The team at Insight Investment1 believes high yield bonds can stay resilient despite ongoing uncertainty, especially through short-duration, active, and globally diversified investing that limits risk while preserving yield.

Key points:

- The investment environment is likely to remain uncertain, with periodic volatility driven by government issuance, political developments, and geopolitical events.

- High yield portfolio resilience can be strengthened through shorter duration and an active, global approach, helping reduce risk while maintaining yield and diversification potential.

- High yield bonds remain supported by a resilient market structure, underpinned by strong technicals, high absolute yields, low defaults, and a solid institutional investor base.

The cycle of uncertainty

Investors today recognise uncertainty not as a temporary disruption but as a defining feature of the post‑pandemic investment landscape. Over recent years, shifting central-bank policy, recurring inflation surprises, geopolitical shocks and unstable cross‑asset correlations have repeatedly triggered short‑lived episodes of volatility. Yet these episodes have followed a broadly consistent pattern.

Market stress typically leads to brief periods of spread widening before supply and demand dynamics reassert themselves. Elevated absolute yield levels continue to attract investor demand, while new issuance remains concentrated on refinancing, limiting net supply growth. This demand-supply imbalance gradually tightens yields as volatility eases.

Persistently high yields have shaped investor behaviour. The opportunity cost of remaining underinvested or attempting to time entry points has been significant, encouraging investors to establish core allocations and add selectively during periods of volatility. Rather than a need to de-risk, volatility increasingly serves as an opportunity to incrementally increase exposure.

Barring a serious recession, we see little reason for this pattern to change in the near term.

Building resilience in high yield bonds

We would highlight several ways that a portfolio can build resilience into high yield bond investments.

Shortening duration: The relatively flat structure of credit curves means that investors are able to capture the majority of the opportunity in high yield bonds with a short-duration strategy. This approach limits interest rate and spread risk, which should help to protect investors from upward shifts in the credit curve.

Deep engagement with management: We believe it is crucial to have a deep understanding of the business plans of the companies we invest in, maintaining regular contact with management to ensure their plan is progressing as expected. This active engagement is critical during economic turbulence, ensuring that investments remain resilient to the prevailing conditions.

Focusing on defensively domestic companies: Many high yield companies operate solely within their domestic market, making them less susceptible to higher transport costs and international tariff risks. By concentrating on companies with predictable, resilient cash flows- such as telecom providers, whose services remain essential even in downturns- we build portfolios designed to withstand economic volatility.

Search out localised resilience within global firms: The mid-sized nature of many high yield companies means they often operate in close geographical proximity to their customer base even when operating internationally. High yield companies are generally not international giants with extended global supply chains. We believe this should help to insulate companies from higher energy prices or changes in tariffs which are only applicable to the cross-border flow of goods.

Avoiding elevated risk in CCC-rated bonds: The companies within high yield bond markets that generally need growth to sustain their business models are those with the greatest leverage. These companies are primarily found in the CCC-rating category.

Expanding geographic horizons: In the hunt for strong domestic franchises, we believe now is the perfect time to broaden the search. With appropriate expertise, many such opportunities can be found in the developing world. These companies, which issue debt in US dollars, often dominate their domestic market but their developing market status means they trade at a yield premium. Telecom providers in Latin America exemplify this dynamic.

Look for regional and country-level support: Some regions or countries may pursue pro-growth strategies that provide a positive environment for high yield companies. For instance, the relaxation of the German debt brake to allow greater defence spending, alongside a new €500bn infrastructure investment fund, is expected to boost growth across the eurozone and with it the outlook for high yield companies operating within the region, especially in sectors such as chemicals, building and even autos.

Take advantage of forced sales to optimise entry points: Some investors will inevitably react to any increased uncertainty by selling their high yield bond holdings. This is particularly true for ETFs where index sales don’t take into account relative value or differences in fundamentals. If issues are sold into volatile markets, they may be at prices well below where they would trade under normal market conditions. This can present opportunities to purchase high-quality issuers at levels which should provide a buffer against further volatility for those who can hold to maturity.

High yield bonds continue to withstand market crises

Ultimately, high yield bond markets have weathered various crises over the last few decades, including the pandemic and the recent surge in interest rates. As a result, high yield companies have gradually improved governance processes to increase resilience during periods of adverse economic and market conditions.

