August 2025

INVESTMENT VIEWS

FROM THE BNY INVESTMENT INSTITUTE

The latest U.S. non-farm payroll data underwhelming, the second quarter gross domestic product (GDP) print marginally exceeding expectations, and the Federal Reserve’s (Fed) decision to leave interest rates on hold are all consistent with the BNY Investment Institute’s view of the U.S. economy continuing to slow but not stalling.

NO SURPRISES

The three events came as no real surprise. Since the start of 2025, underlying growth in the U.S. has slowed significantly which we view as consistent with tariff policy and an economy that is downshifting but not reversing. As such, our asset allocation views are unchanged. We maintain a defensive tilt across portfolios, underscoring our view that risk assets remain vulnerable amid persistent macroeconomic and geopolitical uncertainty.

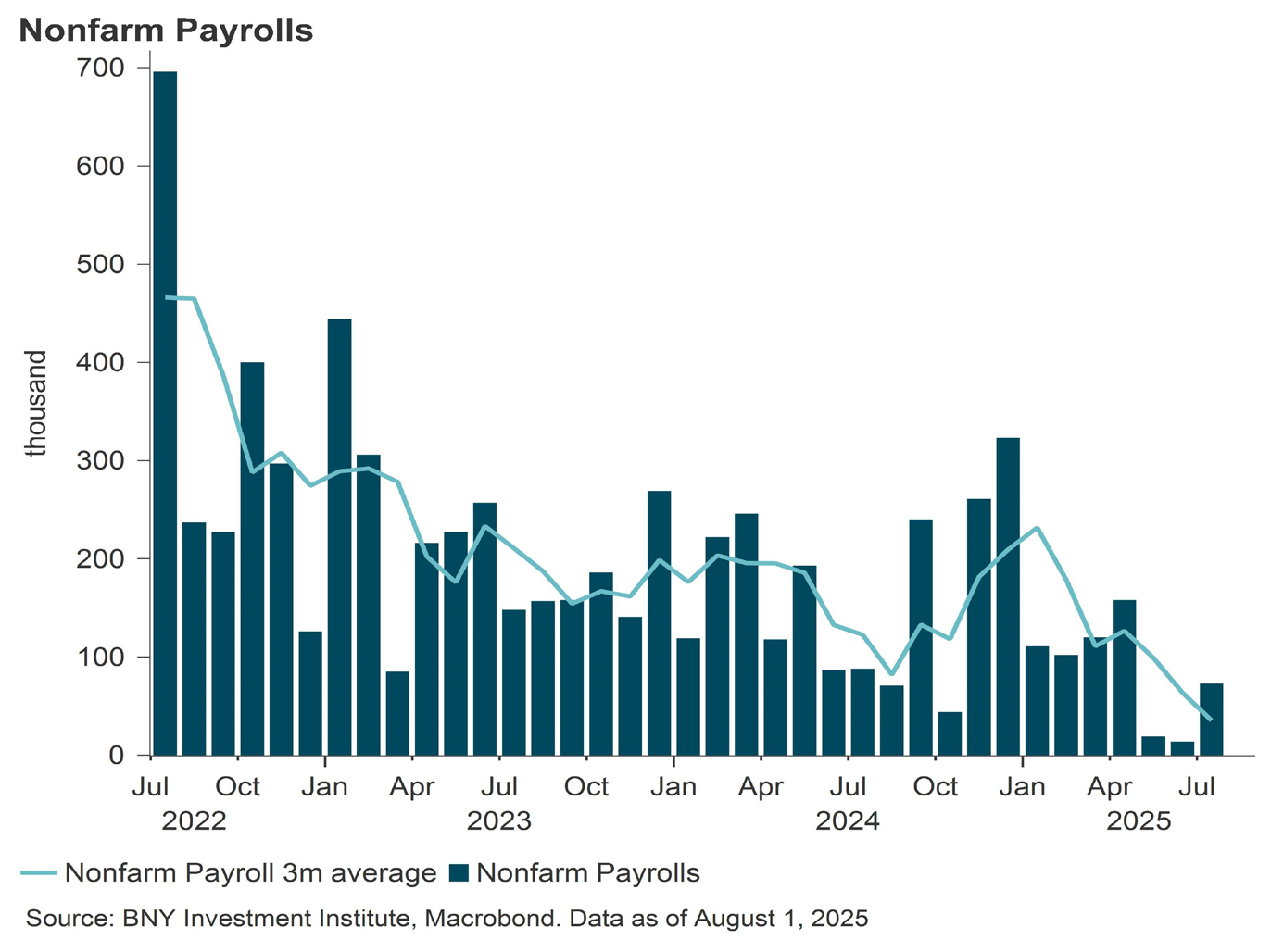

NON-FARM PAYROLLS

U.S. non-farm payrolls rose just 73,000 in July, well below expectations. May and June figures were also revised down sharply, by over 100,000 each, to just 19,000 and 14,000, respectively. These significant downward revisions over the past two months suggest that July’s estimate may also be revised lower.

The three-month average job gains fell to 35,000, signaling a clear loss of hiring momentum. While private sector employment rose 83,000, a modest improvement from June’s revised 3,000 gain, job growth remained narrow, with healthcare and social assistance accounting for 73,000 of the total gain.

