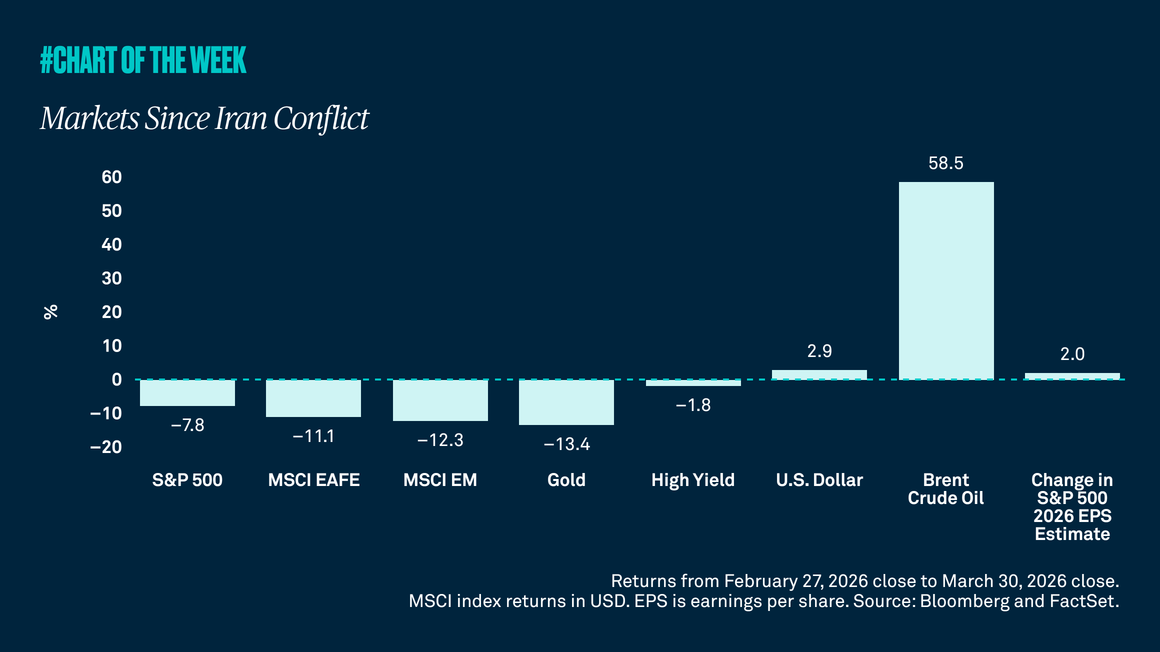

We sat down with Jason Granet, Chief Investment Officer at BNY, Vincent Reinhart, Chief Economist and Macro Strategist at BNY Investments Dreyfus and Mellon, and John Velis, FX and Macro Strategist for the Americas at BNY Markets, to discuss the direction of the U.S. economy, global central bank policy and the outlook for asset prices.

Where is the U.S. economy heading?

JASON: We came into the year with a strong economy; the labor market was in good shape, corporate earnings were resilient and balance sheets were healthy. Through the year, however, the economy had to absorb a series of challenges in the form of tariff shocks, persistent inflation, a weakening dollar and, most recently, the government shutdown. The economy’s ability to withstand these challenges thus far is due to the strong footing from the start of the year. But looking ahead, it feels like the probability of hitting potholes is higher, given the speed of policy shifts and changing market dynamics.

JOHN: We see growth continuing but slowing down. There are two dynamics propping up the economy. First, AI-related investing has increased significantly over the last couple of quarters and is likely to continue. Second, consumption remains strong. But it’s worth noting that consumption is highly concentrated in the top income sectors, and more of it is funded via credit, which is typical late-cycle consumption behavior. So, while we may not be in for a recession, I think we’re heading toward an economy with weakening growth in a quarter or two.

What is the Fed going to do?

VINCENT: My forecast for 2026 and 2027 isn’t as much about the macro economy as the political economy. Personnel is policy, and personnel at the Fed is changing. There will be more monetary policy easing in 2026 and into 2027 because there will be more governors aligned to the policy approach of the White House. Some of the financial accommodation now is in anticipation of significant Fed easing in 2026 and beyond.

JOHN: The government shutdown means there has been limited economic data. Lack of data could mean those Fed members concerned about the labor market and willing to look past the sticky inflation data will have a stronger hand. Therefore, the Fed may err on the side of supporting economic activity.

