The rules of the market may have changed. How should multi-asset investors respond?

Is fiscal policy the new force driving markets?

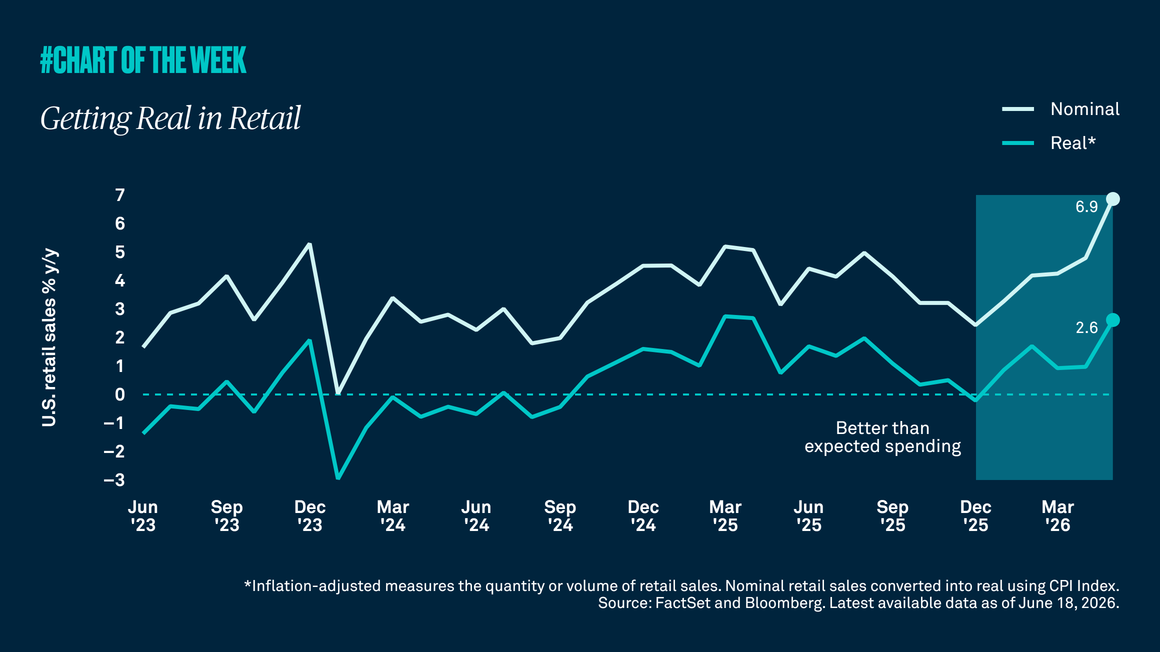

For many years, central banks guided markets, with interest-rate changes driving asset movements. That dynamic is now under pressure. We believe we have entered a regime of fiscal dominance where government spending and borrowing are playing a bigger role in influencing financial assets, and central banks are reacting rather than leading.

Rather than a short-term disruption, we see this as a structural shift. In this paper, we explore its implications.

Rethinking portfolio construction in a new regime

Inflation is proving stickier than expected, fiscal deficits are putting persistent pressure on bond markets, and geopolitical change is redrawing supply chains. The forces sustaining these pressures are structural, not cyclical – and they are unlikely to resolve quickly.

For multi-asset investors, the implications are significant. Relationships that have shaped portfolios for decades, including how asset classes behave under stress, may no longer hold.

We believe investors need to think differently: about where resilience comes from, about the opportunity set available to them, and about the risks that traditional allocations may leave unhedged.

Read the full paper to learn more about these evolving dynamics and how investors can navigate the path ahead.

IN THE UNITED STATES: FOR GENERAL PUBLIC USE. IN ALL OTHER JURISDICTIONS: FOR INSTITUTIONAL, PROFESSIONAL, QUALIFIED INVESTORS AND QUALIFIED CLIENTS.

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy.

Opinions and views expressed are subject to change without notice.

Past performance is no guarantee of future results.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation. BNY Investments is the brand name for the investment management business of BNY and its investment firm affiliates worldwide.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All information contained herein is proprietary and is protected under copyright law.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE |

©2026 THE BANK OF NEW YORK MELLON CORPORATION

MARK-953949-2026-06-17

GU-879 17 juni 2027