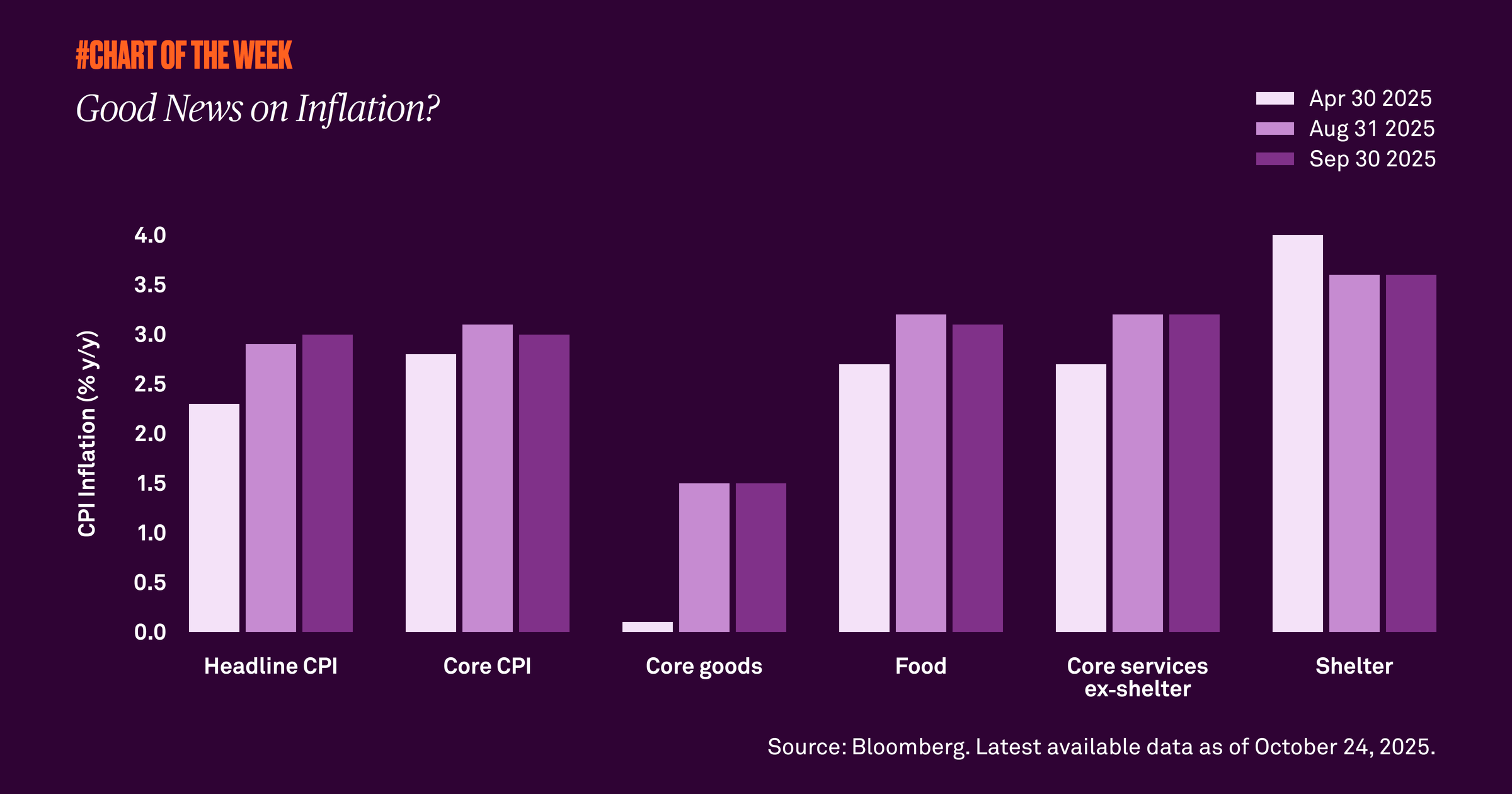

Last week’s Consumer Price Index report, a widely used indicator of inflation in the U.S. economy, showed growth of 3% in September, which was above 2.9% in August but less than expected. Despite the modest increase, various categories have shown signs of stabilization. What does this mean for inflation going forward?

Last week’s Consumer Price Index (CPI) report, a widely used indicator of inflation in the U.S. economy, showed modest growth from 2.9% on an annual basis in August to 3% in September. Yet, the number came in below analysts’ expectations, helping to allay fears of rising inflation. Consequently, the market ended the week higher.

Though the inflation reading was slightly higher than in August, a look at underlying components is encouraging. Core goods, food and core services ex-shelter have risen since April, but appear to have peaked with readings either unchanged or lower in September. Importantly, shelter, which accounts for 35% of CPI, continues to slow, helping to stabilize inflation.

There is the question of what the impact of tariffs will be on inflation once all potential deals are in effect, but we maintain that the result will be a one-time rise in prices rather than a sustained increase. Our view is that inflation will remain within a range of 2.6% to 3.3% through year end.