Financials are calibrated to deliver cyclical offence when you want it and defensive ballast when you need it.

We entered the year with a series of cyclical, structural, and secular tailwinds that we believe could support equity markets in 2026. While these dynamics overall may lift the broader economy and markets, we believe value-oriented sectors are positioned to benefit most — and within that group, financials stand out.

KEY POINTS:

- Financials present a compelling investment opportunity across market cycles, and are currently supported by an alignment of cyclical, structural, and secular tailwinds.

- We believe the sector is poised to benefit from a number of pro-growth actions, including fiscal policy, deregulation, and the broadening adoption of Artificial intelligence (AI).

- By selectively allocating across financial subsectors, we can employ financials to seek to balance offence and defence, enhance diversification, and manage risk across changing market environments.

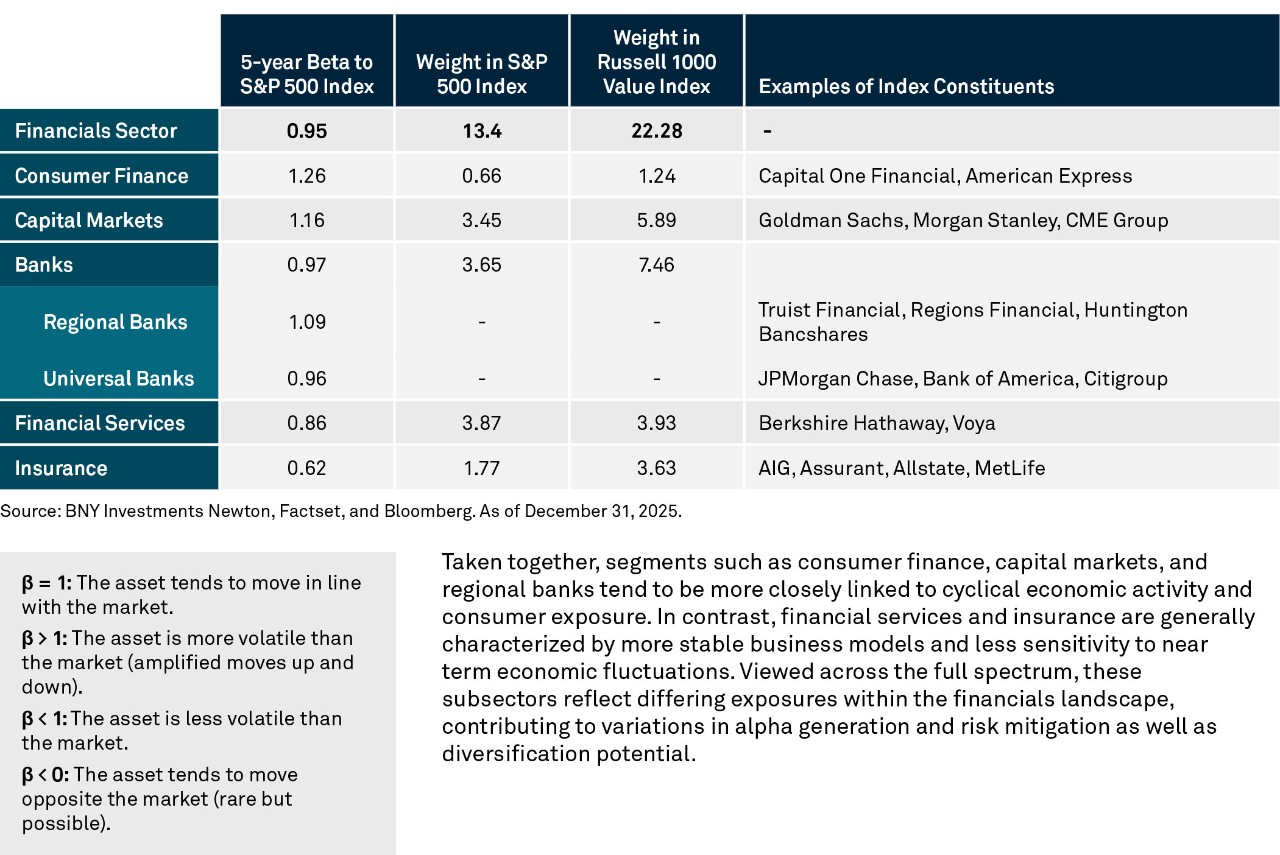

Beyond the immediate investment opportunity, we think the financials sector can play an important role in portfolio construction and risk management, largely given the varied characteristics of its subsectors. For example, US regional banks offer targeted cyclical and consumer exposure, while insurers may provide risk mitigation. Allocating across the financial subsectors may help support a balanced exposure while maintaining individual security selection to drive the best investment outcomes.

FINANCIALS: WHY NOW?

Views on the financial sector have been mixed since the Global Financial Crisis (GFC). Increased regulation and oversight, especially among the banks, has led to higher capital and liquidity standards, more stringent stress tests, and further restrictive rules around proprietary trading via the Volcker Rule. On the insurance side, zero-percent interest rates (ZIRP) weighed heavily on the industry’s ability to generate investment income. While increased regulation and low interest rates were important to help stabilise both the financial sector and the “plumbing” of the global economy, it has impinged on corporate profits and sent investors looking elsewhere to find relatively stronger earnings growth.

Eighteen years on from the depths of the GFC, we believe there are a number of positive tailwinds aligning for the financial sector.

