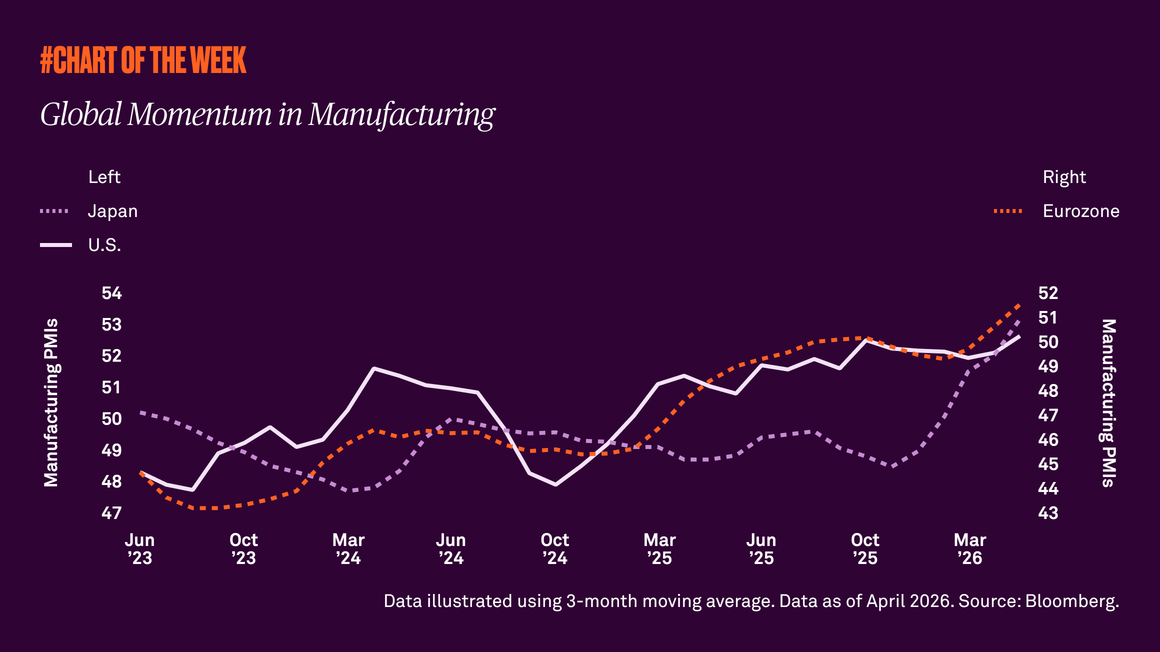

April PMIs (Purchasing Managers’ Indices) point to a meaningful improvement in global manufacturing momentum, with the U.S., Eurozone and Japan all posting stronger-than-expected and firmly expansionary results. The breadth of the rebound suggests improving global demand, supporting a constructive outlook for growth despite ongoing geopolitical tensions.

In April, the U.S. manufacturing PMI rose more than expected to 54.0, its highest level in four years and a firmly expansionary reading. The PMI tracks changes in business conditions across the manufacturing sector, making it a useful gauge of the sector’s overall health and direction. Because purchasing managers tend to see shifts in supply, demand and production plans early, the index is considered a leading indicator of economic activity.

However, the improvement was not confined to the U.S. In the Eurozone, the manufacturing PMI also rose more than expected to 52.2, its strongest reading since May 2022. Japan’s manufacturing PMI likewise advanced to 54.9, the highest level since January 2022. Taken together, these readings suggest that manufacturing activity is strengthening across several major economies at the same time.

That breadth matters. Manufacturing recoveries that occur simultaneously across regions tend to be more durable because they reflect not just local factors, but improving global demand. We view the latest PMI data as constructive. These readings suggest that, despite the ongoing war in the Middle East, momentum in the goods-producing side of these economies is building rather than fading.