Coming into 2025, the United States economy and global markets were strong with solid labor markets, easing inflation and a stock market boom fueling consumer spending. So far this year, markets have shown continuous change across the global landscape with shifting policy, tariff expectations and international relations driving higher volatility across asset classes. Stock performance in the first quarter was weak for both passive and active investors. U.S. equity markets sold off significantly against bounce backs in Europe and Asia. Positions flipped from short to long EU shares, while U.S. longs flipped to short holdings. Rate cut expectations for the Federal Open Market Committee (FOMC) bounced around during the first half of 2025, with calls for no cuts to more than six. Additional noise from persistent structural deficits and lack of fiscal reform led to the U.S. downgrade from Moody’s (the last of the three agency downgrades), though market reaction was muted. Many investors are questioning the U.S. exceptionalism mantra that characterized markets for over a decade.

Consumer and business sentiment data remain weak, but have yet to reflect recent trade developments. The University of Michigan’s consumer sentiment index is near historical lows1 and small business optimism2 has weakened to its lowest since last October. Investor sentiment dropped to near the weakest in history after the initial tariff announcement on April 2, but has since improved to levels before the trade escalation. CEO confidence fell sharply for several months from the post-election high in January, but was unchanged in April, suggesting the downturn has likely stabilized.3 Overall, while sentiment was impacted by higher policy uncertainty, markets are pricing in a stabilization and sentiment improvement — the extent of which will depend on continued policy clarity and a focus on tax cuts and deregulation.

Our Take

The effective tariff rate has potentially settled to ~13%, which our experts think could represent the target terminal tariff rate of the U.S. administration. The U.S. Court of International Trade (USCIT) ruling last week has created additional uncertainty around final tariff rates, but may not ultimately change the course of tariffs given the alternative pathways to increase trade duties. Still, tariffs remain higher than anticipated and continue to be a drag on economic outlook. U.S. growth is seen as materially slowing from 2024 levels to ~1%, and inflation is expected to pick up to ~3.5%. Additionally, the sustainability of U.S.-China sanctions represents a concern for global growth and inflation, with iFlow data indicating outflows from both economies since January as investors seek alternatives. Market recovery hinges on the speed of potential U.S. tariff deals, with the current 90-day pause in 25% average tariffs providing only temporary relief.

Equities

Given the impact on confidence and freezing of investment plans, our experts' base case remains a non-recessionary slowdown with weak 2025 real GDP growth. Our latest estimate is a 25% chance of recession risk, down from 40% before the China tariff rollbacks. The promise of upcoming trade deals has driven an equity rally from the year-to-date low. Our experts anticipate 2025 earnings to hold up, particularly after a remarkably strong first-quarter earnings season, ending the year with 9% growth. Earnings expectations for 2026 are likely to stabilize with clearer tariff rates and can support S&P 500® Index (S&P 500) levels of $6,100-$6,400 in the next 6 to 12 months.

Lingering risks, including government debt and higher rates, could lead to a renewed pick up in volatility depending on policy developments. While the U.S. has generally underperformed other markets year-to-date (lagging the most since 2017), our experts believe U.S. strategic outperformance will resume.

