Key takeaways

- In the wake of the U.S. and Israeli strikes on Iran, a moderate disruption to global energy price stability would occur if primarily Iranian crude exports are impeded and oil spikes to ~$80-90 per barrel.

- A material disruption could occur if the conflict continues to widen to other energy producing countries and transit through the Strait of Hormuz is significantly disrupted, lifting oil to above $100 per barrel for a sustained period of time.

- Every $10 per barrel increase in the price of oil, if sustained for up to a year, can start to lower global GDP growth by 10-20 basis points (bp)i.

- The U.S. is somewhat insulated by domestic oil production. A sustained $10 a barrel increase trims about 3-5 bp from baseline U.S. GDP growth.

- We remain overweight on precious metals and commodities. Meanwhile, U.S. Treasuries and the U.S. dollar might regain some of their ‘safe haven’ properties. Risk assets appear vulnerable to a downward repricing.

The U.S. and Israeli strikes on Iran, resulting in the death of certain members of Iran’s leadership, are serious developments for regional political and global energy price stability as they could set off moderate to material demand-supply imbalances.

Moderate Disruption Scenario

A moderate disruption would be one in which primarily Iranian crude exports, which total around 2 million barrels per day (mb/d), are impeded.

The current conflict with Iran is already more serious than what occurred in June of last year, when Iran’s nuclear sites were targeted and the Iranians and Israelis exchanged missile attacks. At that time, oil market implications were muted – with Brent crude prices rising from $61/barrel to $80 before slumping back to $70 when a cease-fire was announced.

We think that if Tehran adopts a more practical and less theocratic stance, it could reduce the chances of a long-lasting or escalating conflict in the region. The regime’s long-term survival also depends on sound economics, including stable external relations, which can set the stage for a revival of oil production and exports – a key source of jobs, fiscal revenue, and foreign currency liquidity.

A relatively benign scenario would include a less confrontational stance by Tehran and a shift toward normalcy. That could limit the scale and duration of any price shock. For instance, if oil prices rose to $80-90 per barrel for only a few months and then fell back – the limited shock of this scenario could be absorbed by the global economy.

Higher oil prices are like a tax on consumption and lowers real disposable incomes. But a limited shock can be offset by fiscal interventions and, to a lesser extent, by monetary responses without destabilizing the cyclical upswing underway at many major economies.

Material Disruption Scenario

A material disruption could arise if serious impediments to energy shipments through the Strait of Hormuz continue for an extended period of time, especially with the conflict widening to Iran’s other energy producing neighbors in the Persian Gulf.

The Strait of Hormuz is crucial for 20mb/d of oil shipments. Saudi Arabia, Iraq and the UAE together exported 13.3mb/d of oil via the Strait last year. China and the rest of Asia are the main destinations for Persian Gulf oil – accounting for 80% of total flows through the Strait. The International Energy Agency (IEA) estimated last year that only 3.5-5.5mb/d of the oil that flows through the Strait can be redirected using existing pipeline capacitiesii. The U.S. can release around 1-2mb/d from its strategic petroleum reserves for some time.

In this scenario, oil prices could rise to well over $100 per barrel, and stay elevated for a while, as it did in 2022 following Russia’s invasion of Ukraine.

