Le nouveau Premier ministre japonais, Sanae Takaichi, devrait adopter des politiques budgétaires et monétaires accommodantes, ce qui pourrait soutenir les actions japonaises mais exercer une pression sur le yen.

Le Parti libéral-démocrate (PLD) du Japon a organisé un second tour pour l’élection de son chef, qui a abouti à la victoire de Sanae Takaichi. Si, comme prévu, elle est confirmée par le Parlement (vers la mi-octobre), elle deviendra la première femme Premier ministre du Japon. Sa victoire lors du second tour du week-end est une surprise, car le candidat réformateur, Shinjiro Koizumi, était largement favori. Cela laisse entrevoir des luttes de factions visant à retarder le renouvellement générationnel à la tête du PLD.

Le yen japonais (JPY) devrait subir une pression relative, les marchés considérant largement Takaichi comme une partisane de la relance budgétaire, préférant une normalisation monétaire plus progressive que ce qui est déjà anticipé par le marché. L’incertitude entourant les objectifs budgétaires et la probabilité accrue d’une intervention gouvernementale sur la politique monétaire devraient peser sur le yen. Certes, dans un contexte de dollar américain faible (ou du moins moins fort), nous n’anticipons pas une forte dépréciation du taux de change bilatéral. Mais le JPY devrait sous-performer par rapport aux autres grandes devises tant que la politique n’aura pas gagné en clarté.

L’impact à court terme sur les obligations d’État japonaises (JGB) devrait être mineur ou indéterminé. Cela dépendra en grande partie des nominations au sein du cabinet de Takaichi et de l’orientation réelle de ses politiques. Par exemple, la nomination d’un ministre des Finances conservateur, issu d’une des factions traditionnelles du PLD, pourrait rassurer sur le risque de dérapage budgétaire. Mais des mesures de soutien immédiat, dans le budget supplémentaire de fin d’année, pour faire face à la hausse du coût de la vie, pourraient inclure des subventions et des crédits d’impôt pour les ménages à faibles et moyens revenus, qui seront scrutés de près par les marchés.

Des inquiétudes plus larges sur la stabilité du gouvernement persisteront, alors que les négociations politiques et les tensions de coalition reviendront sur le devant de la scène. Nous pensons que la prochaine étape, après l’octroi d’aides immédiates via subventions et crédits d’impôt dans le budget supplémentaire, sera une tentative de baisse du taux de TVA ou d’exonération de certains produits alimentaires. Cela nécessitera une modification législative soutenue par une majorité simple dans les deux chambres du Parlement. Mais, étant donné la position minoritaire du PLD et les risques de dissensions internes, des compromis avec l’opposition seront nécessaires – à défaut, de nouvelles élections pourraient être convoquées pour obtenir un mandat plus clair. Ces incertitudes pourraient limiter le potentiel de hausse du yen.

Les actions japonaises devraient mieux se comporter dans les prochains jours, car les marchés perçoivent les orientations du nouveau Premier ministre comme accommodantes, et la politique macroéconomique globale devrait favoriser des conditions financières plus souples et durables. Une impulsion budgétaire plus favorable, une croissance nominale du PIB plus ferme, un yen relativement plus faible et une probabilité réduite d’aplatissement (voire de pentification) de la courbe des taux des JGB sont de bon augure pour les actions. Mais tout rebond pourrait marquer une pause si la Banque du Japon procède à une nouvelle hausse des taux lors de l’une de ses prochaines réunions – le 30 octobre ou le 19 décembre.