Rates and U.S. Bonds

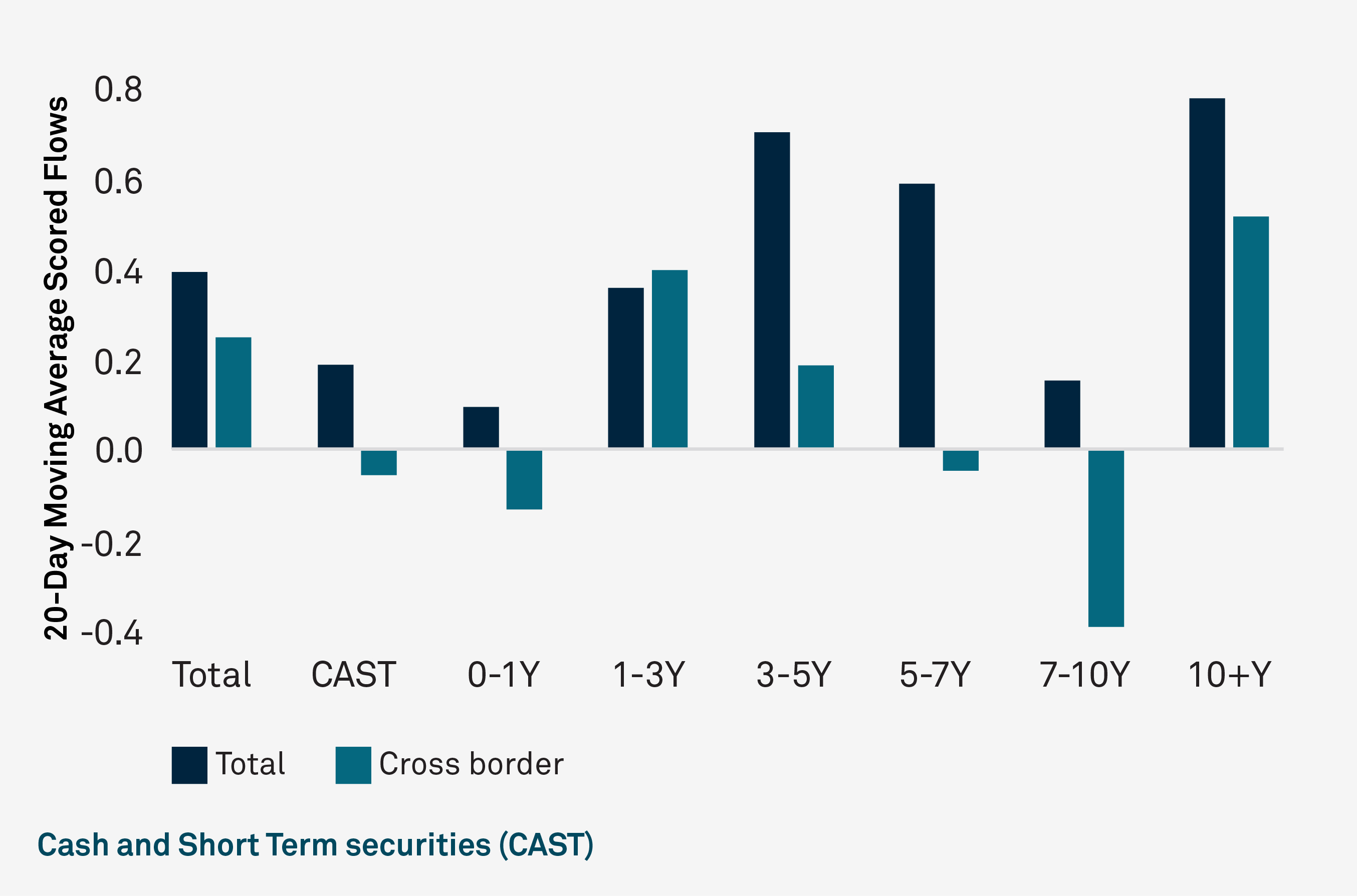

The recent run-up in bond yields and U.S. dollar (USD) weakness from mid-April to mid-May indicate a significant shift in safe-haven perceptions, with U.S. assets no longer commanding their traditional haven status during risk-off environments. BNY’s iFlow data shows foreign investors are reducing exposure to U.S. assets and the dollar, redirecting capital flows toward Eurozone and Japanese government bonds. Post-Liberation Day selling has affected U.S. Treasuries across maturities, alongside broader fixed-income products (Figure 1). Despite financial press speculation, fears of a U.S. Treasury basis trade unwind appear misplaced, as our securities lending data shows this hedge fund strategy remains robust. While U.S. Treasury liquidity faced challenges in early April, trading desk metrics confirm conditions have since recovered. Central bank policy remains on hold, with the Federal Reserve discouraging the idea of a "Powell put" while focusing on containing inflation expectations.

FIGURE 1: TERM STRUCTURE OF U.S. TREASURY FLOWS

Sources: BNY, WM/Refinitiv, Bloomberg. Data as of 5/19/25. Charts provided for illustrative purposes only.

