Q3 2026

QUARTERLY INVESTMENT OUTLOOK

Intelligence for Your Portfolios

Global growth remains resilient but regional divergences are widening as geopolitical strains persist. Central banks remain focused on containing inflation amid ongoing supply shocks. We also expect continued momentum in AI investment. Three factors shape our macro view.

Immediate pressures abate but inventory rebuilds will support commodities demand in the coming months.

Inflation expectations are more fragile, and more frequent price adjustments raise inflation tail risks.

The compute race continues to intensify, forcing leading AI companies to keep raising capex to stay in the race.

We favor selective equity exposure while staying cautious on duration, preferring non-U.S. bonds. Real assets and inflation hedges offer a buffer against geopolitical shocks and supply-driven price pressures.

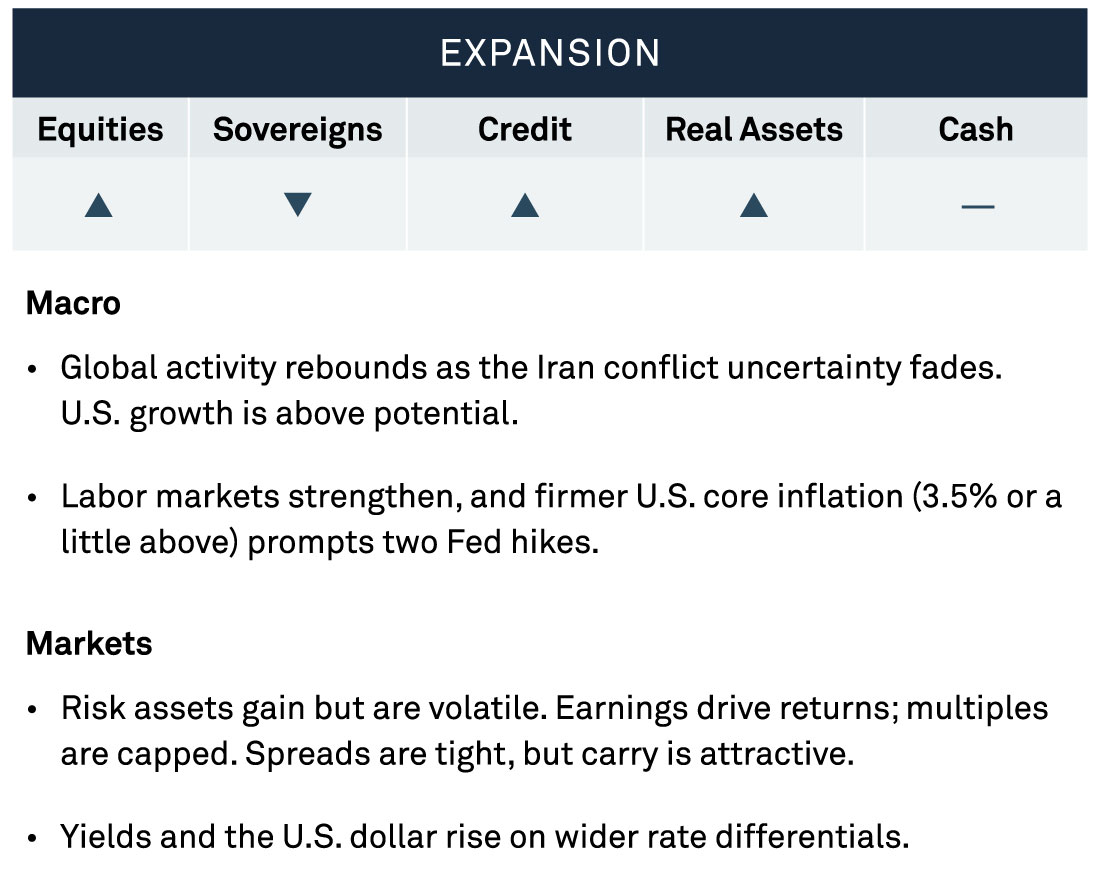

Global activity picks up as Iran-related uncertainty fades, with U.S. growth staying above potential on fiscal stimulus, AI capex, and loose financial conditions. The U.S. core personal consumption expenditures price index (PCE) rises to 3.5% or a little higher, prompting two Fed hikes. In Europe and the UK, their respective central banks hike once.

Risk assets rise but remain volatile as yields drift higher; earnings drive returns, credit spreads stay tight, and the U.S. dollar strengthens modestly.