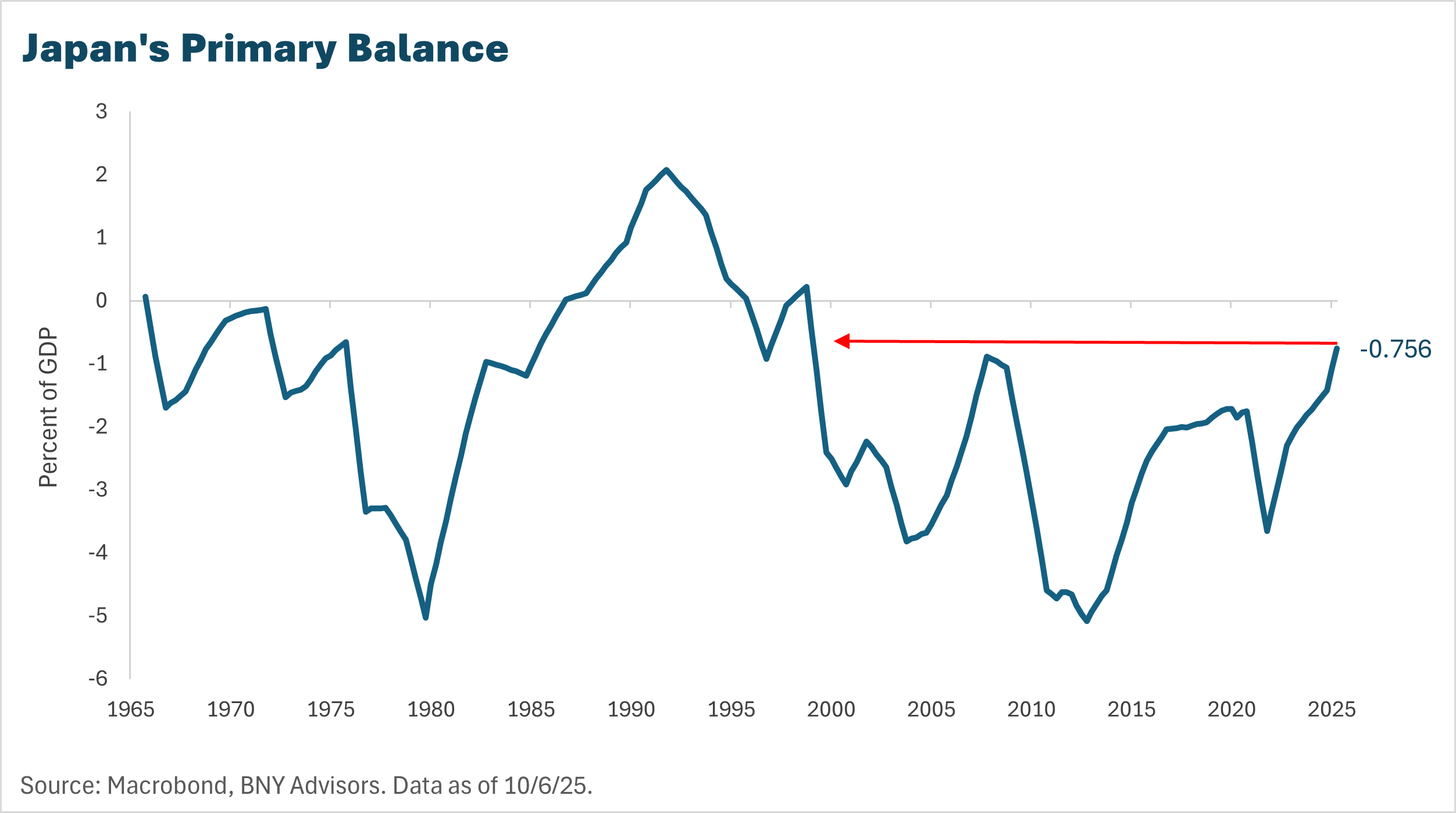

Dans l’ensemble, il semble prudent de se prémunir davantage contre les risques baissiers du JPY dans ce contexte d’incertitude, mais il est encore trop tôt pour s’inquiéter d’un dérapage budgétaire massif ou d’une insoutenabilité de la dette publique. Le Premier ministre sortant, Ishiba, avait maintenu une discipline budgétaire stricte – le déficit primaire ayant été ramené à seulement 0,8 % du PIB, son niveau le plus bas depuis la fin des années 1990. Une forte croissance nominale et une politique budgétaire rigoureuse ont également contribué à placer l’énorme dette publique du Japon sur une trajectoire descendante – passant de 226 % du PIB fin 2020 à 210 % à la mi-2025. Parallèlement, l’élargissement des primes de terme et des rendements réels depuis le début de l’année, qui semblent excessifs par rapport aux autres économies avancées, nous amène à penser que la dynamique de la dette japonaise et la valorisation attractive des JGB (notamment sur le long terme) offrent une certaine protection contre l’incertitude politique.

À propos du BNY Investment Institute

S’appuyant sur l’expertise de BNY Investments, l’Investment Institute propose des analyses approfondies sur les tendances macroéconomiques, les marchés investissables et la construction de portefeuille.

Produit intérieur brut (PIB) : valeur totale de tous les biens et services finis produits à l’intérieur des frontières d’un pays sur une période donnée.

Prime de terme : rendement supplémentaire exigé par les investisseurs pour détenir une obligation à long terme plutôt qu’à court terme.

Rendements réels : taux d’intérêt perçu par les investisseurs sur les obligations d’État, après prise en compte de l’inflation.

GU-722 - 30 October 2026