The AI revolution is not just a tech story; it is a capital allocation story, and private markets are at the center of an AI-driven capital expenditure boom. Given AI’s infrastructure requirements from data centers and semiconductor fabricators to energy infrastructure, private investment should become a facilitator of AI adoption, creating significant investment opportunities for investors.

AI as a Capital Allocation Story

In 2024, global venture capital (VC) funding for AI startups surged to $131.5 billion, marking a 52% increase year over year.1 Landmark deals, such as Databricks ($10 billion),2 Anthropic ($13 billion),3 and OpenAI (close to $7 billion),4 underscore the scale of private investment flowing into foundational models and infrastructure. This deal flow reflects confidence in AI as a dynamic sector with significant growth potential.

We are also seeing more partnerships between large tech companies and startups, as corporations tap into the VC sector for R&D and selective acquisitions, expanding exit opportunities for early investors. Additionally, crossover public-private investment in later-stage rounds helps to temper bubble concerns by estimating value from cash flow fundamentals and comparable valuations rather than speculation.

AI Drives Infrastructure Spending

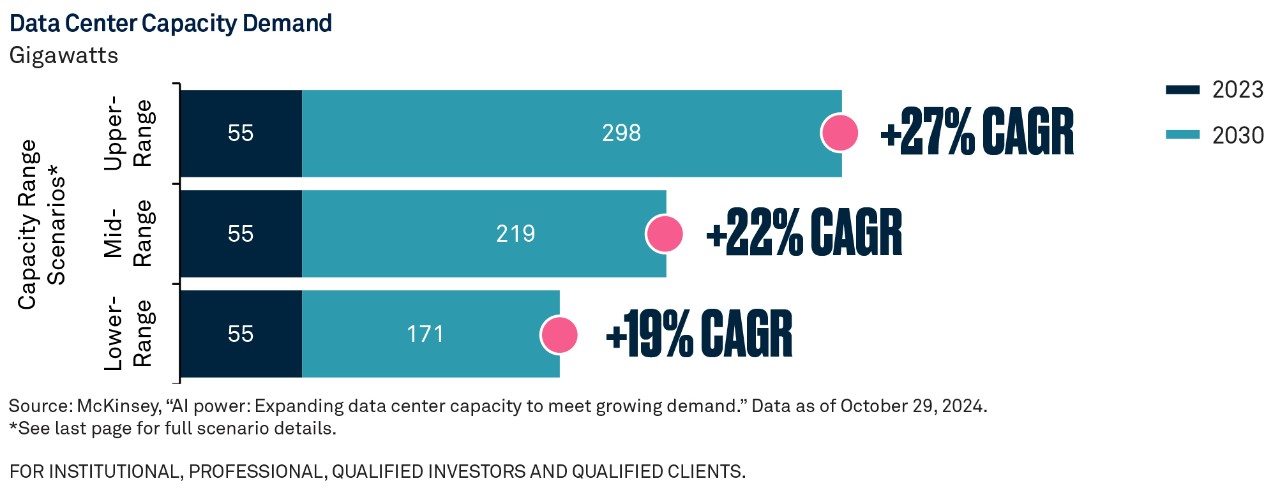

AI’s potential for productivity growth is fueling unprecedented demand for data centers, semiconductor facilities, and energy systems critical in supporting the computationally intensive workloads of AI. The top five hyperscalers spent over $215 billion on data center infrastructure in 2024 — a 50% year-over-year increase.5 As shown in the chart on the previous page, data center capacity is expected to grow at a CAGR of 19% to 27% through 2030.6 This creates significant opportunities for private real asset funds to invest in the initial buildout of the AI ecosystem.7

Energy & Electricity Requirements

The energy implications from AI are profound. U.S. data centers consumed 176 terawatt-hours (TWh) of electricity in 2023, accounting for 4.4% of total national energy usage. That figure is projected to rise at a much faster rate, to between 7% and 12% of total U.S. consumption by 2028.8 Meeting this demand requires private investment in energy infrastructure, including natural gas, independent power producers, and renewables. Private real asset funds are well-positioned to capitalize on this trend.

Private Market Vehicles for Infrastructure

Private equity and venture capital remain key funders of startups and are well-suited for long-term, active investments in AI infrastructure. They are increasingly complemented by private infrastructure and real estate funds, which offer inflation-linked returns and exposure to secular trends in energy and data.