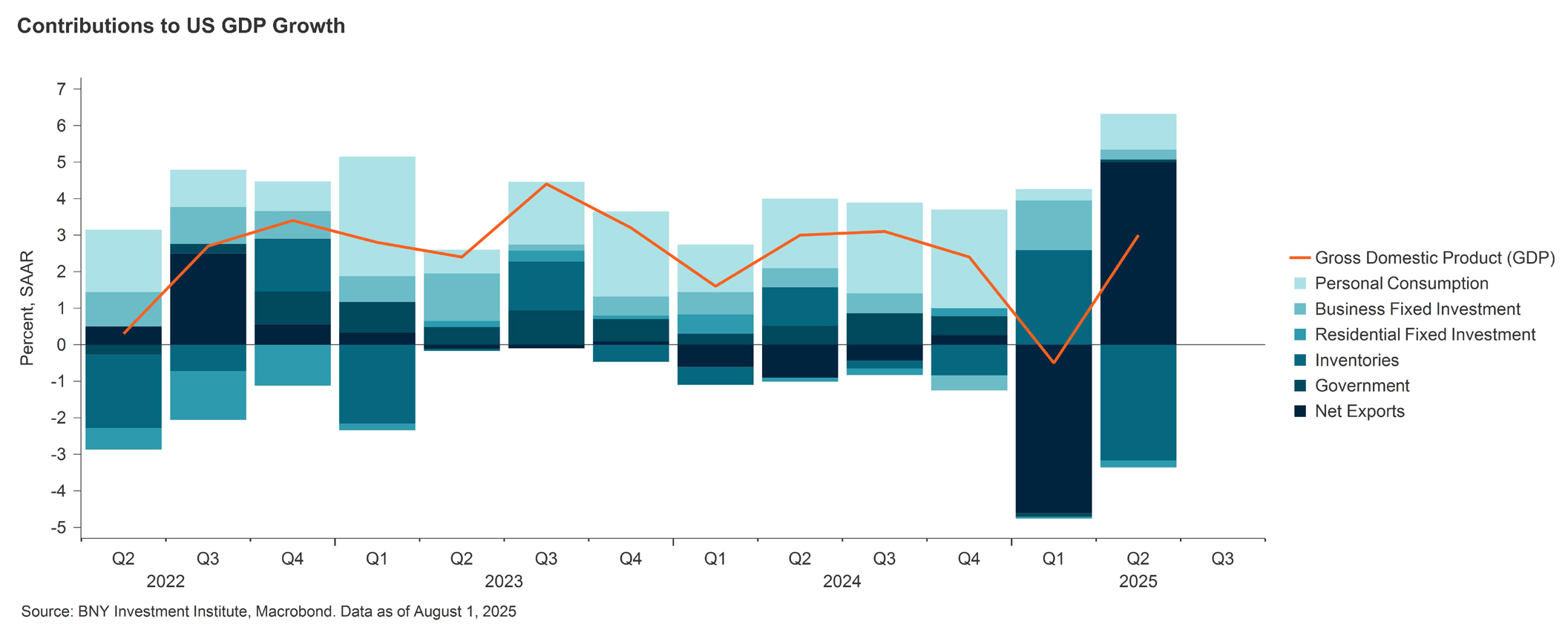

A ‘NOISY’ GDP READING

The U.S. economy grew at an annualized rate of 3% in Q2 which was above the consensus estimate of 2.6%. Looking under the hood, we believe the GDP figures for both Q1 and Q2 were affected by three policy factors that make the readings noisy:

- Fluctuations in net exports, inventories and equipment investment due to frontloading before the tariff hikes.

- Consumption distortions related to the election.

- Cuts in federal government spending (Department of Government Efficiency (DOGE)).

President Trump highlighted the 3% headline GDP growth as “way better than expected”, but we believe the underlying picture is weaker for the following reasons:

- The main driver of Q2 growth was a 5% contribution from net trade, nearly reversing the 4.6% drag in Q1 as the pre-tariff surge in goods imports unwound. Together, net exports and inventories boosted GDP growth by 1.8 percentage points (pp) in Q2, compared with a 2pp drag in Q1.

- The most reliable indicator of underlying economic momentum in the GDP data – retail final sales to private domestic purchasers, which adds consumer spending and private fixed investment – slowed significantly to an annualized rate of just 1.2% in Q2, down from 3% growth in 2024. Consumer spending rose 1.4%, up from 0.5% in Q1, but still lower than in 2024. Some of this was driven by final pre-tariff purchases, which are now reversing, indicating a weaker Q3.

- Fixed investment during the quarter was up just 0.4%. Declines in residential (-4.6%) and non-residential structures (-10.3%) were offset by solid gains in intellectual property, software, and equipment investment (4.8%) – mainly computer equipment linked to the artificial intelligence sector. However, most other equipment investments were flat or down, and surveys suggest investment will remain weak amid tariff-related uncertainty.

- Elsewhere, government spending increased only 0.4%, failing to fully offset a 0.6% decline in Q1, largely due to an annualized 11.2% drop in federal non-defense spending, likely related to DOGE cuts.

A FED CUT IN SEPTEMBER?

The Fed’s decision to leave rates on hold was universally expected and Fed chair Jay Powell offered no real policy guidance in his 45-minute press conference. The vote was split 9-2, with governors Waller and Bowman voting to ease by 25 basis points (bp).

