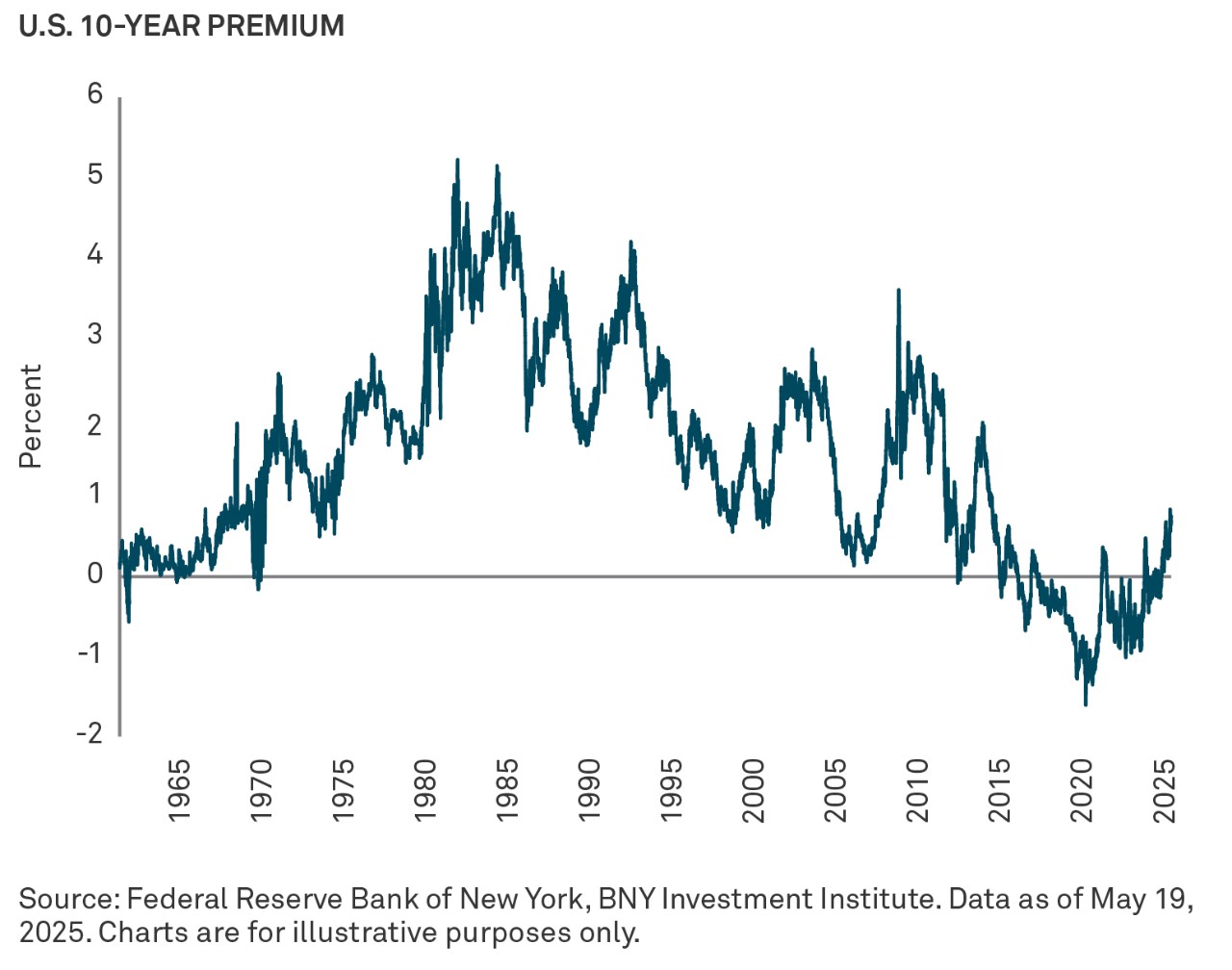

As market interest rates have remained elevated in recent months, alongside high trade policy uncertainty, growth expectations have deteriorated. Our quantitative modeling and macro scenarios suggest that the probability of real interest rates rising above real growth for the U.S. is as high as 50% in 2025 and beyond. If interest rates do rise above growth, fiscal and monetary policies will come under pressure. This is because the deficit will have to be seen as falling for debt to be sustainable in the future. Without a realistic path to fiscal adjustment, a rise in borrowing costs relative to growth could lead to a further, near-term, steepening of the U.S. yield curve.

One for the history books

Moody’s ratings action over the weekend will also be one for the history books — it has had a triple-A issuer rating for the U.S. government since 1949. While the downgrade now takes the issuer ratings down to where S&P and Fitch have already downgraded, respectively, in 2011 and 2023, it underscores the scarcity of “triple-A rated” sovereign securities. To place this in a crosscountry context, currently, only Germany, Netherlands, Australia, Switzerland, Denmark, Sweden, Norway, and Singapore have triple-A ratings from all three major ratings agencies. Canada and New Zealand have triple-As from at least one (but not all) agency(s). But the main point is that the sovereign bonds of these issuers cannot match the scale or liquidity of U.S. Treasury securities.

Countries like Britain and France lost their triple-A ratings several years ago (following the Euro Area debt crisis, and then Brexit), and Japan lost its triple-A by the early noughties (after its asset price downturn, and ballooning government debt, in the 1990s). China’s sovereign ratings are in the mid-to-high single-A space, and the scale of its bond market is approaching that of the U.S. But credit pressures are rising there as well — on intensifying deflation and a worsening quasi-fiscal position. Beijing has, itself, faced issuer ratings downgrades lately —most recently a one-notch downgrade from Fitch in April 2025.

In theory, at least, no issuer or security is totally ‘risk-free’ in an absolute sense. But having a triple-A rating has an aura of unbounded credit quality. When you are rated triple-A it is not possible to measure further credit strength (for instance, there is no quadruple-A or quintuple-A rating). But following the loss of the U.S.’ triple-A status from all three major agencies, the norms around what truly constitutes risk-free securities in a relative sense may come under greater medium-term scrutiny.

Asides from the risk of an entrenchment of term premia, the loss of the U.S.’ triple-A rating may also constrain the ratings of other (e.g.: sub-national and corporate) issuers. This is because sovereign ratings typically act as a ceiling on other debt issuers. In rare cases, these can be pierced — for instance, if the corporation/issuer in question can demonstrate enough credit resilience — large net assets in or cashflows — from offshore sources (and triple-A rated jurisdictions).