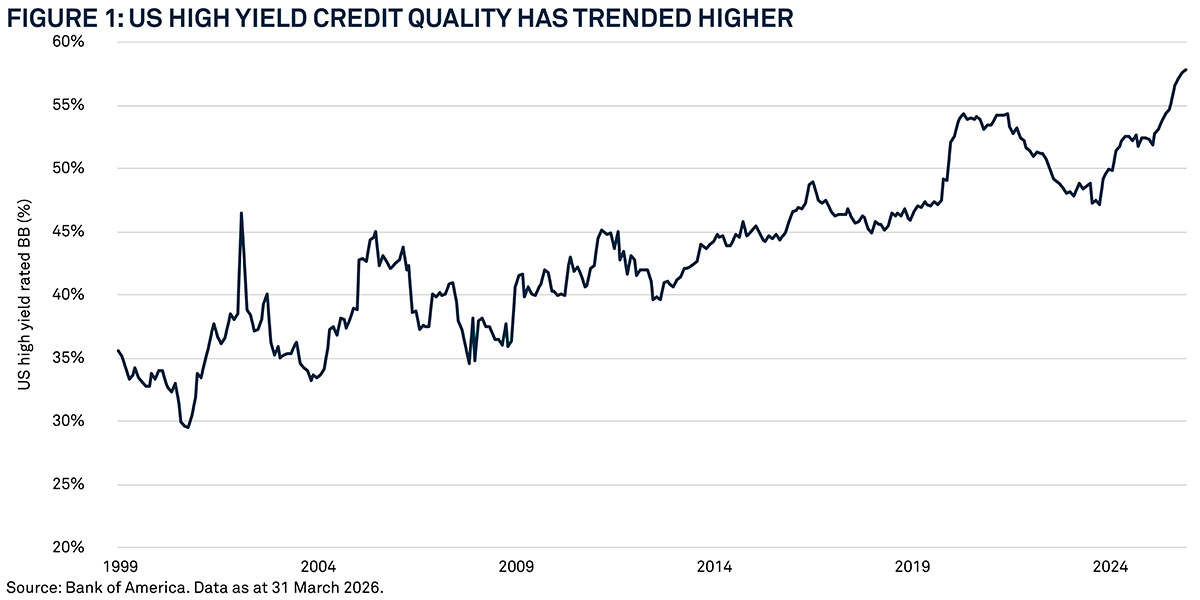

One consequence of this has been a significant improvement in the aggregate credit quality of the global high yield bond market. In the US, for example, nearly 58% of the market held the highest BB rating at the end March 2026. This has consistently trended upward from a low of 29.6% in 2001.

Analysis of leverage data further underscores this improvement; this measures the level of debt a company has relative to its earnings before interest, taxes, depreciation and amortisation (EBITDA). In the US high yield bond market, for example, net leverage has edged up from the lows reached in 2023 but, at 3.8 times, remains below the 10-year average of 4 times.

The technical backdrop remains strong

In recent years, high yield bond markets have been bolstered by a strong technical foundation, primarily due to an evolution in the underlying management of high yield companies.

Management teams are often executing clearly defined growth plans, managing rapidly growing businesses with specific objectives. Securing certainty of funding has become a critical element of this planning, allowing them to remain focused and undistracted by volatility within credit markets. The pandemic reinforced this mindset and we see no signs of it changing.