Credit

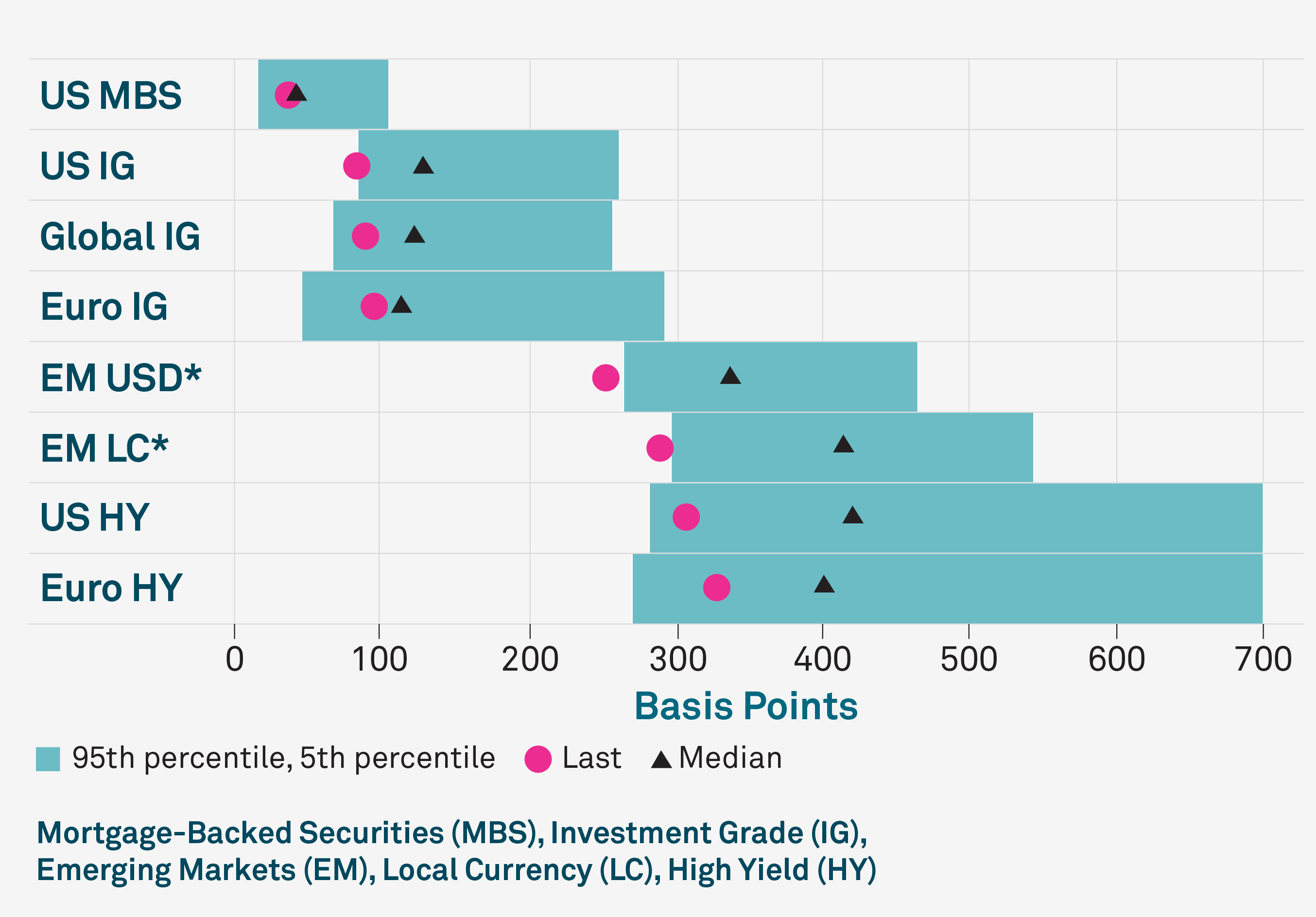

With recent trade policy developments, credit spreads have retraced most of the widening seen since mid-February (Figure 2), heading back to near-historic lows. In the short term, risk appetite may remain supportive, driven by several tailwinds, including resilience in activity data and potentially some improvement in forward-looking sentiment. Additionally, the reduced risk of a U.S.-China decoupling curtails the likelihood of recession, the worst-case scenario for credit investors, and our experts expect other technical factors, such as strong credit demand, to remain supportive.