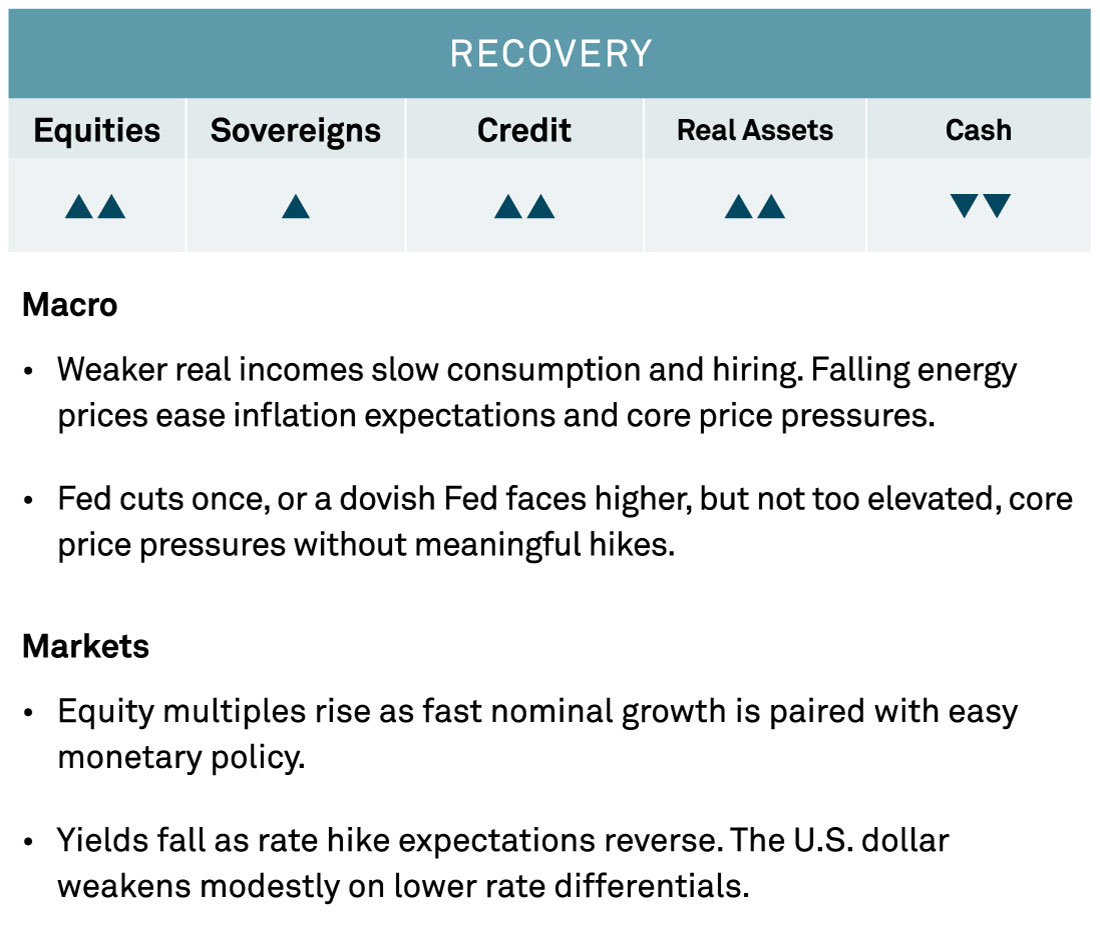

Temporarily weaker real incomes and greater economic uncertainty slow U.S. consumption and hiring. Falling energy prices ease inflation expectations and core price pressures, allowing the Fed to cut rates once or remain dovish despite elevated inflation. The European Central Bank (ECB) and Bank of England (BoE) do not tighten.

Yields fall as central bank hikes are priced out, while the U.S. dollar is stable to modestly weaker as rate differentials narrow.

