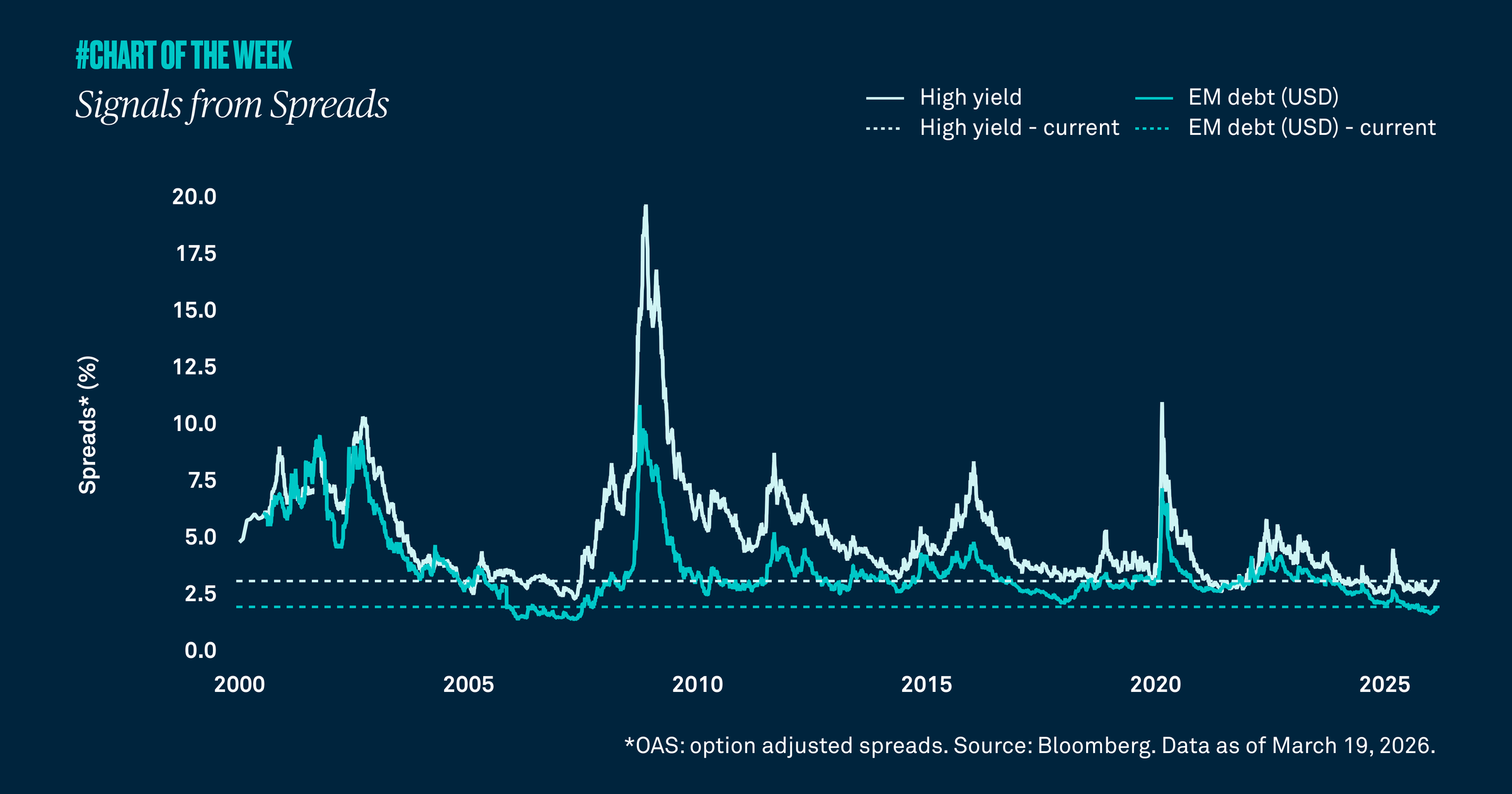

Credit spreads have risen yet remain historically low, reinforcing our view that the oil shock is likely temporary — not a driver of long-term growth concerns.

The Middle East conflict continues but key credit spreads remain relatively subdued. Historically, rising credit spreads signal greater risk aversion and concerns about slowing growth. A sustained widening would indicate more persistent growth concerns.

Similar to the equity market, credit spreads suggest the conflict will likely be short-lived. Though U.S. high yield spreads rose 55 basis points (bps) and emerging market debt spreads increased 30 bps in the last two months, these levels are historically low. We agree with the market and believe the oil shock will be temporary. While recent developments from President Trump on potential negotiations could be positive, the situation remains dynamic, and we’ll continue to watch whether credit spreads widen further.