Private Credit: A Bigger Deal

Over the last three decades, private credit has evolved from a niche allocation to a core component of corporate financing. While the number of FDIC-insured banks fell from 14,434 in 1980 to approximately 4,200 in 2024,9 private credit funds stepped in to supply middle-market companies with flexible capital. Filling this disintermediation gap pushed assets under management in private credit to approximately $1.7 trillion by 2025.10

Rise of Direct Lending

Direct lending - privately negotiated loans typically secured as senior debt from asset managers by middle-market companies - has become one of the fastest-growing segments of private credit. Transactions now routinely exceed $1 billion and offer a compelling alternative to public markets or syndicated loans. Borrowers benefit from faster execution, tailored terms, and reduced syndication risk, while lenders benefit from higher interest rates and an illiquidity premium. Private credit has historically delivered a 200–300 basis point premium over public debt.11

Asset-Backed Lending as a Complement

Asset-backed lending - another subset of private credit - has also gained traction and complements direct lending by offering loans secured by tangible assets such as inventory, receivables, and equipment. The global asset-based lending market was valued at $661.7 billion in 2023 and is projected to grow at a CAGR of over 11% through 2032.12 These loans offer front-loaded cash flows and reduced correlation to public markets, enhancing diversification and income generation.

Private vs. Public Markets: Shifting Capital Formation

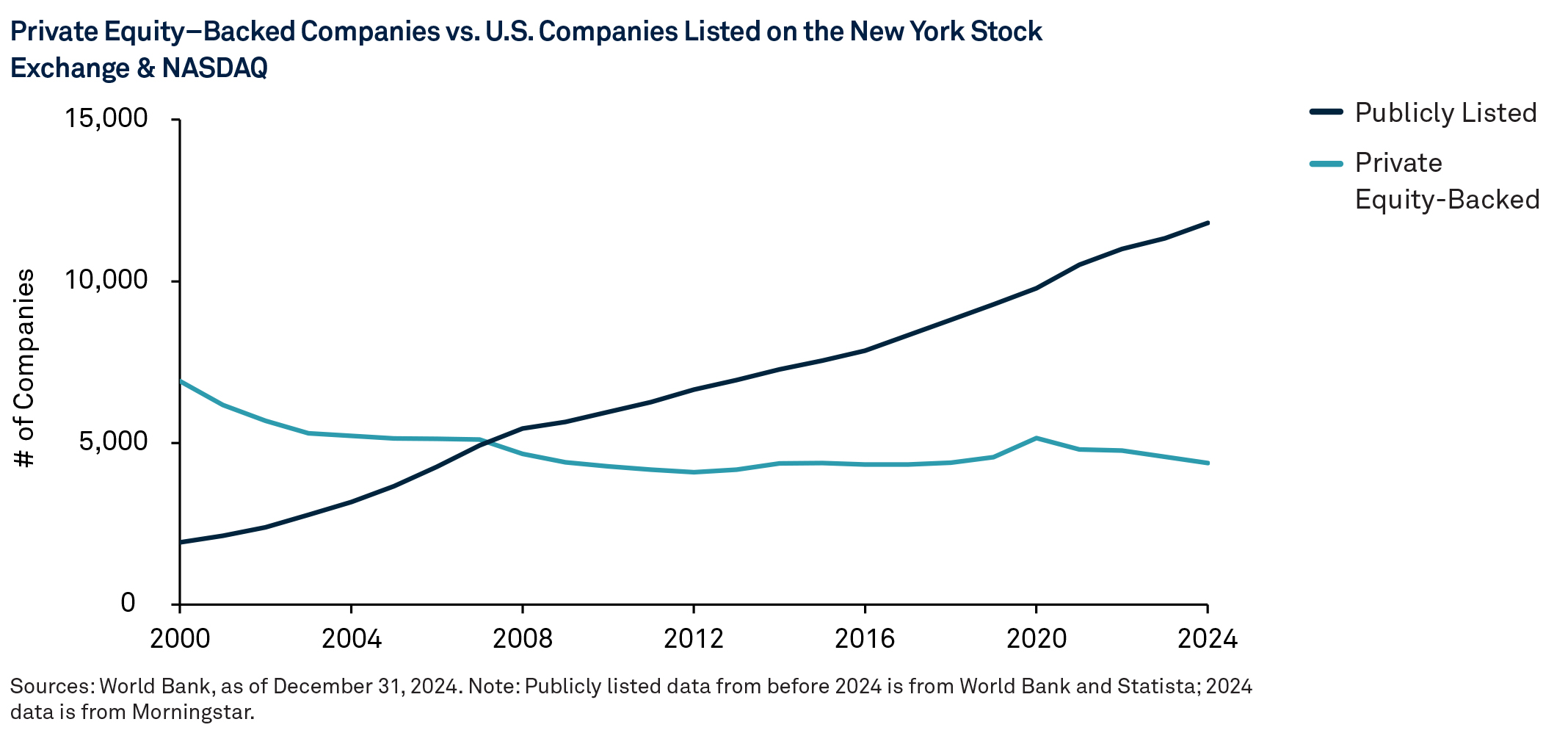

The structural shift in capital formation is reshaping where value is created. More companies are choosing to remain private for longer, allowing more growth to occur before reaching public markets. This shift is reflected in market composition. As of December 2024, there are almost three times as many U.S. companies with private equity-backing than public listings.13 Many firms opt to remain private to retain strategic flexibility and avoid the regulatory burden that comes with a public listing, while maintaining access to capital with potentially favorable terms.