CYCLICAL

Fiscal stimulus and accommodative monetary policy

From a fiscal policy perspective, we believe legislation can have a powerful effect on investment outcomes. On 4 July 2025, President Trump signed the One Big Beautiful Bill Act (OBBBA) into law, which aims to revitalise domestic economic activity by ushering in a series of pro-growth policies. It also reshaped tax policy and introduced meaningful capital incentives to spur investment across key industries. We think certain bank and capital markets-exposed companies may benefit, given their role in powering US infrastructure, and drive capital flows. We believe monetary policy is still relatively accommodative, even if interest rates hold steady through year end. A steep or steepening yield curve should also support net-interest margins for lenders and lead to earnings growth, in our view.

STRUCTURAL

Deregulation

In early 2025, the Trump administration launched an aggressive deregulatory campaign aimed at lowering business costs and accelerating growth. A central pillar was the 6 February 2025 Executive Order “Unleashing Prosperity Through Deregulation,” which requires federal agencies to identify at least 10 existing regulations for repeal for every new one proposed, ensuring the overall cost of regulation declines. The White House later estimated that these actions could lift long-term US economic growth by roughly 0.3% to 0.8% annually and trim inflation by about 0.6% per year if regulatory expansion remains capped for a decade. For financials, we believe the sector will benefit from relaxed post-crisis capital and compliance requirements – freeing up capital to put to better use. We also believe it will lead to an increase in mergers and acquisitions (M&A) activity – not only within the financials sector, which we think would be a healthy development, but across all sectors, which will benefit the banks and capital markets that advise on dealmaking activity.

SECULAR

Broadening out of AI adoption

Artificial intelligence (AI) investing has evolved through three waves, starting with hyperscalers and initial infrastructure build-out, expanding to energy production, transmission and distribution systems, and infrastructure, and now entering widespread adoption across traditional industries. While the first two AI waves favoured large technology companies, the third is reshaping traditional industries and is poised to create new value beyond the technology sector. We are seeing early evidence of transformation in finance and insurance, including lower call centre costs, quicker and better underwriting for loans or insurance policies, and lower loss costs enabled by faster, more thorough credit evaluation.

FINANCIALS: WHY ALWAYS?

Although current conditions are favourable, we believe financials are important in any market, leveraging subsector characteristics for targeted exposure and results. From our perspective, we believe the sector provides ample opportunities to play “offence” when there are strong economic tailwinds or idiosyncratic opportunities and “defence” when the macro environment is less certain or volatility increases.

We believe a robust investment process is anchored in fundamental, bottomup company research and individual stock selection, and should also take into account how each position will interact with other positions within the portfolio as well as the broader market to ensure intended exposure is achieved. This is critical from a portfolio construction and risk management perspective.

A key consideration is a sector’s and the individual company’s beta to the equity markets (using the S&P 500 Index as a proxy). Beta is a statistical measure that indicates how much the price of an individual stock or investment is expected to move in response to fluctuations in the overall market. The table below shows five-year beta and benchmark weights across financials subsectors using the S&P 500 Index and the Russell 1000 Value Index, underscoring the sector’s offence and defence versatility.

FINANCIALS OFFER MULTI-CYCLE OPPORTUNITY

Financials offer compelling investment opportunities, and the current market backdrop is highly supportive with cyclical, structural, and secular tailwinds aligned. After years of post–GFC headwinds from regulation and low interest rates, we believe the sector is poised to benefit from pro-growth fiscal policy, accommodative monetary conditions, deregulation, and the broadening adoption of AI, which is improving efficiency and profitability across banking, capital markets, and insurance. Beyond the near-term upside, financials also offer valuable portfolio construction benefits, as different subsectors provide varying degrees of cyclical exposure and defensiveness. By selectively allocating across these subsectors and focusing on bottom-up stock selection, financials can balance offence and defence, enhance diversification, and manage risk across changing market environments.

Important Information

Asset allocation and diversification cannot ensure a profit or protect against loss.

All investments involve risk, including the possible loss of principal. Certain investments involve greater or unique risks that should be considered along with the objectives, fees and expenses before investing.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

Alpha is a measure of selection risk in relation to the market. A positive alpha is the extra return awarded to the investor for taking a risk instead of accepting the market. The Volcker Rule generally restricts banking entities from engaging in proprietary trading and from owning, sponsoring or having certain relationships with a hedge fund or private equity fund. Artificial intelligence refers to the capability of computational systems to perform tasks typically associated with human intelligence, such as learning, reasoning, problem-solving, perception and decision-making. Hyperscalers are large-scale cloud service providers that offer highly scalable and flexible computing infrastructure to businesses and organisations. These companies operate massive data centres, leveraging advanced networking, storage and computing capabilities to deliver cloud-based services efficiently. ZIRP stands for Zero Interest Rate Policy, a monetary strategy where a central bank (like the Fed) sets nominal interest rates at or near 0%.

The S&P 500® Index is widely regarded as the best single gauge of large-cap US equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. The Russell 1000® Value Index measures the performance of the large-cap value segment of the US equity universe. It includes those Russell 1000 companies that are considered more value-oriented relative to the overall market as defined by Russell’s leading style methodology. The Russell 1000® Value Index is constructed to provide a comprehensive and unbiased barometer for the large-cap value segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics. Investors cannot invest directly in any index.

For Professional Clients only.

The value of investments and the income received can fall as well as rise and investors may not get back the original amount invested.

This is a financial promotion.

Any views and opinions are not investment advice or a research recommendation. In Switzerland for Qualified Investors only. BNY is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally. Issued in the UK by BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. Issued in Switzerland by BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. Issued in Europe (ex-Switzerland) by BNY Mellon Fund Management (Luxembourg) S.A. (BNY MFML), a public limited company (société anonyme) incorporated and existing under Luxembourg law under registration number B28166 and having its registered address at 2-4 Rue Eugène Ruppert L-2453 Luxembourg. BNY MFML is regulated by the Commission de Surveillance du Secteur Financier (CSSF).

3242350 Exp: 20 December 2026