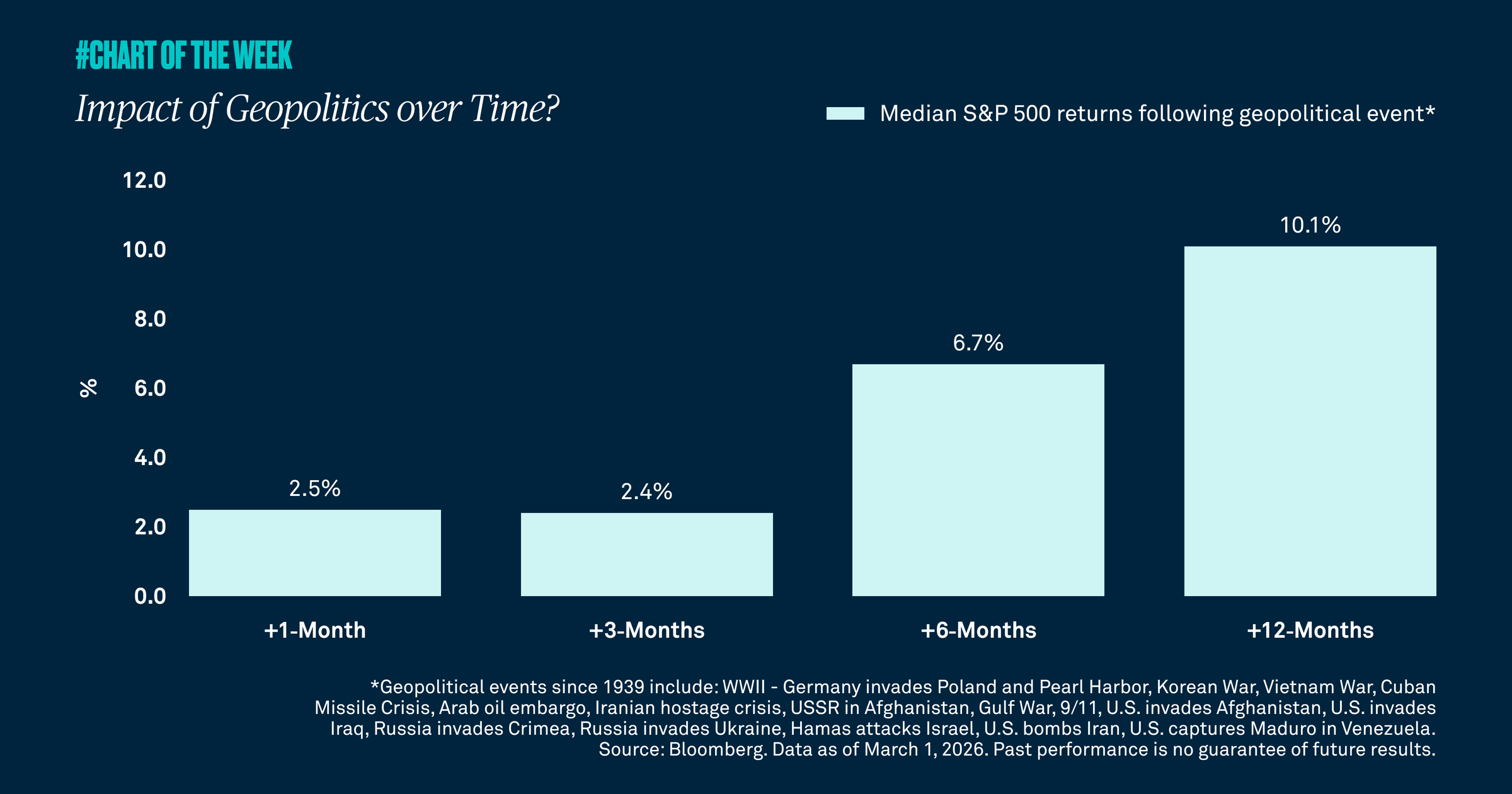

Tensions between the U.S./Israel and Iran have recently boiled over into a military conflict, which has given many investors the jitters. However, our research shows that equity market pullbacks resulting from geopolitical events are often short lived with the S&P 500 typically higher in the months following these events.

The events in the Middle East involving the U.S., Israel and Iran have led many investors to worry about the near-term implications for financial markets and oil in particular. As largely expected, the biggest impact has been on the price of oil. While it may be hard to know how long this conflict will last, history demonstrates that as long as there is no sustained energy supply shock, S&P 500 returns are higher one, three, six and 12 months after a geopolitical conflict according to data since 1939.

Over time, it’s equity market fundamentals — earnings and interest rates ― that drive markets. Given that the fundamentals remain supportive, we reiterate our constructive outlook on global growth and markets in 2026, reminding investors that a globally diversified portfolio will help navigate near-term uncertainty and preserve wealth.