Market uncertainty and the possibility of inflation becoming less well anchored is encouraging investors to pay more attention to infrastructure assets.

As 2026 neared its mid-year point, concerns about the impact of geopolitical shocks on inflation and growth have lingered despite hopes for a scaling back in the Middle East conflict.

European Central Bank (ECB) research and US Federal Reserve commentary has suggested geopolitical supply shocks could re-anchor inflation expectations higher1. On 29 May, for example, ECB Governing Council member Fabio Panetta warned that oil and gas prices were unlikely to normalise quickly even if the Iran conflict was rapidly resolved2.

Investors, grappling to make sense of the multiple macro cross currents, have been seeking out ways to enhance portfolio resilience and diversification while also targeting evolving upside opportunities.

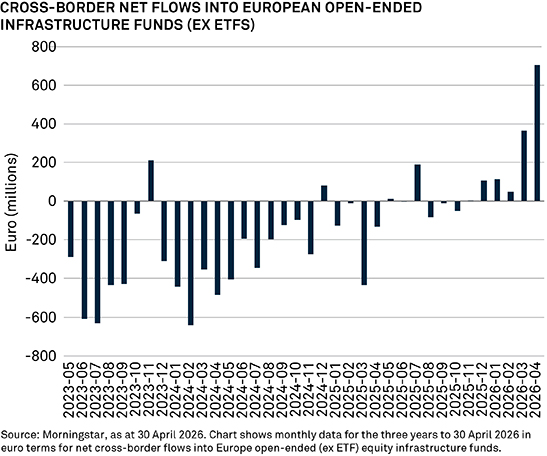

To this end, asset classes that have shifted more into favour include infrastructure and real assets. The chart below, for example, shows a significant uptick in cross-border net flows into European open-ended infrastructure funds, in euro terms, in the first half of 2026.

Inflows into listed infrastructure assets are parallelled in private markets too. According to the 2025 IFM Investors Private Markets 700 annual survey, allocations are trending upwards as investors become increasingly confident about the potential returns of infrastructure equity and infrastructure debt3. Based on the responses of 714 senior investment professionals, the number of institutional investors planning to allocate capital to infrastructure equity and debt is projected to grow from 50% to 60% by 2030; key reasons being risk management and return enhancement. Survey respondents said they expected the potential returns of infrastructure equity and infrastructure debt respectively will outstrip those offered by private equity and private debt, with average net returns expected from private infrastructure equity and private infrastructure debt standing at 13.4% and 9.59% respectively.

According to several BNY thought leaders, this shift can be understood against the backdrop of a move to a new, as yet undefined, economic order in which periods of volatility, supply-side shocks and heightened macroeconomic uncertainty likely become more frequent; one in which investors will need to focus more on active, targeted return seeking (i.e., less on broad-based beta exposures that benefited from artificially easy monetary conditions) as well as effective portfolio diversification and downside protection.

An additional appeal to investing in infrastructure assets is the massive, long-term demand for infrastructure projects globally. Demand has escalated due to secular trends like:

- Energy security and decarbonisation. Geopolitical shifts and ambitious net-zero targets have accelerated the need for capital deployment in renewable power generation, grid expansion and energy storage.

- Digitalisation and AI. The explosive growth in artificial intelligence, cloud computing and data sovereignty has created an urgent, massive demand for real-world digital infrastructure, such as fibre networks and data centres.

According to management consulting firm McKinsey & Company, the world requires an estimated US$106 trillion in infrastructure investment by 2040 to meet the demands of global population growth and to enable parabolic technological advancement4.

Various governments are seeking to address this challenge. For example, the UK introduced the Planning and Infrastructure Act 2025 in December last year, a landmark piece of legislation designed to expedite the construction of new homes, improve transport links and support clean energy projects. In March 2026, the National Infrastructure and Service Transformation Authority put the value of the UK’s infrastructure project pipeline over the next decade at £718 billion5.

Clearly, infrastructure has much to offer investors worried about geopolitical uncertainty and macroeconomic volatility, and who are looking for inflation protection, resilient diversification options and dependable investment returns.

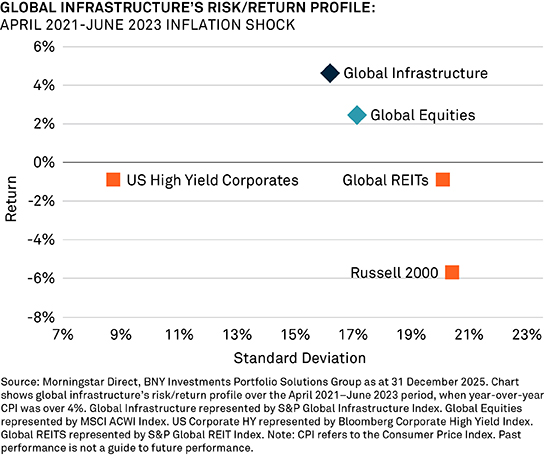

Infrastructure works as an inflation hedge because infrastructure revenues are frequently tied to long-term contracts or regulated frameworks with built-in inflation pass-through mechanisms, helping protect real returns during periods of price volatility. Infrastructure’s risk/return performance during the inflation spike over the April 2021–June 2023 period, when year-over-year CPI was over 4%, lends weight to this view.

Infrastructure can also deliver resilient, defensive returns. This is because infrastructure assets like toll roads, utilities and energy grids – as essential services – provide steady, predictable demand across all economic cycles.

Admittedly, inflation and growth-related concerns in markets will likely abate somewhat following signs of an easing in the Middle East conflict. However, there remains a case for having some exposure to asset classes that can aid portfolio resilience beyond what a traditional 60/40 portfolio offers.