What are other central banks likely to do?

JOHN: We don’t think the easing story is necessarily finished in most European economies, nor for the Bank of Japan (BOJ). While we still expect a rate hike in December from the BOJ, the country’s new prime minister is dovish, so a lot could yet unfold in terms of monetary policy.

VINCENT: I think the Fed is going to be easing more, potentially leaving it on a contrary path to some other central banks. The European Central Bank (ECB) perhaps has the advantage over the Fed of not reporting to any one government about the conduct of its policy. Without coordinated political pressure, the ECB has more leeway to pursue its single goal of price stability, which is why its policy rate won’t go down as far as the Fed’s. In the U.S., the Fed is under pressure because the White House and a lot of Congress are on one side.

What worries you?

VINCENT: A lot of Fed policy accommodation has made the wealthy wealthier, so the upper echelons are driving spending. If financial accommodation remains, this segment could continue to drive spending.

The core issue is whether labor demand is slowing to “stall speed,” making the economy vulnerable to adverse shocks. Picture an airplane flying slower and closer to the ground — a pilot would say this makes the plane vulnerable to non-linear events, like an abrupt shift in winds. An economist would say a non-linear economic event is a shock that tips you into a recession.

We should worry about stall speed, given how slow job gains have to be to keep the labor market in balance given the slowing in labor supply — something on the order of 50,000 jobs created on net per month. It doesn’t take much for that number to turn negative, which would result in those worrying non-linearities: jobs declining, people without income, businesses closing — those all lead to irreparable damage. We’re close to stall speed and that’s a shock risk.

JOHN: As far as we can tell, there’s not a lot of hiring going on, but there’s not a lot of firing either. That is often a first step in starting to see layoffs. When you start producing fewer than 100,000, 75,000 or 50,000 private-sector jobs for several months in a row, then you’re at stall speed. As Vincent pointed out, stall speed can quickly become “hard-landing speed” if the policy response and/or the market response isn’t sufficient or timely enough.

What is your outlook on asset prices in the current environment?

JASON: The economic headwinds that we’ve discussed — tariff uncertainty, sticky inflation, the weakening U.S. dollar and the government shutdown — are all likely to be reflected in the market through steeper yield curves. Also, at some point, inflation will have to be addressed, and markets will have to reconcile the costs of higher prices. If we get an easier central bank up front, and we run the economy hotter, the yield curve is likely to steepen over time as markets begin to question the system’s longer-term credibility.

The dollar’s weakness makes the U.S. more investable relative to places with their own frustrations. From an asset allocation standpoint, it could pay to be ready by considering downside protection or long rates — but carry will remain attractive, and the dollar-weakness trend feels like a feature, not a bug, for U.S. aggregate demand.

JOHN: The U.S. dollar has picked up from its lows in mid-September. And with the Fed easing and some other central banks potentially following suit, interest rate differentials are unlikely to remain extremely wide in the short term. In a low-volatility environment, that dynamic encourages investors to pursue carry and yield-enhancing strategies, which can amplify risk taking and fuel market exuberance.

Jason Granet

Chief Investment Officer

BNY

Vincent Reinhart

Chief Economist

BNY Investments Dreyfus & Mellon

John Velis

Americas Macro Strategist

BNY Markets

This is an excerpt from our report Recalculating Route: At the Table with BNY

Important Information

For sole and exclusive use by Institutional Investors, Accredited Investors and Professional Investors only. Not for further distribution. This is a financial promotion and is not investment advice. Any views and opinions are those of the investment manager, unless otherwise noted. The value of investment can fall. Investors may not get back the amount invested. BNY, BNY Mellon and Bank of New York Mellon are the corporate brands of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally. BNY Investments encompass BNY Mellon’s affiliated investment management firms and global distribution companies. Any BNY entities mentioned are ultimately owned by The Bank of New York Mellon Corporation. In Hong Kong, the issuer of this document is BNY Mellon Investment Management Hong Kong Limited, which is registered with the Securities and Futures Commission (Central Entity Number: AQI762). In Singapore, this document is issued by BNY Mellon Investment Management Singapore Pte. Limited, Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore (MAS). This advertisement has not been reviewed by the Monetary Authority of Singapore.

GU-746 Exp: 31 October 2026