LatAm Equities, Commodities and Politics

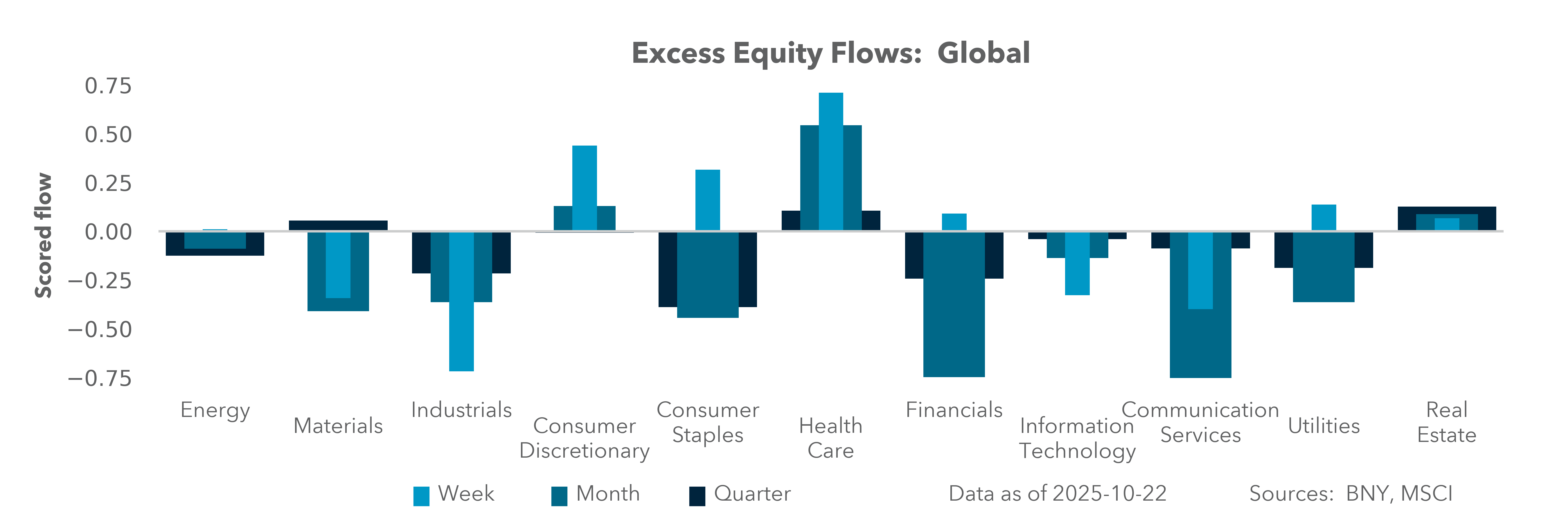

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

LatAm markets were hit by the unwinding of carry trades in FX and fixed income last week. One factor behind the repricing in the region is the shifting role of U.S. and Chinese trade and investments in the region. The upcoming APEC summit could mark a return of LatAm as a strategic growth region given its demographics, ability to straddle U.S. and Chinese demand and improving fiscal and growth outlook. Investors are looking for confirmation of this scenario from voters, but the role of Gen Z in the region cannot be ignored with Peru and Uruguay reflecting the global youth movement seen in countries as disparate as Nepal, Morocco and Kenya.

There is a new political risk in emerging markets, as traditional parties face increased scrutiny focused on issues like the environment, corruption and inequality. The impact of elections in Argentina will be felt well beyond Buenos Aires as investors look at ARS and the U.S. role in supporting the Argentine currency against others in the region. Elections will also be held in Chile (November 16), Peru (April 2026), Colombia (May 2026) and Brazil (October 2026). Investors are currently focused on the unwinding of the carry trade as it limits bond and FX buying in the region, along with the fiscal dominance risks arising from the shifting political landscape. Equities are the main under-appreciated offset with raw materials viewed as the anchor for value across a region fraught with fears of inflation.