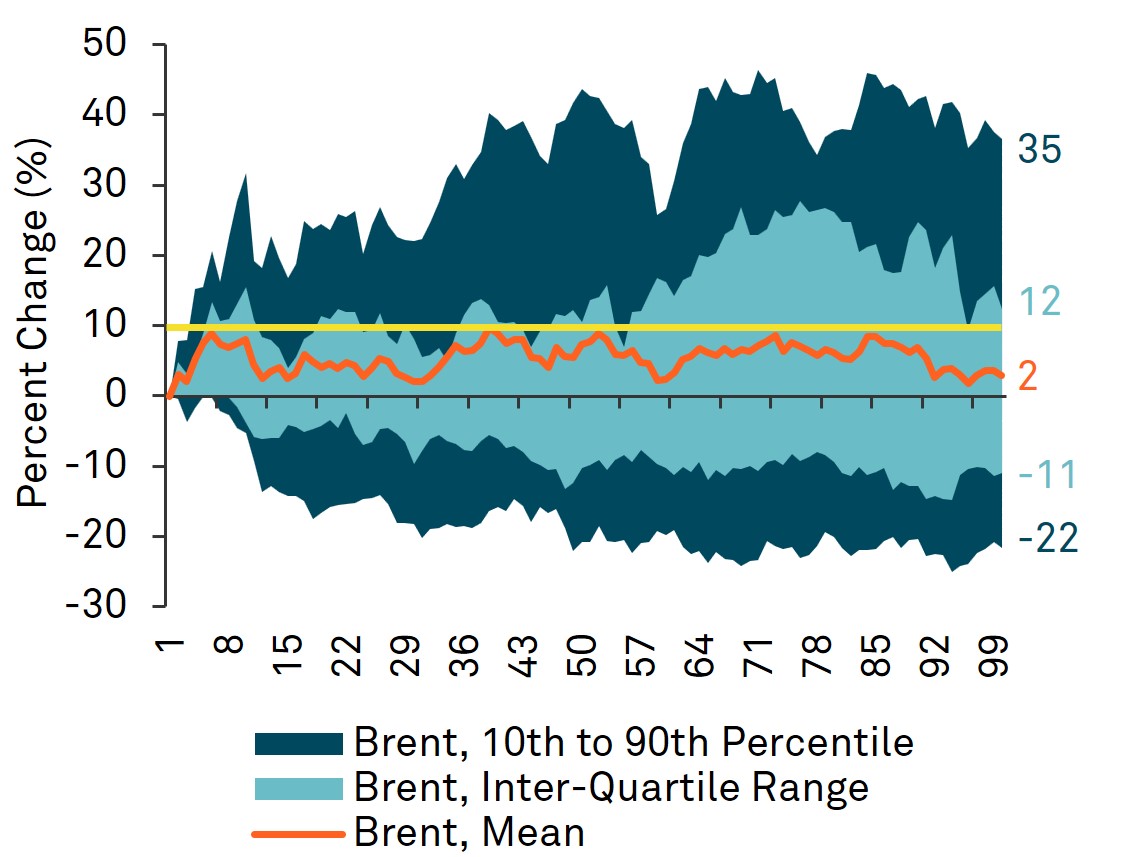

Chart 1: Extreme disruptions can raise crude oil prices by more than 40% in less than 100 days following onset of geopolitical shock; but the mean increase tends to stay below 10%.

Brent Crude Oil Prices in Next 100 Days After a Major' Geopolitical Event

Percentage change from a pre-event level of crude price.

Chart reflects the average changes 100 days onward from a number of geopolitical events including the Gulf War (Aug. 1, 1990); September 11 attacks (Sept. 11, 2001); U.S. invasion of Iraq (March 19, 2003); Israel's invasion of Lebanon (June 11, 2006); Arab Spring Revolt (Nov. 30, 2010); Russia's invasion of Ukraine (Feb. 23, 2022); Hamas attack on Israel (Oct. 7, 2023).

Impact on Global Growth

Macroeconomic sensitivities are key in framing the impact of geopolitical shocks. For instance, every $10 per barrel increase in the price of oil, if sustained for up to a year, can start to lower global GDP growth by 10-20bp . If oil prices were to spike to $120-150 per barrel and stay elevated (like in 2022), the world economy could be significantly impacted.

U.S. growth, however, is more insulated due to domestic production of oil. It is estimated that every $10 per barrel increase in the price of oil detracts around 3- 5bp from a baseline level of U.S. growth.

What to Expect in the Short Term

We think short-term disruptions are likely to persist. But we lean towards more benign outcomes in the coming few weeks. We believe there is less appetite in the U.S. for foreign entanglements or voter tolerance for a renewed oil price spike. Appetite for a prolonged conflict in Israel or at the Gulf Arab countries also seems quite limited, in our view. Moreover, in a post-Khamenei setting, any new government in Iran could be more amenable to an alteration in terms of its foreign relations if it implies better odds of a post-Khamenei regime survival and economic revival.

Asset Class Impact

We remain overweight on precious metals and commodities which continue to provide a hedge against geopolitical upheavals and stagflationary risks. U.S. Treasuries and the U.S. dollar might regain some of their ‘safe haven’ properties.

However, risk assets appear vulnerable to a downward repricing against what was already an uncertain backdrop – with artificial intelligence (AI)-related disruptions, and unsettled questions around the U.S. government’s trade policies and Federal Reserve appointments.

Until there is more clarity about the contours of any new (or old) political regime in Iran, and any re-orientation of its foreign policy approach, risk assets could remain under pressure.

Credit spreads are poised to widen, equity multiples could come under pressure and market pricing of policy rates may be biased to drift higher – if the market looks ahead to the reality of major central banks being more alert to inflation and willing to hike rates in response to a negative energy shock.

Endnotes:

i International Monetary Fund (IMF), World Economic Outlook, October 2023

ii International Energy Agency (IEA), Strait Of Hormuz Factsheet, February 2026

iii International Monetary Fund (IMF), World Economic Outlook, October 2023

Artificial intelligence (AI) refers to computer systems that can perform tasks typically requiring human intelligence, such as visual perception, speech recognition, decision-making, and language translation.

Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period.

Disclaimer

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy.

Opinions and views expressed are subject to change without notice.

Past performance is no guarantee of future results.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

© 2026 THE BANK OF NEW YORK MELLON CORPORATION

MARK-894004-2026-03-02

GU-810-31 December 2026