We believe diversifying exposure across equity factors is important in today’s geopolitically fraught and concentrated markets. Historically, the quality factor has added ballast to portfolios.

Key points:

- With investors questioning artificial intelligence’s (AI) impact on a growing array of companies, a focus on fundamentals is paramount.

- History shows that diversifying equity style exposure is important for avoiding over concentration in sectors and factors.

- The quality factor has historically provided stability to portfolios.

AI remains a powerful theme. We don’t believe it is a bubble yet, but it is entering a more volatile phase, and valuations remain elevated.

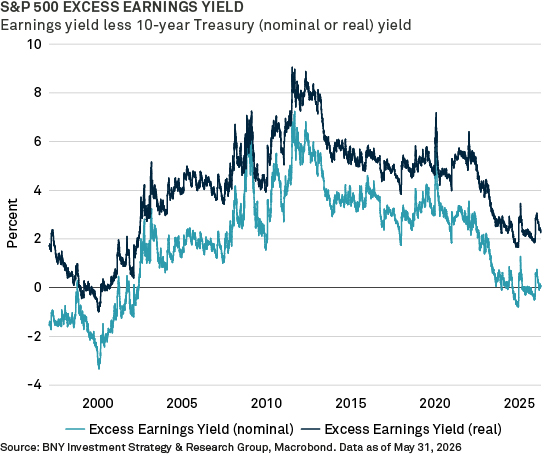

The excess earnings yield (the earnings yield on the S&P 500 over the 10-year Treasury yield) has narrowed since 2012. This suggests stock prices have risen relative to earnings. The nominal excess earnings yield is hovering close to zero, which was also evident around the 2000 tech bubble.

What does history tell us?

Timing a full-blown bubble from a market valuation perspective is uncertain, but history tells us rotations can be sharp.

Rather than aim to time market moves, we believe it is important to diversify equity style exposure and stay invested in quality companies for the long term.

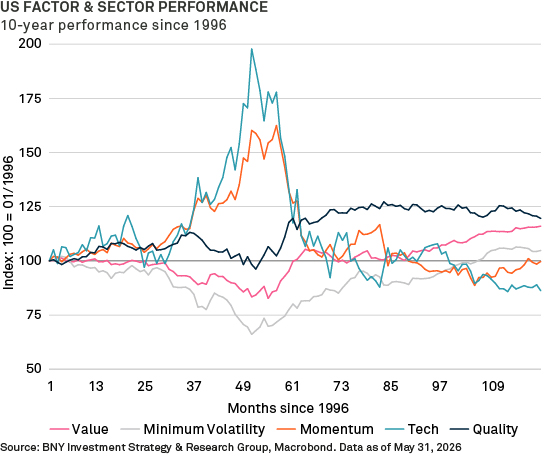

A breakdown of equity style performance around the dot‑com era reminds us why diversification is crucial. It shows that tech leadership can be dramatic – but also reverse quickly.

The chart below shows that from 1996 until after the dot-com bubble burst, the S&P 500 Quality index outperformed each of the S&P 500 Value, Momentum and Tech indexes. As the bubble unwound, quality companies lost less than the other market segments.

Focus on fundamentals

Extrapolating this to today’s markets shows why it is prudent to manage concentration and investment style risk. Over the long term, it matters to focus on company fundamentals and historically, the quality factor has provided ballast to portfolios.

Diversification counts within the AI theme, too. Here there are diverse quality companies, such as chip manufacturers and energy suppliers that are reaping the benefits of the evolution of the technology. But over time, many companies across a host of sectors should benefit from AI, making careful section paramount.

Asset allocation and diversification cannot assure a profit or protect against loss.

IMPORTANT INFORMATION

IN THE UNITED STATES: FOR GENERAL PUBLIC USE. IN ALL OTHER JURISDICTIONS: FOR INSTITUTIONAL, PROFESSIONAL, QUALIFIED INVESTORS AND QUALIFIED CLIENTS.

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy.

Opinions and views expressed are subject to change without notice.

Past performance is no guarantee of future results.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation. BNY Investments is the brand name for the investment management business of BNY and its investment firm affiliates worldwide.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All information contained herein is proprietary and is protected under copyright law.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE |

©2026 THE BANK OF NEW YORK MELLON CORPORATION

MARK-958639-2026-06-29

GU-895 - 5 July 2027