Having the freedom to access credit markets on a worldwide scale offers ample opportunities for active managers to target diversified investment opportunities with an eye to achieving outperformance and building resilience over time. This strengthens the case for incorporating an active approach to global credit within an investor’s portfolio.

A global approach can help weather extreme volatility

The broader opportunity set in a global mandate can offer greater resilience in a financial storm, when compared to a regional allocation.

Looking at the outcomes of various crises that have affected bond markets in the last 20 years, global managers have typically performed comparatively well in the wake of such crises, when compared with regions individually.

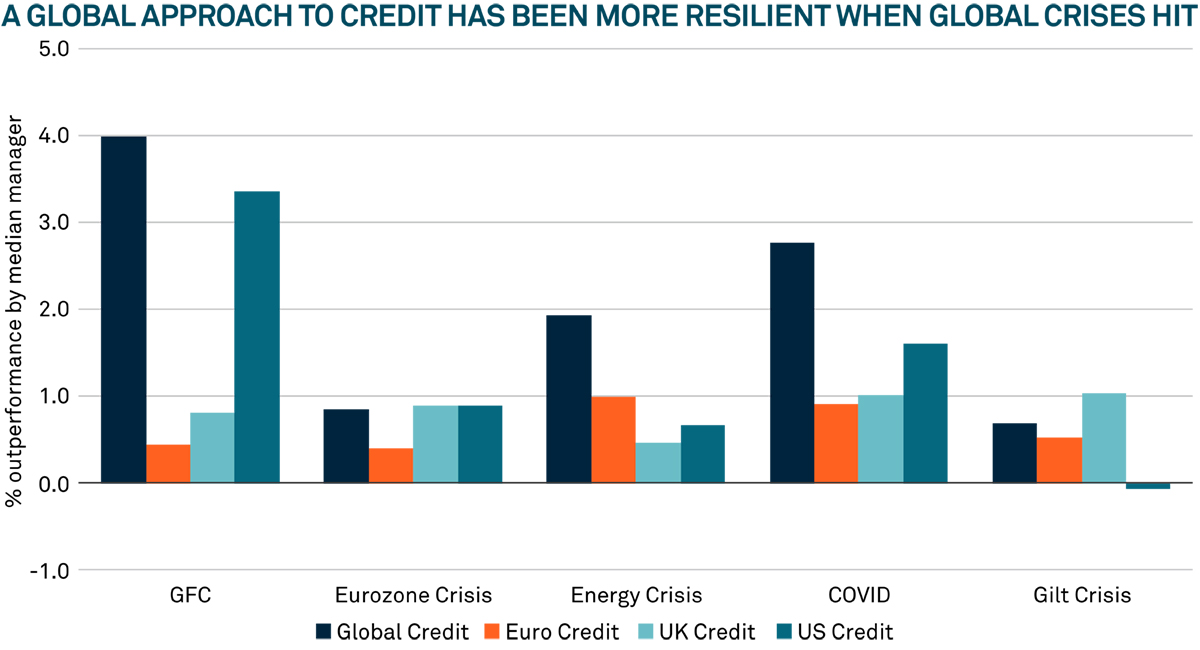

Figure 1: A global approach to credit has been more resilient when global crises hit1

Following the global financial crisis, the 2015-16 energy crisis during which oil prices fell substantially, and the 2020 COVID crisis, the median global manager generally achieved equivalent or better performance relative to their peers than did the median managers of regionally focussed (US, euro and sterling) strategies. The exception was the 2022 gilt crisis, where a global approach was only bettered by sterling credit market specialist approaches.

Broadening access to other sectors and issues can improve diversification and make the most of the market

Adopting an active approach to global credit, which extends flexibility to a manager so they have the freedom to access markets and asset classes beyond a traditional global benchmark, can provide clear benefits. Investing in asset classes such as high yield, emerging markets, asset-backed securities, or loans, can open up extra options to garner additional alpha for portfolios. It also enables a portfolio manager to spread the risk they are taking more widely, potentially allowing them to achieve a performance objective but with the risk taken being more diversified.

Enable active positioning to deliver outperformance

To us, the potential benefits of active management are clear, but how might a global credit manager actually achieve these benefits? There are a number of different approaches for applying active strategies.

First, one can apply credit strategy, including managing portfolio beta. Active managers flex the credit risk in the portfolio relative to the benchmark index. That credit strategy decision may be influenced by where in the credit cycle the market is perceived to be, or what its valuation appears to be relative to history.

Second, credit asset allocation decisions may be driven by considering the macro relative value of related markets, such as positioning in one geographic market versus another. Others may include considering high yield over investment grade, emerging markets over developed markets, or identifying that synthetic markets (such as credit default swaps) appear to be priced differently to physical bonds.

Third, we believe great added value can be achieved through sector strategy. Here, whole industry sectors can sometimes have valuations that do not reflect the current or future strength or weakness of their constituent companies. This is often due to the sector experiencing a slightly differentiated economic cycle than the broader market. Additionally, some industry sectors may become over-leveraged relative to others, making them less attractive to active managers. Importantly, unlike a passive approach, active managers have the flexibility to avoid investing in sectors where they believe the outlook is concerning.

Fourth, security selection can be a key driver of success in active credit management, in our view. Seeking to pick the winners, as we see them, in regions/sectors and avoiding the laggards by applying diligent and detailed fundamental credit analysis. That process aims to identify securities whose valuations do not accurately reflect the company's current and future fundamental strength or weakness. When selecting an issuer's securities, it is crucial to choose those with robust balance sheets and easy access to money markets. Additionally, issuers may need to be stress tested for risks such as litigation, new regulations, environmental or social factors, and potential mergers or acquisitions.

Last, it may be possible to add value through duration and yield curve strategies, or through applying active currency views. Managers can strategically position their portfolios based on their outlook for market yields. If they anticipate a decline in yields, they might add longer-maturity issues, which are expected to benefit the most from such a scenario. More sophisticated strategies may involve targeting specific segments of the yield curve or varying investments across different maturities. A manager may also believe that a currency be unjustifiably undervalued and wish to apply some active risk through that channel.

We believe taking an active approach can be a superior approach over the long term. It seeks to identify where there is excess value that can be captured, or where the expected returns are insufficient given the apparent risks.

We would maintain that the key to achieving consistent outperformance would be to focus on successfully applying credit strategy decisions sector/security selection, where having a well-resourced, experienced, and dedicated credit research team may be able to provide a competitive advantage.

Investment Managers are appointed by BNY Mellon Investment Management EMEA Limited (BNYMIM EMEA), BNY Mellon Fund Management (Luxembourg) S.A. (BNY MFML) or affiliated fund operating companies to undertake portfolio management activities in relation to contracts for products and services entered into by clients with BNYMIM EMEA, BNY MFML or the BNY Mellon funds.

The value of investments can fall. Investors may not get back the amount invested. Income from investments may vary and is not guaranteed.

1Source: Bloomberg. As at 31 May 2025. Recovery is measured as the median manager relative performance in the six-month period ending in: GFC: June 2009, Eurozone Crisis: April 2012, Energy Crisis: August 2016, COVID: September 2020 and Gilt Crisis: April 2023.

2540000 Exp: 31 December 2025