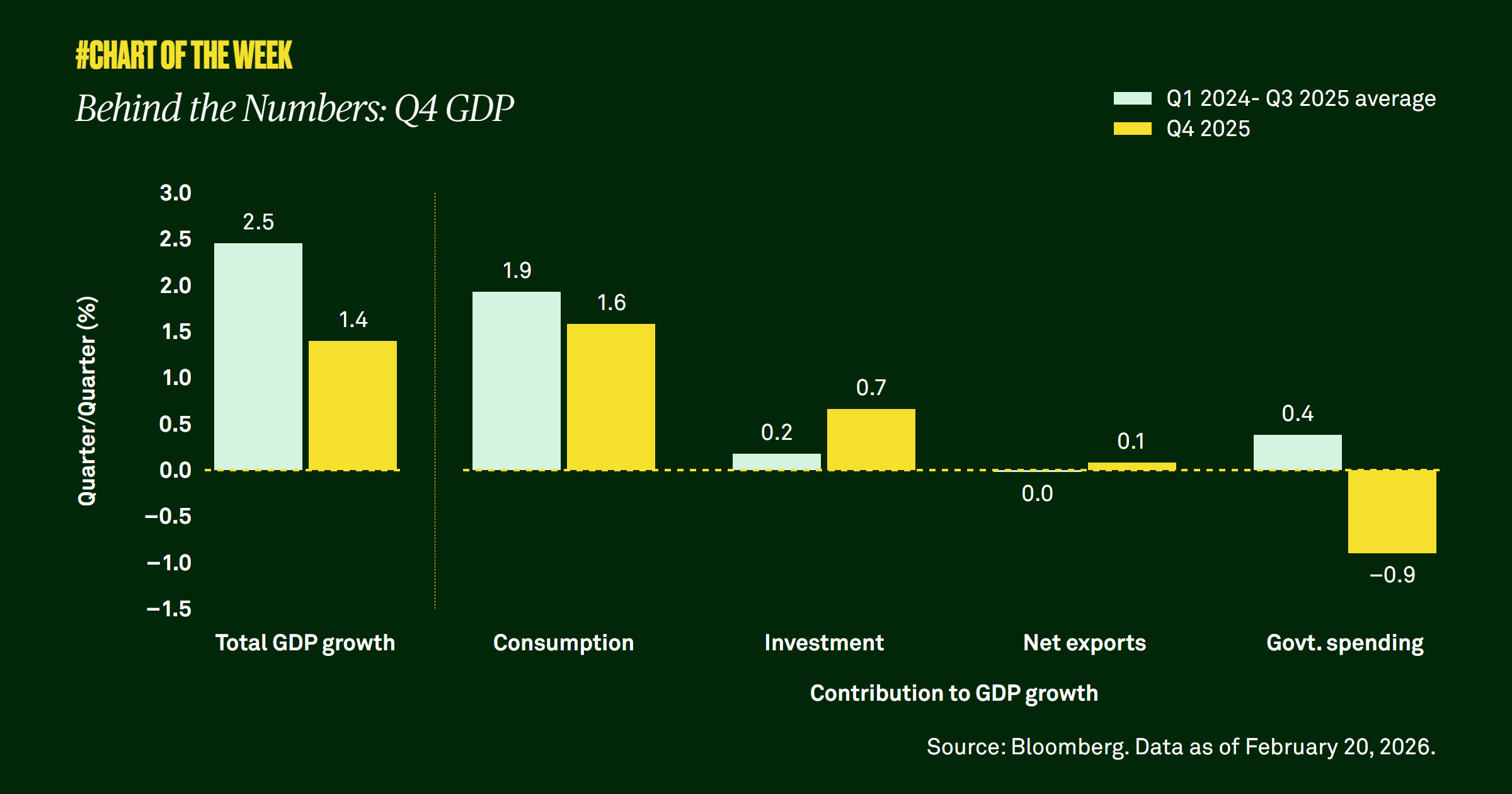

Gross domestic product undershot expectations last quarter, but the shortfall appears driven more by the temporary government shutdown than broad-based weakness. Consumer demand remains resilient, and with supportive fiscal policy, easing financial conditions and a steady labor market, the outlook points to a modest acceleration in economic activity this year.

Last week’s fourth quarter gross domestic product (GDP) report came in at annualized pace of 1.4%, disappointing many Wall Street analysts who had anticipated 2.8%. For some investors, the news renewed concerns about an economic slowdown.

Growth was indeed softer than the 3% or more recorded in the previous two quarters, but the drivers of the miss are clear. The biggest drag was government spending at −0.9%, an unusually weak contribution that suggests the fourth quarter could have ended near 2.3% — above trend — absent the 43‑day government shutdown.

Consumption, the largest driver of GDP with a 70% share, slowed slightly to 1.6%, yet it remains resilient and in line with the average since 2024. We believe fiscal stimulus, lower interest rates and a steady job market will support household balance sheets and spending going forward.

Taken together, the evidence suggests the government shutdown — rather than a broad slowdown — drove the shortfall. Consensus GDP is 2.5% this year, and our target of 2.3% closely matches, reflecting our confidence in the economy amid a steady job market and sustained consumer spending.