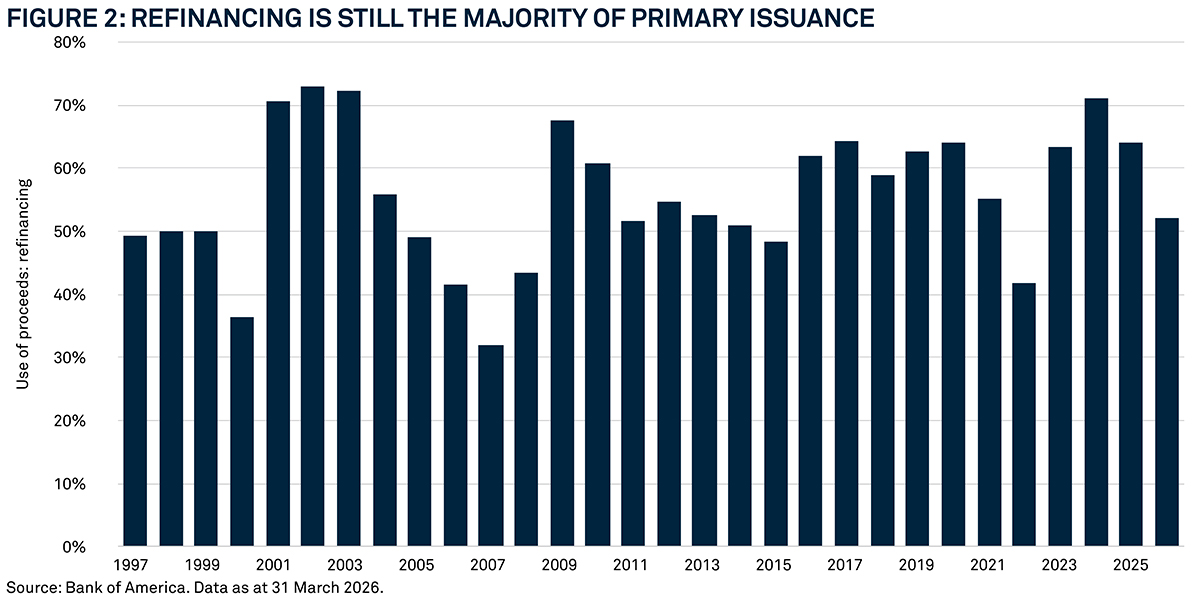

As a result, companies are proactively managing their maturity profiles, refinancing debts well ahead of schedule to secure funding certainty. This often results in existing bonds being called early at a premium, benefiting existing investors. Although there was a dip in Q1 2026 to 52%, the majority of primary issuance continues to be refinancing activity.

With high absolute yields attracting inflows to the asset class, and limited new supply, we believe the asset class will benefit from demand as investors seek out paper in which to invest subscriptions, coupons and maturing or called debt.

Defaults are running at low levels

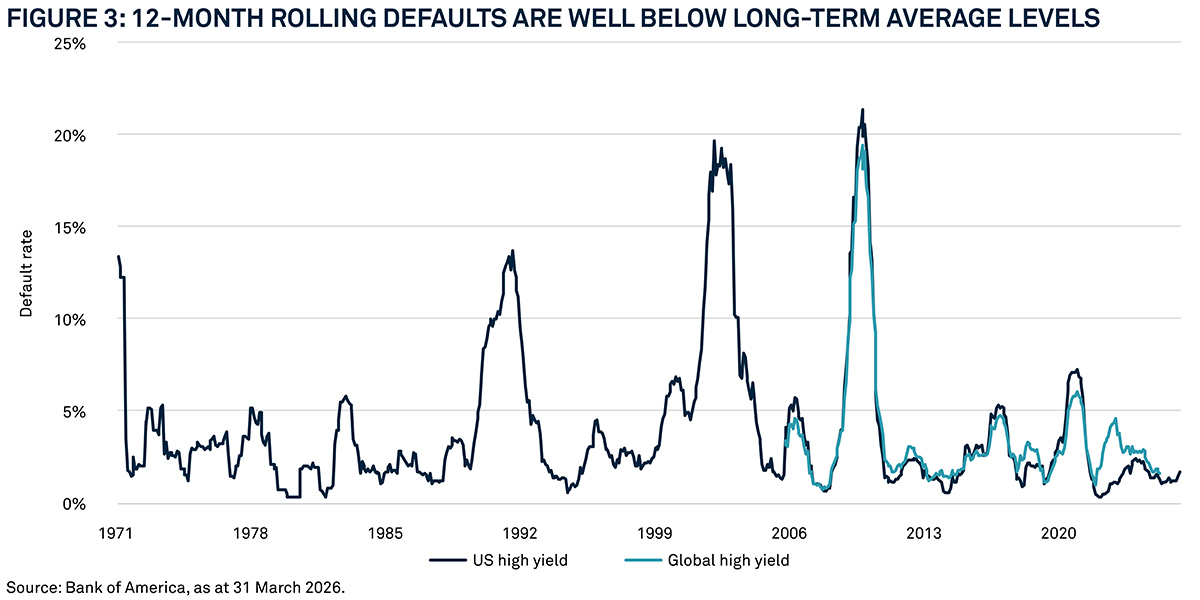

Across key metrics – ratings, total debt/EBITDA (leverage), and EBITDA/interest expense (coverage) – credit quality has markedly improved. This has translated into lower defaults and the expectation that defaults will remain low. The average rolling 12-month default rate for US high yield bonds has been 4.4% over the past 25 years.