However, the stagflationary impulse from trade policy remains a concern. Based on our experts’ U.S. outlook, downward pressure on growth and upward pressure on costs and prices is expected. Our experts anticipate the hard data to roll over from the summer as front-loading unwinds and the rise in inflation dampens spending. Though volatility may be expected in the second half of the year, with the risk premium somewhat rising, this can be managed via careful active selection of quality names, international diversification and seeking out relative value opportunities, which will require staying nimble.

FIGURE 2: GLOBAL CREDIT SPREADS

Sources: BNY Investment Strategy and Macrobond. Data as of 5/21/2025. 95th percentile of HY spreads is not shown. *EM debt is shown as a spread vs maturity matched U.S. Treasury yields. Credit spreads referes to the difference in yield between two debt instruments with the same maturity but different credit ratings.

Foreign Exchange (FX)

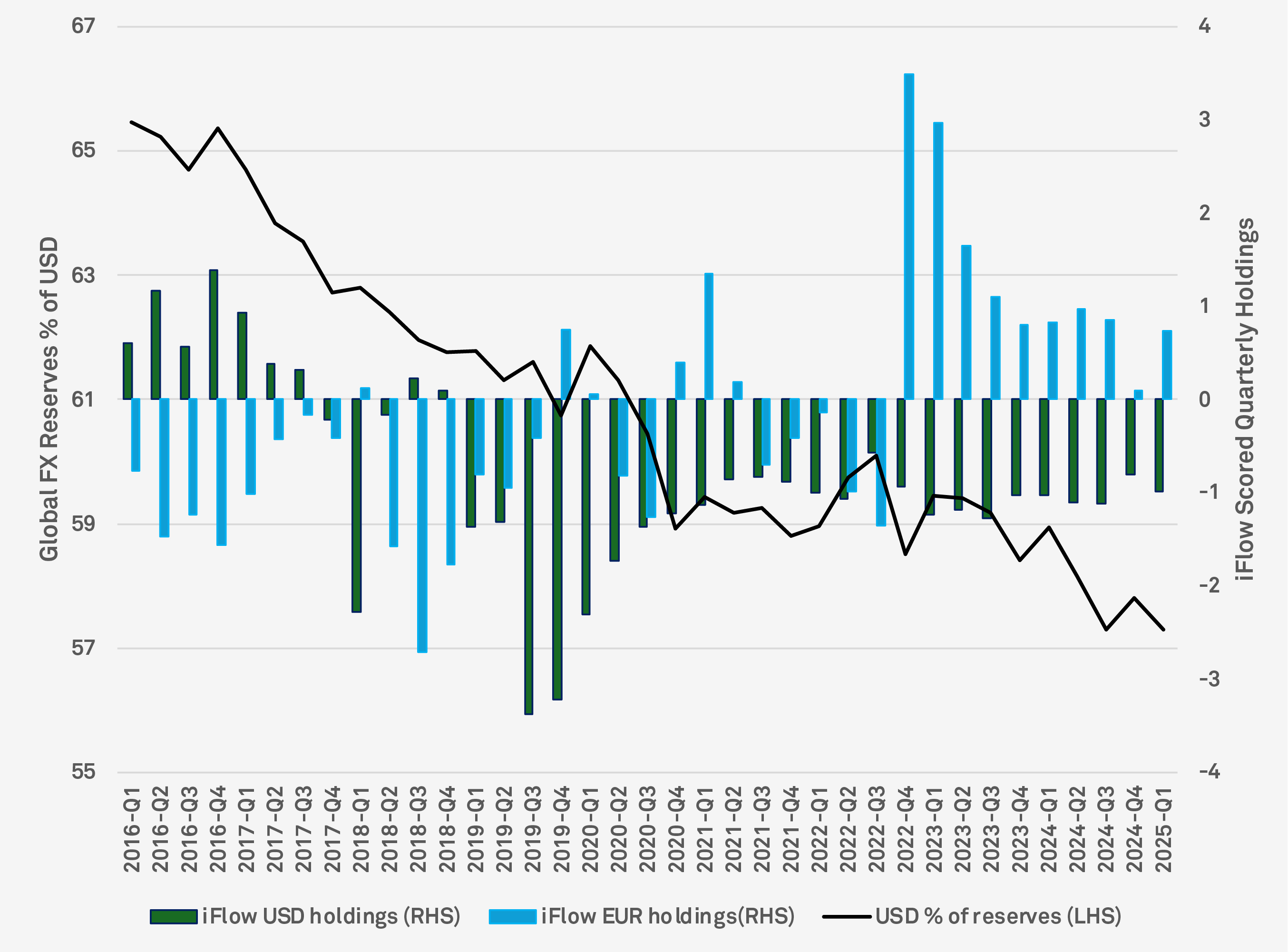

The debate surrounding the USD's status as the world’s reserve currency remains a focal point. Despite its continued dominance, accounting for more usage than all other FX reserve currencies combined, there is a discernible shift towards alternatives like gold and other currency baskets. Notably, the USD’s share of FX reserves has decreased from 65% in 1Q16 to 57% today, marking a 25-year low (Figure 3).

iFlow data reveals a significant reversal in euro (EUR) buying in 2025 , which was near zero at the end of 2024. This trend suggests that investor flows between EUR and USD are more closely tied to economic growth expectations than interest rates or prevailing trends. Despite this shift, the perception around U.S. exceptionalism is evident in dollar hedging and home bias from cross-border flows. FX reserve holdings are increasingly correlated with the volume of USD or EUR held abroad, underscoring the critical role of trade in shaping these dynamics.

The potential for further decline in USD holdings over the coming weeks, months and quarters is influenced by more than just U.S. tariff concerns; U.S. policy and budgetary concerns, the risk premium associated with holding bonds and the volatility of national assets all play a key role. Our experts’ near-term focus will be around U.S. fiscal spending and taxes. The value of the USD and the appetite of cross-border investors to hold U.S. assets have tracked U.S. two-year rates and the S&P 500, but while U.S. asset acquisition is gaining traction, it may no longer carry the label of exceptionalism.

