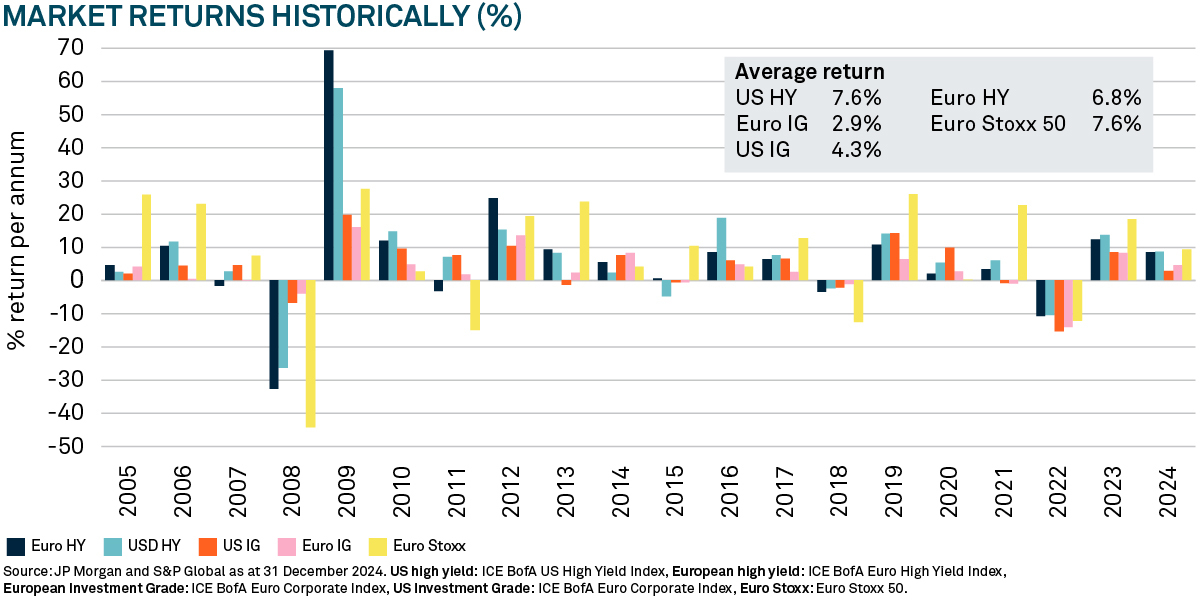

LaRusse observes over long periods high yield has performed well against equities and with lower volatility, based on a comparison of the Euro Stoxx 50 with the US high yield market (see chart below).

Is high yield beta attractive? Should it be a core rather than tactical part of investment portfolios? Insight Investment1 head of fixed income specialists April LaRusse explains how a systematic approach can offer the potential for enhanced beta exposure to the asset class.

Additionally, LaRusse says when it comes to asset allocation, with equity market valuations looking expensive and dividends being at the whim of a company’s performance, the certainty of a bond’s coupon could be appealing to investors in this environment.

“The potential for further volatility in the equity market is absolutely there and I think it is one of the reasons why clients want to talk about the equity/bond balance in their portfolios,” she adds.

What’s more, LaRusse argues that high yield has fundamentals on its side. For example, defaults in the asset class are low. Higher inflation and interest rates made borrowing expensive in recent years, meaning companies have sensible levels of leverage and interest coverage, she says. Then there is the fact that bond yields generally have moved higher in this higher interest rate environment, meaning they actually pay an income.

Beta with a bit extra

Given these tailwinds, LaRusse says some clients have been seeking exposure to high yield beta. But she observes some are seeking an added return to compensate for fees. Historically high yield has been an illiquid market and expensive to trade but LaRusse suggests a quantitative, systematic approach can be a cost-effective way of accessing illiquid areas of fixed income, for example fallen angels2.

Insight uses a so-called ‘portfolio trading’ to reduce trading costs. Rather than trade bond by bond, this approach uses the exchange traded fund (ETF) ecosystem to trade a basket of bonds. This basket contains stocks screened using a quant model for quality and cost – in that order – and that by nature tend to have a structurally higher spread.

The screen essentially identifies two factors – quality and cost:

1. It aims to eliminate poor quality companies with deteriorating credit trends in terms of leverage, interest coverage, profit margins and liquidity – and it looks at how the equity is performing.

2. It screens for cost. It is important this step comes after the quality screen to avoid value traps: companies that are cheap for good reason because they are poor quality.

“The reason that order matters is because if you tell any computer system to optimise for the most attractive bonds, it is going to pick the ones with the biggest spread or yield. But there might be a reason that you have a high spread or yield. So, first you need to get rid of the bonds that are poor quality, then you can optimise for value,” explains LaRusse.

But she says it is important to tilt the portfolio to avoid it being skewed towards certain sectors and credit quality which deviates too far away from the high yield market, or beta.

As a result, the portfolio tends to be overweight recently downgraded companies (fallen angels). But LaRusse notes rigorous analysis avoids “falling knives” – businesses that have been downgraded but are likely to be downgraded again and again.

“Ultimately what we're trying to build using this quantitative model is a portfolio that is less risky than the universe but capturing all the value and making sure that it has the same beta of the overall high yield market,” she explains.

Three reasons why fallen angels appear attractive:

1. Large global businesses that ultimately end up back in the investment grade universe, so they are quality companies.

2. Potential for solid returns, given they tend to have longer duration which has proved positive in a falling interest rate environment.

3. Favourable risk/reward characteristics. Technical dislocations can create valuation opportunities, particularly when fixed income indices are required to offload investment grade holdings when they are downgraded to high yield.

“It is not about taking views on interest rates or about shifting sector allocations,” adds LaRusse. “This is about trying to give access to high yield in the cheapest way possible, essentially by using these quant techniques.”

The value of investments can fall. Investors may not get back the amount invested. Income from investments may vary and is not guaranteed.

1 Investment Managers are appointed by BNY Mellon Investment Management EMEA Limited (BNYMIM EMEA), BNY Mellon Fund Management (Luxembourg) S.A. (BNY MFML) or affiliated fund operating companies to undertake portfolio management activities in relation to contracts for products and services entered into by clients with BNYMIM EMEA, BNY MFML or the BNY Mellon funds.

2 Fallen angels: investment grade bonds that have dropped down the credit rating into the high yield space.

2409509 Gültig bis: 17 Oktober 2025