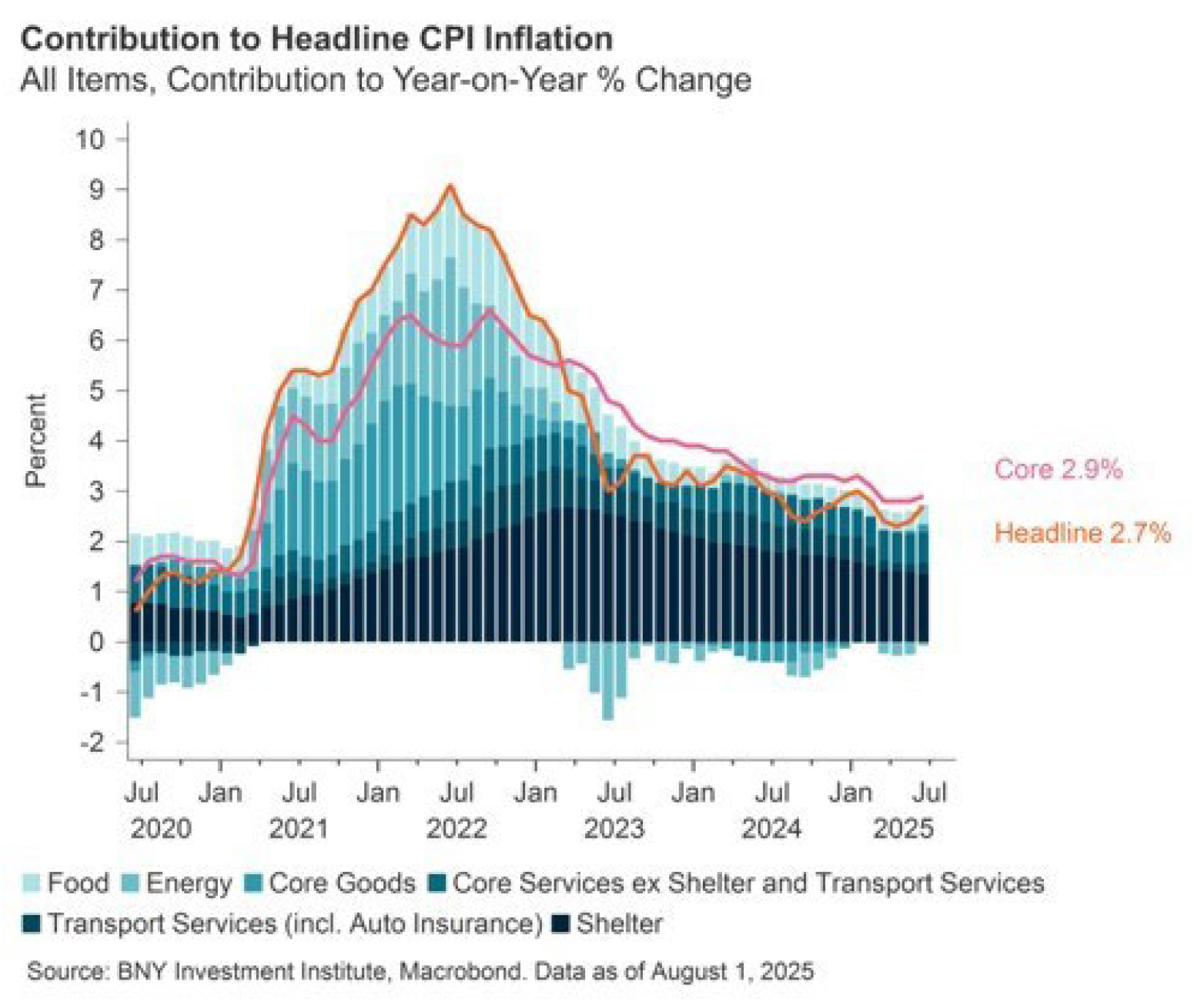

The statement from the Fed has been slightly revised since June. The main change is the committee now observes that economic activity growth has “moderated in the first half of the year”, instead of “continued to expand at a solid pace”. Labor market conditions remain “solid”, and inflation is described as “somewhat elevated”.

The statement also did not seem to provide any clear indications or signal of a September easing. However, it is worth noting that last year, the July statement also did not lay the groundwork for action in September, yet the committee ended up cutting rates by 50bp.

The Fed has the Jackson Hole conference between now and September to signal to the market if September is in play. Powell also used his press conference to say as little as possible about the future path of policy.

Looking ahead, we remain skeptical that the Fed will deliver the rate cut in September that markets are anticipating. We expect limited progress on inflation, and the impact of tariff-related price pressures should become more apparent in the data.

That said, the slowdown in the number of jobs created in the US economy, as evidenced in the recent non-farm payrolls release, is likely to have left the Fed more worried about labor market prospects. If tariff-driven inflation won’t rise as much as feared, the Fed will most likely resume rate cuts after the summer. There are two Consumer Price Index (CPI) reports scheduled before the September Federal Open Market Committee (FOMC) meeting, but only one will be available if the Fed chooses to signal its intentions at Jackson Hole.