This backdrop has important implications for investors. With fewer companies entering public markets and more value creation happening privately, investors are increasingly looking beyond traditional markets to access the full spectrum of growth opportunities.

Private Markets: Finding Value

With more value creation happening before companies go public, early-stage growth is shifting from small-cap stocks to private investors. As a result, venture capital and growth equity strategies are capturing much of the dynamic opportunity set that once fueled the small-cap premium. This shift has compressed public market returns while expanding access to high-growth potential for private investors.

Within private markets, venture capital continues to thrive -particularly in sectors like technology, health care, and energy. In fact, AI startups captured 53% of all global venture capital dollars in the first half of 2025, with that percentage jumping to 64% in the U.S.14 The post-2021 valuation reset has created a more investor-friendly environment, characterized by higher-quality entrants and more favorable deal terms.

Growth equity complements this trend by targeting founder-led businesses with scalable models in transformative sectors such as technology, health care innovation, and energy transition. By remaining private longer, these companies can scale efficiently before public exposure, allowing investors to benefit from extended growth cycles and stronger return profiles.15

Concentrated Public Markets: Strategies for Risk Management

Meanwhile, public markets are becoming increasingly concentrated. With fewer companies going public, leading stocks now hold a larger share of the market, raising portfolio risk, especially for investors with meaningful exposure to mega-cap names. Hedge fund strategies, particularly long-short equity strategies, can play an effective role in helping investors diversify from crowded exposures while hedging market-wide drawdowns. These strategies can serve as a complementary risk management tool in an environment where public market performance is dependent on an increasingly narrow set of companies.

This is an excerpt from our 2026 report, Capital Market Assumptions: Endurance Under Pressure

For further discussion and in-depth analysis, read the full report.

Past performance is no guarantee of future results

Endnotes

- PitchBook, “AI startups grabbed a third of global VC dollars in 2024,” January 9, 2025.

- The New York Times, “Databricks Is Raising $10 Billion, in One of the Largest Venture Capital Deals,” December 2024.

- The Wall Street Journal, “Anthropic Valuation Hits $183 Billion in New $13 Billion Funding Round,” September 2025.

- Forbes, “OpenAI Valued at $157 Billion After Closing $6.6 Billion Funding Round,” October 2, 2024.

- MetLife Investment Management, “Data Center Investments: A 360-Degree View,” June 2, 2025.

- McKinsey & Company, “AI power: Expanding data center capacity to meet growing demand,” October 2024.

- McKinsey & Company, October 2024.

- Berkeley Lab: Energy Analysis & Environmental Impacts Division, “2024 United States Data Center Energy Usage Report,” December 2024.

- Preqin, “2025 Global Report: Private Debt,” December 11, 2024.

- Preqin, December 2024.

- Global Market Insights, “Asset-Based Lending Market Size Industry Report,” July 2024.

- Global Market Insights, July 2024.

- Apollo Global Management, Inc., Apollo Academy, “Share of public and private companies in the U.S. with revenue greater than $100 million,” April 2024.

- PitchBook, “2024 Annual Venture Capital First Look,” January 6, 2025.

- Apollo Global Management, Inc. “Apollo Asset-Backed Finance Overview,” March 2024.

Important Information

For sole and exclusive use by Institutional Investors, Accredited Investors and Professional Investors only. Not for further distribution. This is a financial promotion and is not investment advice. Any views and opinions are those of the investment manager, unless otherwise noted. The value of investment can fall. Investors may not get back the amount invested. BNY Investments is the brand name for the investment management business of BNY and its investment firm affiliates worldwide. BNY is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole or its various subsidiaries generally. In Hong Kong, the issuer of this document is BNY Mellon Investment Management Hong Kong Limited, which is registered with the Securities and Futures Commission (Central Entity Number: AQI762). In Singapore, this document is issued by BNY Mellon Investment Management Singapore Pte. Limited, Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore (MAS). This advertisement has not been reviewed by the Monetary Authority of Singapore.

GU-794 - 15 February 2027