At the end of March 2026, the default rate stood at just 1.7% for the US and 2.1% globally, both well below the long-term average. This reinforces our view that global high yield bond markets are significantly more resilient than in the past.

A longer-term investor base

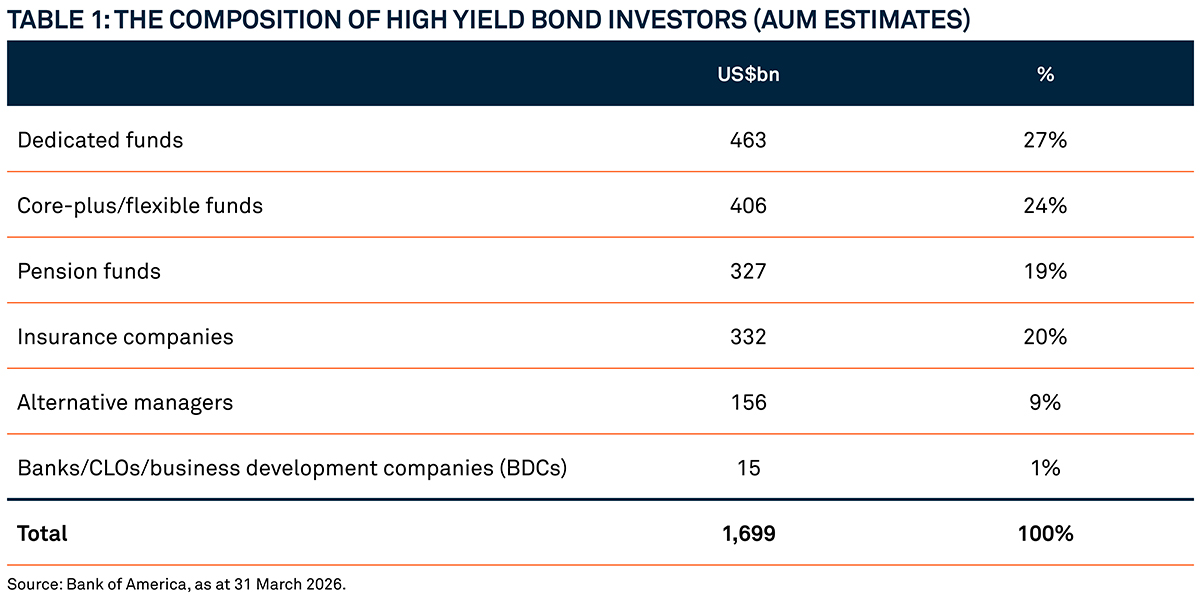

A decade ago, the high yield bond market was dominated by retail investors, which increased the volatility of the market. At the end of March 2026, pension funds and insurance companies directly own 39% of the market, much of which will be dedicated long-term allocations to high yield bonds.

Many other institutional investors will hold the asset class within either dedicated high yield bond funds, or core-plus or flexible funds, which can strategically allocate to the asset class. This large institutional investor base increases stability, and the high absolute level of yields, improved credit quality and low level of defaults makes us confident that institutional investors will continue to flow towards the asset class.

Conclusion

We believe investing in global short-dated high yield bonds is a way to capture credit risk premium while limiting duration exposure. By reducing interest‑rate sensitivity, it avoids unnecessary complexity and delivers a potentially attractive, transparent carry profile. An active manager can seek to enhance this further with high‑conviction investments.

We believe such strategies could be well suited as a core allocation, allowing investors who wish to express other views, such as duration, to do so separately through more targeted instruments or strategies.

The value of investments can fall. Investors may not get back the amount invested. Income from investments may vary and is not guaranteed.

1 Investment Managers are appointed by BNY Mellon Investment Management EMEA Limited (BNYMIM EMEA), BNY Mellon Fund Managers Limited (BNYMFM), BNY Mellon Fund Management (Luxembourg) S.A. (BNY MFML) or affiliated fund operating companies to undertake portfolio management activities in relation to contracts for products and services entered into by clients with BNYMIM EMEA, BNY MFML or the BNY Mellon funds.

3312852 Exp: 6 November 2026