Overall, the potential for an optimistic case exists, where the U.S. remains focused on trade negotiations and decreasing uncertainty, changes in tax and regulation take center stage, and greater policy stimulus from the rest of the world kicks in. One thing is certain: With the rapidly evolving market landscape, our experts think the ability to see through the noise will help investors successfully navigate market swings.

FIGURE 3: USD / EUR HOLDING TRENDS

Source: BNY and International Monetary Fund (IMF) Cofer data (as of 3/30/25), which tracks global FX reserves and is viewed as a link between FX and U.S. bonds and stocks.

Final Thoughts

Overall, we see the potential for an optimistic case, where the U.S. remains focused on trade negotiations and decreasing uncertainty, changes in tax and regulation take center stage, and greater policy stimulus from the rest of the world kicks in. One thing is certain: With the rapidly evolving market landscape, our experts think the ability to see through the noise will help investors successfully navigate market swings.

Bryan Besecker, Eric Hundahl, Alicia Levine, Bob Savage and John Velis contributed to this article.

1 Joanne Hsu, “Consumers Anticipate Rising Unemployment and Elevated Risks of Personal Job Loss,” University of Michigan Surveys of Consumers, May 2025, https://www.sca.isr.umich.edu/

2 William C. Dunkelberg, Holly Wade, “NFIB Small Business Economic Trends,” National Federation of Independent Business, April 2025, https://www.nfib.com/news/press-release/new-nfib-survey-small-business-optimism-declines-in-april/

3 Bloomberg Chief Executive Group, CEO Confidence Index.

Important Information

For sole and exclusive use by Institutional Investors, Accredited Investors and Professional Investors only. Not for further distribution. This is a financial promotion and is not investment advice. Any views and opinions are those of the investment manager, unless otherwise noted. The value of investment can fall. Investors may not get back the amount invested. BNY, BNY Mellon and Bank of New York Mellon are the corporate brands of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally. BNY Investments encompass BNY Mellon’s affiliated investment management firms and global distribution companies. Any BNY entities mentioned are ultimately owned by The Bank of New York Mellon Corporation. In Hong Kong, the issuer of this document is BNY Mellon Investment Management Hong Kong Limited, which is registered with the Securities and Futures Commission (Central Entity Number: AQI762). In Singapore, this document is issued by BNY Mellon Investment Management Singapore Pte. Limited, Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore (MAS). This advertisement has not been reviewed by the Monetary Authority of Singapore.

2527209 Exp: 30 September 2025