About

BNY Investments Institute

Drawing upon the breadth and expertise of BNY Investments, the Investment Institute generates thoughtful insights on macroeconomic trends, investable markets and portfolio construction. For related content and market analysis, please visit BNY Investment Institute.

DISCLOSURE

Asset allocation and diversification cannot ensure a profit or protect against a loss. Charts are for illustrative purposes only. Past performance is no guarantee of future results.

Core inflation measures the long-term trend in prices by excluding volatile items like food and energy, providing a clearer picture of underlying inflationary pressures in the economy. Consumer price index (CPI) is an index used to measure inflation, based on the prices in a basket of goods and services, meant to be representative of those we typically spend our money on. Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. Headline inflationrefers to thetotal inflation rate within an economy, encompassing the change in prices ofall goods and services.

IN THE UNITED STATES: FOR GENERAL PUBLIC USE IN ALL OTHER JURISDICTIONS: FOR INSTITUTIONAL, PROFESSIONAL, QUALIFIED INVESTORS AND QUALIFIED CLIENTS.

This material should not be considered as investment advice or a recommendation of any investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Any statements and opinions expressed are those of the author as at the date of publication, are subject to change as economic and market conditions dictate, and do not necessarily represent the views of BNY. The information has been provided as a general market commentary only and does not constitute legal, tax, accounting, other professional counsel or investment advice, is not predictive of future performance, and should not be construed as an offer to sell or a solicitation to buy any security or make an offer where otherwise unlawful. The information has been provided without taking into account the investment objective, financial situation or needs of any particular person. BNY is not responsible for any subsequent investment advice given based on the information supplied. This is not investment research or a research recommendation for regulatory purposes as it does not constitute substantive research or analysis. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be and should not be interpreted as recommendations. Charts are provided for illustrative purposes only and are not indicative of the past or future performance of any BNY product. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance is no guarantee of future results. Information and opinions presented have been obtained or derived from sources which BNY believed to be reliable, but BNY makes no representation to its accuracy and completeness. BNY accepts no liability for loss arising from use of this material.

All investments involve risk including loss of principal.

Not for distribution to, or use by, any person or entity in any jurisdiction or country in which such distribution or use would be contrary to local law or regulation. This information may not be distributed or used for the purpose of offers or solicitations in any jurisdiction or in any circumstances in which such offers or solicitations are unlawful or not authorized, or where there would be, by virtue of such distribution, new or additional registration requirements. Persons into whose possession this information comes are required to inform themselves about and to observe any restrictions that apply to the distribution of this information in their jurisdiction.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation.

IMPORTANT INFORMATION FOR ASIA PACIFIC AUDIENCE

This document is provided to the recipient for information purposes only. This document may not be used for the purpose of an offer or solicitation, directly or indirectly, in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorised. This document has not been reviewed or approved by any regulatory authorities and is only for “Eligible Recipients”. “Eligible Recipients” means professional clients (i.e. non-retail clients) and (in jurisdictions where there are restrictions on (i) the types of professional clients which can be provided with this document; and (ii) the purposes for which this document can be provided to such professional clients) such types of professional clients (e.g. eligible financial institutions or financial intermediaries) which shall only use this document for the specific purposes as permitted under applicable laws and regulations.

This document is for the exclusive use of the Eligible Recipient. This document may not be copied, duplicated in any form by any means, published, circulated or redistributed or caused to be done so, whether directly or indirectly, to any other persons without the prior written consent of BNY. It is not intended for onward distribution or dissemination to the retail public and is not to be relied upon by retail clients. This document is not for distribution to, or to be used by, any person or entity in any jurisdiction or country in which such distribution or use would be contrary to local law or regulation, or where there would be, by virtue of such distribution or use, new or additional registration or approval requirements. Persons into whose possession this document comes are required to inform themselves about and to observe any restrictions that apply to the distribution or use of this document in their jurisdictions.