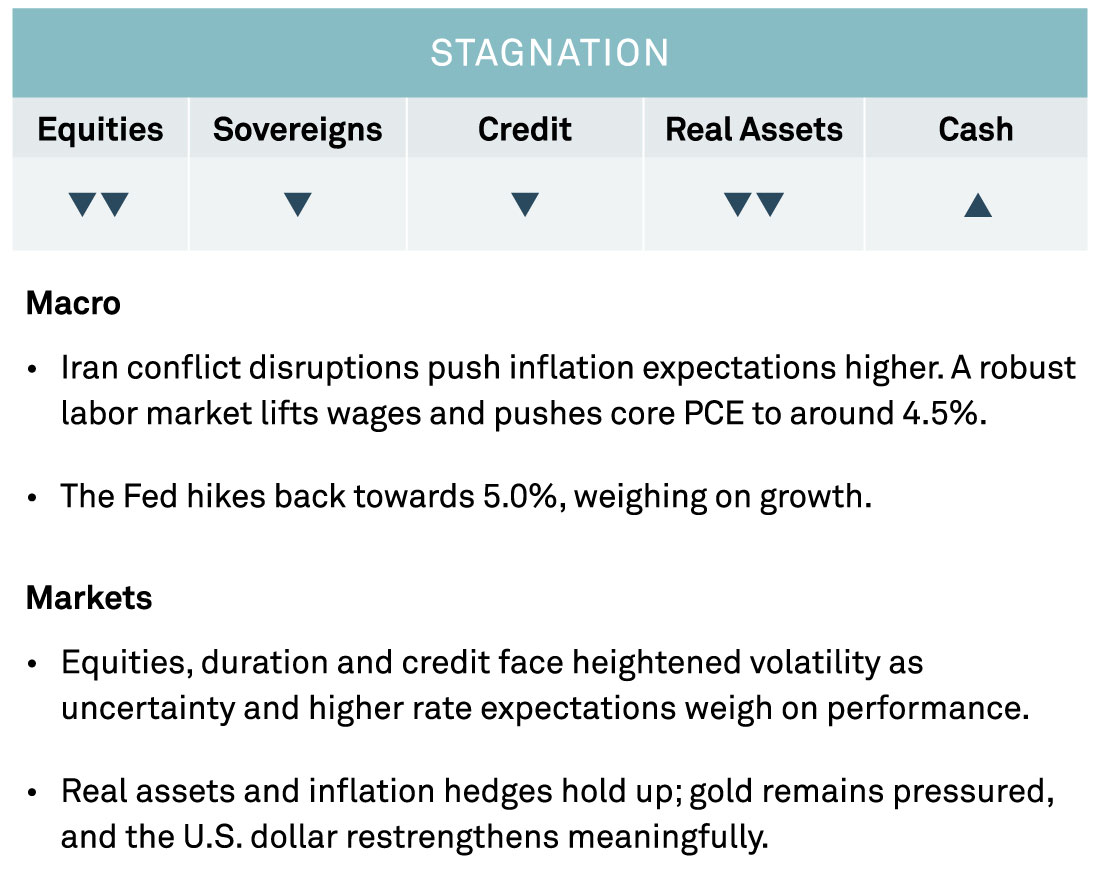

Persistent disruptions from the Iran conflict push inflation expectations higher, while a tight labor market also lifts wages and triggers second‑round effects. This drives U.S. core PCE to around 4.5%, and the Fed hikes back toward 5.0%, weighing on growth. In Europe, the ECB and BoE also tighten, though less aggressively, amid de‑anchoring inflation expectations.

Markets become significantly more volatile as rates reprice higher, pressuring equities, duration and credit. Real assets and inflation hedges outperform, U.S. dollar restrengthens while higher yields weigh on gold.