1A European Central Bank research post has warned that consumer expectations following the Iran war point to renewed stagflation concerns, although the reaction has so far been less severe than that which followed Russia’s invasion of Ukraine in 2022. See ECB blog, 29 May 2026, “Geopolitical risk and scarring effects on consumer expectations: insights from the wars in Ukraine and Iran” https://www.ecb.europa.eu/press/blog/date/2026/html/ecb.blog20260529~fdd1d1e8a3.en.html

Meanwhile, Federal Reserve Bank of St. Louis President Alberto Musalem has stated that policymakers should not rely on a potential AI-driven productivity boom to reduce the currently elevated US inflation, which remains significantly above the 2% target. Source: Bloomberg. https://www.bloomberg.com/news/articles/2026-05-28/fed-s-musalem-says-officials-can-t-rely-on-ai-to-fix-inflation?srnd=homepage-europe

2 Source: Reuters, 29 May 2026. https://www.msn.com/en-gb/money/other/ecb-will-act-to-head-off-persistent-inflation-panetta-says/ar-AA24lmB2?ocid=BingNewsSerp. In June, the ECB raised its key interest rate to 2.25% to combat inflation – its first tightening move since 2023.

3IFM Investors’ Private Markets 700 Report, 2025. The report provides a window into how institutional investors around the world view and approach private markets.

4McKinsey & Company, Global Private Markets Report, March 2026, “Infrastructure: Investing to support global growth”.

5Source: National Infrastructure and Service Transformation Authority (NISTA) press release “Infrastructure Pipeline update signals future workforce needs” dated 9 March 2026. NISTA is a public agency set up in 2025 to advise the UK Government on infrastructure delivery and improvement.

FOR INSTITUTIONAL, PROFESSIONAL, QUALIFIED INVESTORS AND QUALIFIED CLIENTS ONLY.

Past performance is not a guide to future performance.

This material should not be considered as investment advice or a recommendation of any investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Any statements and opinions expressed are those of the author as at the date of publication, are subject to change as economic and market conditions dictate, and do not necessarily represent the views of BNY. The information has been provided as a general market commentary only and does not constitute legal, tax, accounting, other professional counsel or investment advice, is not predictive of future performance, and should not be construed as an offer to sell or a solicitation to buy any security or make an offer where otherwise unlawful. The information has been provided without taking into account the investment objective, financial situation or needs of any particular person. BNY is not responsible for any subsequent investment advice given based on the information supplied. This is not investment research or a research recommendation for regulatory purposes as it does not constitute substantive research or analysis. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be and should not be interpreted as recommendations. Past performance is no guarantee of future results. Information and opinions presented have been obtained or derived from sources which BNY believed to be reliable, but BNY makes no representation to its accuracy and completeness. BNY accepts no liability for loss arising from use of this material. BNY, BNY Mellon and Bank of New York Mellon are the corporate brands of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally.

All investments involve risk including loss of principal.

Not for distribution to, or use by, any person or entity in any jurisdiction or country in which such distribution or use would be contrary to local law or regulation. This information may not be distributed or used for the purpose of offers or solicitations in any jurisdiction or in any circumstances in which such offers or solicitations are unlawful or not authorized, or where there would be, by virtue of such distribution, new or additional registration requirements. Persons into whose possession this information comes are required to inform themselves about and to observe any restrictions that apply to the distribution of this information in their jurisdiction.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYMSC), 240 Greenwich Street, New York, NY 10286. BNYMSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • Singapore: BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. •Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized andregulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All entities are subsidiaries of The Bank of New York Mellon Corporation.

BNY COMPANY INFORMATION

BNY Investments is one of the world’s leading investment management organizations, encompassing BNY Mellon’s affiliated investment management firms and global distribution companies. BNY, BNY Mellon and Bank of New York Mellon are the corporate brands of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally. • Mellon Investments Corporation (MIC) is a registered investment advisor and subsidiary of The Bank of New York Mellon Corporation. MIC is composed of two divisions: Mellon, which specializes in index management, and Dreyfus, which specializes in cash management and short duration strategies. • Insight Investment - Investment advisory services in North America are provided through two different investment advisers registered with the Securities and Exchange Commission (SEC) using the brand Insight Investment: Insight North America LLC (INA) and Insight Investment International Limited (IIIL). The North American investment advisers are associated with other global investment managers that also (individually and collectively) use the corporate brand Insight. Insight is a subsidiary of The Bank of New York Mellon Corporation. • Newton Investment Management - “Newton” and/or “Newton Investment Management” is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021, NIMJ was established in March 2023. NIM and NIMNA are registered with the Securities and Exchange Commission (SEC) in the United States of America as an investment adviser under the Investment Advisers Act of 1940. Newton is a subsidiary of The Bank of New York Mellon Corporation. • ARX is the brand used to describe the Brazilian investment capabilities of BNY Mellon ARX Investimentos Ltda. ARX is a subsidiary of The Bank of New York Mellon Corporation. • Walter Scott & Partners Limited (Walter Scott) is an investment management firm authorized and regulated by the Financial Conduct Authority, and a subsidiary of The Bank of New York Mellon Corporation. • Siguler Guff - BNY owns a 20% interest in Siguler Guff & Company, LP and certain related entities (including Siguler Guff Advisers LLC). • BNY Mellon Advisors, Inc. (BNY Advisors) is an investment adviser registered as such with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Investment Advisers Act of 1940, as amended. BNY Advisors is a subsidiary of The Bank of New York Mellon Corporation.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All information contained herein is proprietary and is protected under copyright law.

NOT FDIC INSURED |NO BANK GUARANTEE | MAY LOSE VALUE |

©2025 THE BANK OF NEW YORK MELLON CORPORATION

GU3468900 Exp: 30 December 2026