Accordingly, this document and any other documents and materials, in connection therewith may only be circulated or distributed by an entity as permitted by applicable laws and regulations. BNY Investments do not have any intention to solicit Eligible Recipients for any investment or subscription in a fund or use of BNY Investments services and any such solicitation or marketing will only be made by an entity permitted by applicable laws and regulations. BNY Investments do not intend to conduct any offering activities, investment management business, investment advisory business, and/or any other securities business in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized.

Any views and opinions contained in this document are those of Investment Manager as at the date of issue; are subject to change and should not be taken as investment advice. BNY is not responsible for any subsequent investment advice given based on the information supplied.

BNY, BNY Mellon and Bank of New York Mellon are the corporate brands of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally. BNY Investments encompass BNY Mellon’s affiliated investment management firms and global distribution companies. Any BNY entities mentioned are ultimately owned by The Bank of New York Mellon Corporation.

This document is not intended as investment advice. Investment involves risk. Past performance is not indicative of future performance. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. The value of investments and the income from them is not guaranteed and can fall as well as rise due to stock market and currency movements. When you sell your investment you may get back less than you originally invested.

No warranty is given as to the accuracy or completeness of this information and no liability is accepted for errors or omissions in such information. BNY accepts no liability for loss arising from use of this material.

The investment program contained in this presentation may not meet the objectives or suitability requirements of any specific investor. An investor should assess his/her own investment needs based on his/her own financial circumstances and investment objectives. You are advised to exercise caution when reading this document. If you are in any doubt about the contents of this document, you should obtain independent professional advice.

The information contained in this document should not be construed as a recommendation to buy or sell any security. It should not be assumed that a security has been or will be profitable. There is no assurance that a security will remain in the portfolio. Tax treatment will depend on the individual circumstances of clients and may be subject to change in the future.

If there is any inconsistency between this warning statement and the disclosure stated under this document, this warning statement shall prevail to the extent of the inconsistency.

BNY COMPANY INFORMATION

BNY Investments is the brand name for the investment management business of BNY and its investment firm affiliates worldwide. BNY is the corporate brand of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally. • Mellon Investments Corporation (MIC) is a registered investment advisor and subsidiary of The Bank of New York Mellon Corporation. MIC is composed of two divisions: Mellon, which specializes in index management, and Dreyfus, which specializes in cash management and short duration strategies. • Insight Investment - Investment advisory services in North America are provided through two different investment advisers registered with the Securities and Exchange Commission (SEC) using the brand Insight Investment: Insight North America LLC (INA) and Insight Investment International Limited (IIIL). The North American investment advisers are associated with other global investment managers that also (individually and collectively) use the corporate brand Insight. Insight is a subsidiary of The Bank of New York Mellon Corporation. • Newton Investment Management - “Newton” and/or “Newton Investment Management” is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021, NIMJ was established in March 2023. NIM and NIMNA are registered with the Securities and Exchange Commission (SEC) in the United States of America as an investment adviser under the Investment Advisers Act of 1940. Newton is a subsidiary of The Bank of New York Mellon Corporation.• ARX is the brand used to describe the Brazilian investment capabilities of BNY Mellon ARX Investimentos Ltda. ARX is a subsidiary of The Bank of New York Mellon Corporation. • Walter Scott & Partners Limited (Walter Scott) is an investment management firm authorized and regulated by the Financial Conduct Authority, and a subsidiary of The Bank of New York Mellon Corporation. • Siguler Guff - The Bank of New York Mellon owns a 20% interest in Siguler Guff & Company, LP and certain related entities (including Siguler Guff Advisers LLC). • BNY Mellon Advisors, Inc. (BNY Advisors) is an investment adviser registered as such with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Investment Advisers Act of 1940, as amended. BNY Advisors is a subsidiary of The Bank of New York Mellon Corporation.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All information contained herein is proprietary and is protected under copyright law.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE |

©2025 THE BANK OF NEW YORK MELLON CORPORATION

MARK-782966-2025-08-01

GU-679 1 March 2026