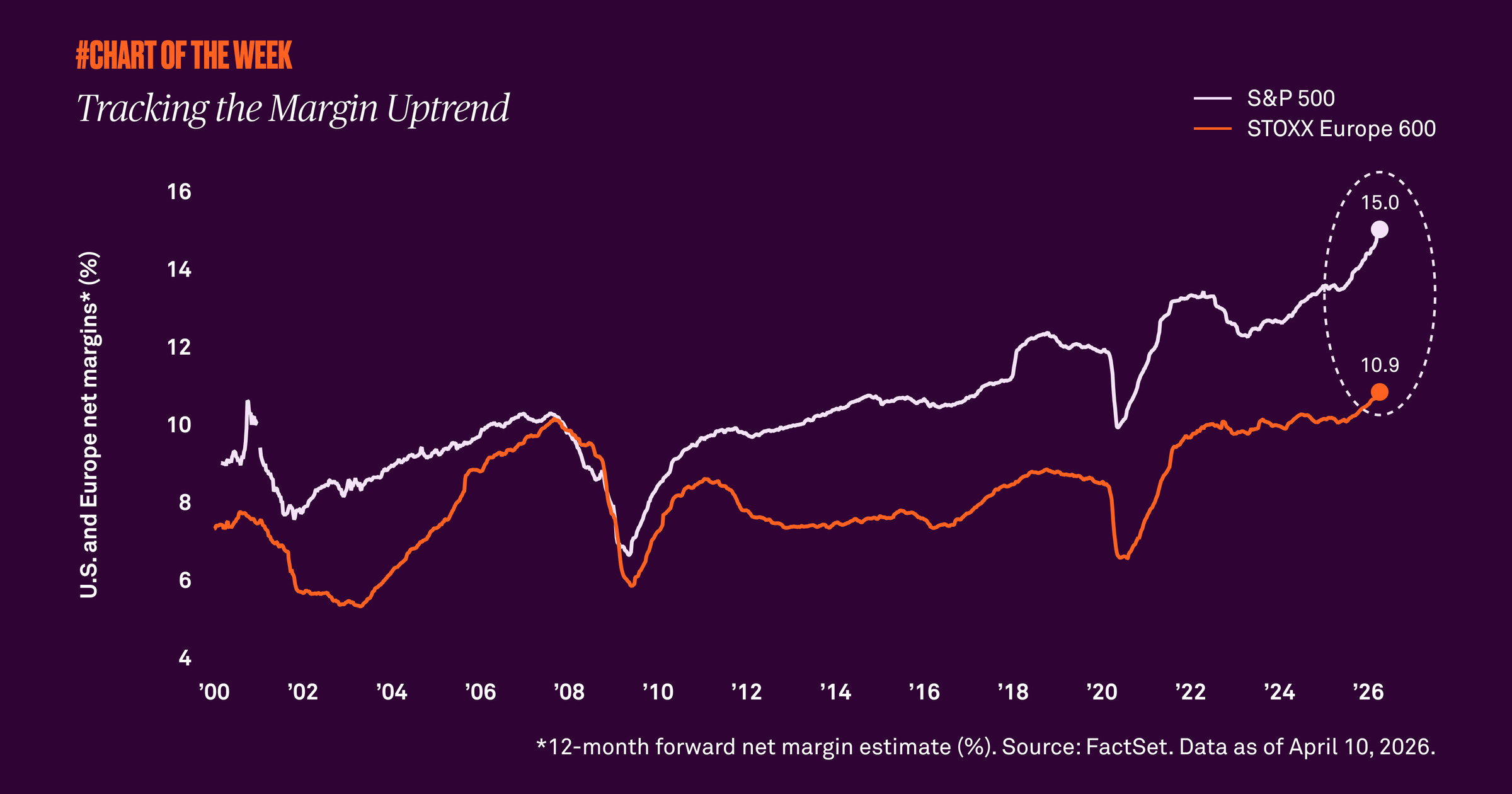

Rising margin expectations continue to support equities, underscoring the resilience of corporate profitability in the face of last year’s tariffs and this year’s Middle East war. The U.S. remains especially strong compared to peers, though first quarter earnings will be an important test.

Margins remain one of the clearest indicators of corporate strength because they illustrate how much profit companies keep after absorbing the costs of doing business. The recent rise in future margin estimates is therefore an important support for equities.

What stands out now is the resilience of those margins. Despite last year’s tariff concerns and this year’s geopolitical uncertainty, margin expectations have continued to move higher rather than weaken. That suggests companies are still exercising pricing power, cost discipline and an ability to protect profitability in a more challenging environment.

Additionally, the U.S. continues to lead its peers. Forward S&P 500 profit margin estimates are near 15% versus roughly 11% in Europe, demonstrating the widest gap on record. That margin advantage helps support our positive view on U.S. equities, though first quarter earnings remain an important signal. Any meaningful weakness in guidance or downward margin revisions could pressure estimates, shift sentiment and increase volatility.