Bond markets: duration could be your friend

In each of the three market crises we’ve addressed, bond yields fell as investors sought the safety of fixed income. For example, during the GFC, the 10-year U.S. Treasury yield, which stood above 5% in mid-2007, fell to below 2.5% by the end of 2008. Yields remained below 4% for most of the next decade, as the Federal Reserve maintained ultra-accommodative policies to support the economy.6

During the Covid-19 pandemic, bond markets reacted sharply — the 10-year Treasury yield plunged to an all-time low of just ~0.5% in March of 2020 and remained below 2% until economies around the world reopened in 2022.7

Longer-duration bonds (Treasuries with 10-to-30-year maturities) saw significant capital appreciation during these periods due to bond prices surging. In some cases, these gains helped stabilize portfolios and provided total return, even though rates were low.

It’s notable that during these times that spreads on sub-investment grade bonds widened significantly, suggesting caution around over-exposure to high yield credit during volatile times.

Lessons for investors

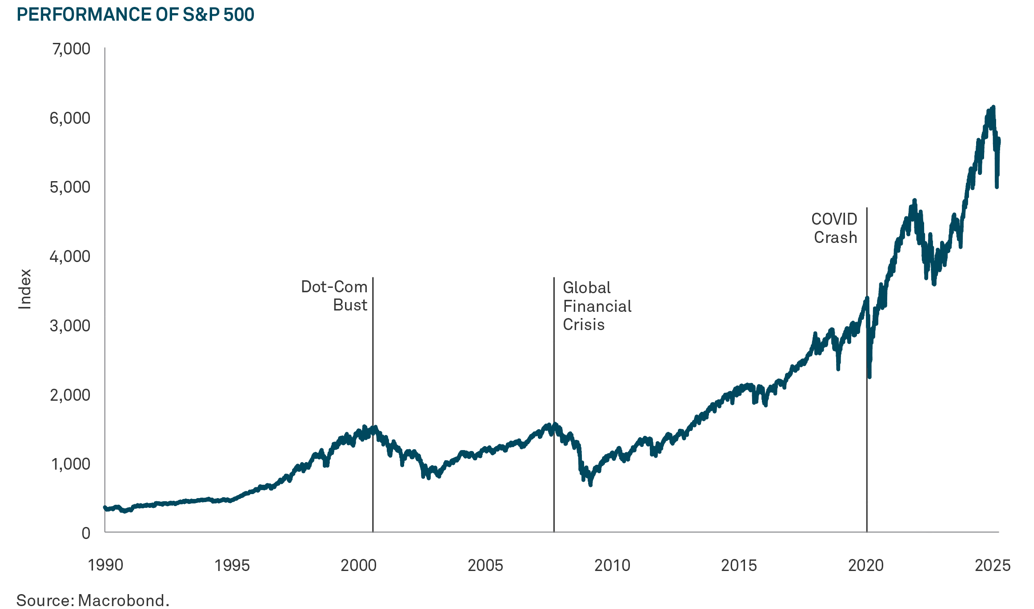

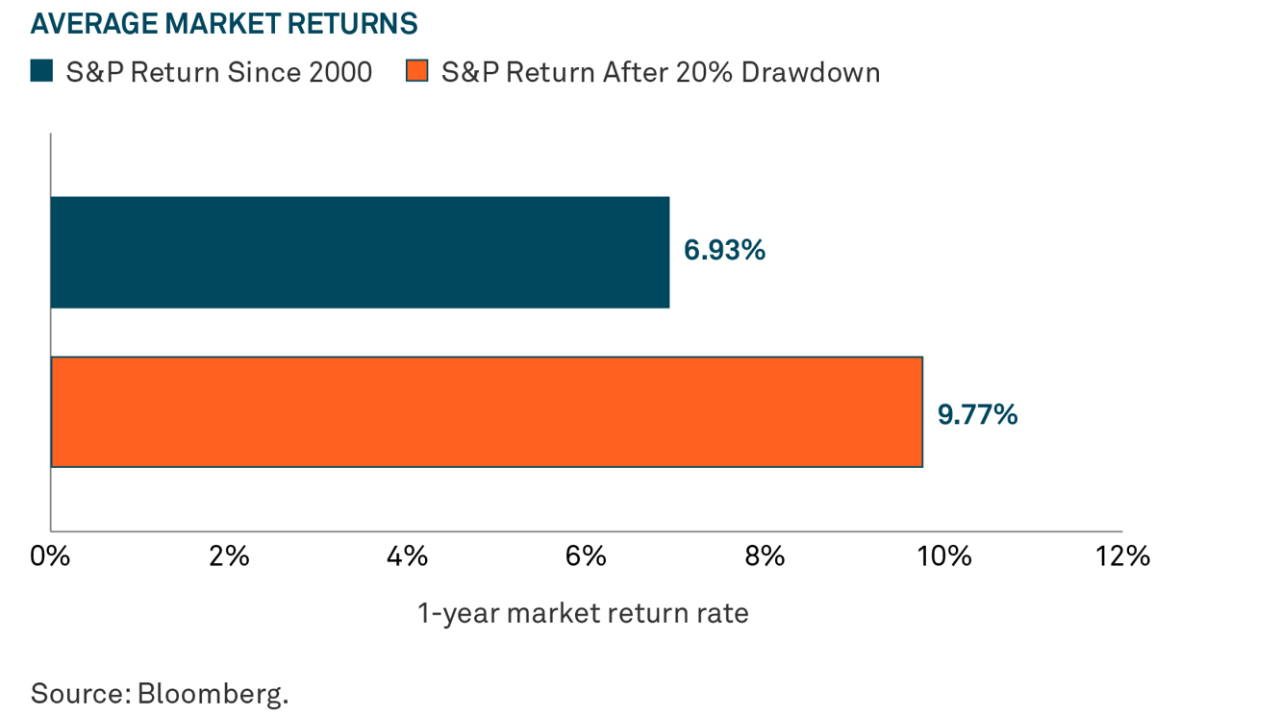

Market history shows that though periods of volatility are painful, equity drawdowns have consistently been followed by recovery. And while bond yields have historically taken longer to recover, there are opportunities in fixed income during volatile times as well.

Overall, amid market volatility, it’s valuable to keep in mind that:

1. Market declines are a feature, not a bug, of long-term investing.

2. The depth of a downturn does not preclude a strong rebound.

3. Trying to time the market amid uncertainty is exceedingly difficult — and often counterproductive.

4. Staying invested, diversified, and focused on long-term goals remains a reliable strategy.