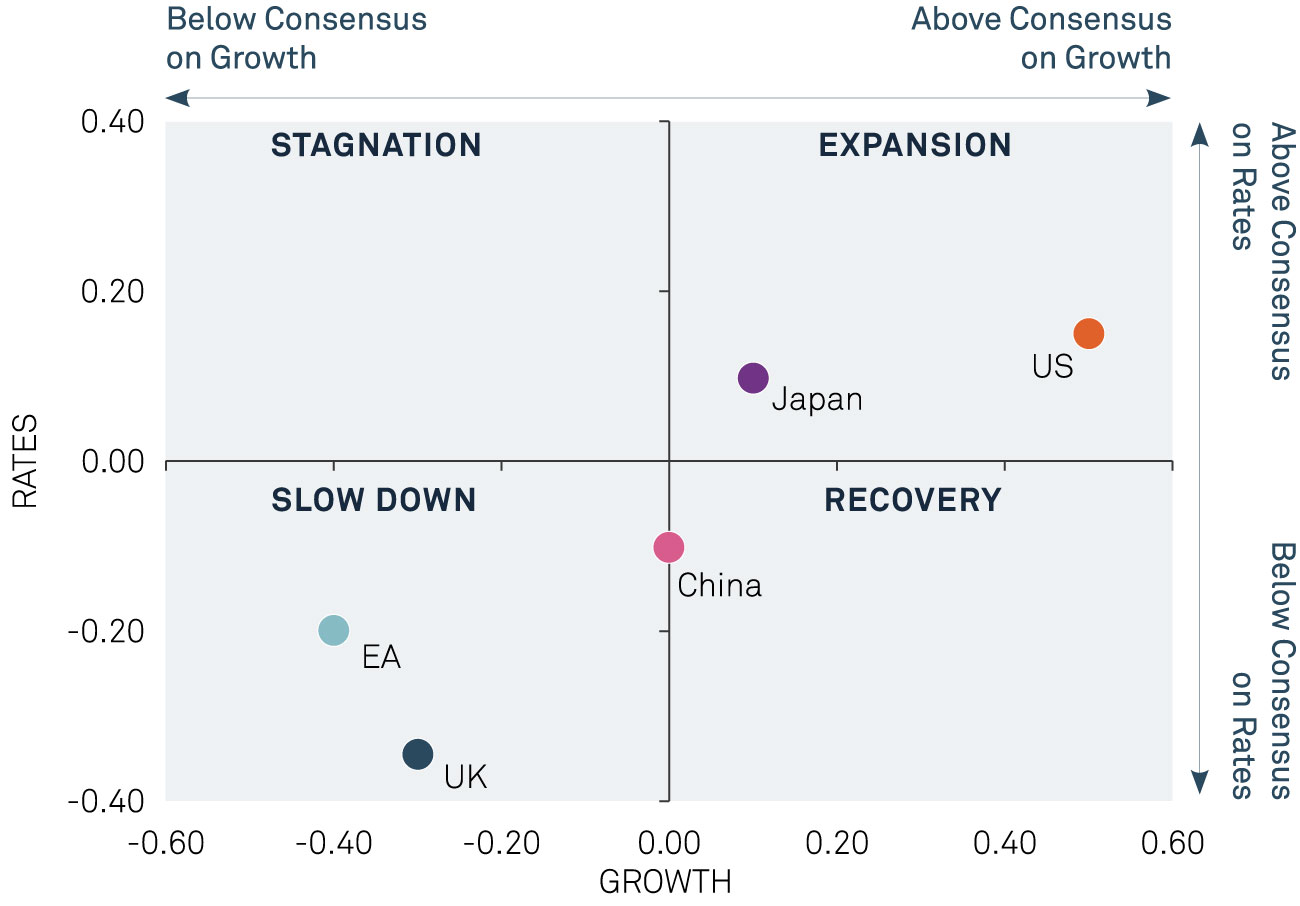

Our global outlook is one of divergence. We expect stronger-than-consensus growth in the U.S. In Europe and the UK, we see weaker-than-consensus growth and fewer rate hikes than anticipated. We are in-line with consensus on growth and rates for Japan and China.

Dive deeper into our asset class positioning and portfolio implications in the full report, where you'll find:

✓ Economic outlook on growth, inflation, and monetary policy

✓ Three scenarios-based forecasts

✓ Key risks we are watching

✓ How our view differs from consensus

Related Research

Endurance Under Pressure

Pressure creates resilience or strain. Our CMAs provide a disciplined, long-term view to help investors build enduring portfolios.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

RISK CONSIDERATIONS

This report has been provided for informational purposes only and is subject to significant limitations. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment. The information contains projections or other forwardlooking statements regarding future events, targets or expectations, and is only current as of the date indicated. Targets contained herein are based upon an analysis of historical and current information and assumptions about circumstances and events that may not yet have taken place and may never occur. If any of the assumptions used do not prove to be true, results may vary substantially. Certain information has been obtained from sources believed to be reliable, but not guaranteed. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. If the reader chooses to rely on the information, it is at its own risk. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. We do not undertake to advise you of any change in the information contained in this report. The report does not reflect actual trading and other factors that could impact future returns. Given the inherent limitations of the assumptions, this report does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. The information has been provided without taking into account the investment objective, financial situation or needs of any particular person. Please consult a legal, tax or financial professional in order to determine whether an investment product or service is appropriate for a particular situation.

Equities are subject to market, market sector, market liquidity, issuer, and investment style risks, to varying degrees. Bonds are subject to interest-rate, credit, liquidity, call and market risks, to varying degrees. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes and rate increases can cause price declines. Commodities contain heightened risk, including market, political, regulatory, and natural conditions, and may not be appropriate for all investors. High yield bonds involve increased credit and liquidity risk than higher-rated bonds and are considered speculative in terms of the issuer’s ability to pay interest and repay principal on a timely basis. Investing in foreign denominated and/or domiciled securities involves special risks, including changes in currency exchange rates, political, economic, and social instability, limited company information, differing auditing and legal standards, and less market liquidity. These risks generally are greater with emerging market countries. Small and midsized company stocks tend to be more volatile and less liquid than larger company stocks as these companies are less established and have more volatile earnings histories. Currencies are can decline in value relative to a local currency, or, in the case of hedged positions, the local currency will decline relative to the currency being hedged. These risks may increase volatility. Alternative strategies may involve a high degree of risk and prospective investors are advised that these strategies are appropriate only for persons of adequate financial means who have no need for liquidity with respect to their investment and who can bear the economic risk, including the possible complete loss, of their investment. The strategies may not be subject to the same regulatory requirements as registered investment vehicles. The strategies may be leveraged and may engage in speculative investment practices that may increase the risk of investment loss. Investors should consult their financial professional prior to making an investment decision.

INDICIES & DEFINITIONS

1-year forward swap: the avg. interest rate for 1-mth. in 1-year forward. 10Y UK Gilt – Average yield of a range of UK government bonds all adjusted to the equivalent of a ten-year maturity. The 10Y US Treasuries Average Yield of a range of Treasury securities all adjusted to the equivalent of a ten-year maturity. Artificial intelligence (AI): refers to computer systems that can perform tasks typically requiring human intelligence, such as visual perception, speech recognition, decision-making, and language translation. Beta: a measure of a security’s sensitivity to market movements, indicating its systematic risk relative to the overall market. Bloomberg US Corporate High Yield: covers the universe of fixed-rate, non-investment grade corporate debt in the US. Bloomberg US Corporate Investment Grade: designed to measure the performance of the investment grade corporate sector in the US 1-mth. The CBOE VIX Index (VIX) is an indicator of the implied volatility of S&P 500 Index as calculated by the Chicago Board Options Exchange (CBOE). Europe STOXX 600 Index represents the performance of 600 large, mid and small capitalization companies across 18 countries in the European Union. Expansion: GDP growth above trend. GDP: gross domestic product is the total monetary or market value of all the finished goods and services produced within a country’s borders over a given time period. Initial public offering (IPO): is the term for the first time that a private company sells shares of its stock to the public on a stock exchange. Japan (Nikkei 225): The NIKKEI 225 is an index that tracks the performance of the largest 225 companies traded in the Japanese market. The Majors Dollar Index (USD) measures the value of the US dollar relative to a basket of currencies of the most significant trading partners of the US including the euro, Japanese yen, Canadian dollar, British pound, Swedish krona, and Swiss franc. The MSCI EM Index (Emerging Markets Equities) tracks the total return performance of emerging market equities. Neutral Rate of Interest (r-star or r*) is the short-term interest rate that would prevail when the economy is at full employment and stable inflation. A rate at which monetary policy is neither contractionary nor expansionary. Personal Consumption Expenditures Price Index (PCE): is a monthly measure of the prices of goods and services purchased by consumers in the United States. Recovery: growth recovering towards long-term trend growth. The S&P 500 Composite Index (S&P 500) is designed to track the performance of the largest 500 US companies. Slowdown: GDP growth slowing below trend. Stagnation: period of slow or no economic growth. US Consumer Prices (CPI) Index measure of prices paid by consumers for a market basket of consumer goods and services. The yearly (or monthly) growth rate represents the inflation rate.

STATISTICAL TERMS

Skewness in statistics represents an imbalance and an asymmetry from the mean of a data distribution. In a normal data distribution with a symmetrical bell curve, the mean and median are the same. Probability-weighted mean is similar to an ordinary arithmetic mean, except that instead of each of the data points contributing equally to the final average, data points are weighted by the statistical probability for a particular scenario outcome. Duration is a measure of a bond’s interest rate sensitivity, expressed in years. The higher the number, the greater the potential for volatility as interest rates change.

OTHER

QE: quantitative easing. Fed: US Federal Reserve. ECB: European Central Bank. BOJ: Bank of Japan. BOE: Bank of England.

IN THE UNITED STATES: FOR GENERAL PUBLIC USE

IN ALL OTHER JURISDICTIONS: FOR INSTITUTIONAL, PROFESSIONAL, QUALIFIED INVESTORS AND QUALIFIED CLIENTS.

Disclaimer

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy. It is intended for institutional and professional audiences and may not be relied upon by retail investors jurisdictions other than the US.

Opinions and views expressed are subject to change without notice.

Past performance is no guarantee of future results.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE |

©2026 THE BANK OF NEW YORK MELLON CORPORATION

MARK-954599-2026-06-18

GU-880 - 30 June 2027