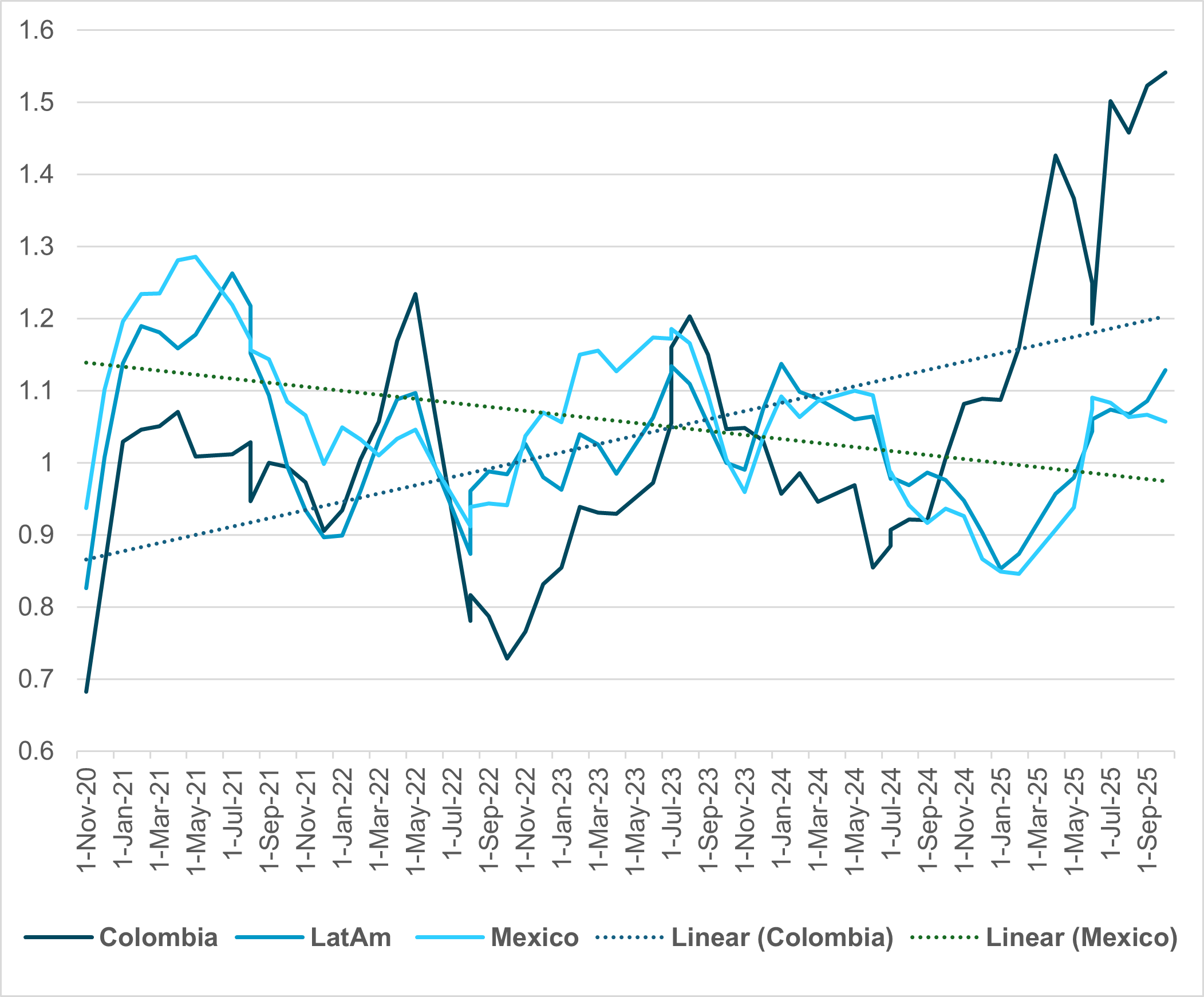

EXHIBIT #1: LATAM, COLOMBIA, PERU AND MEXICO EQUITY HOLDINGS

Source: BNY

Our take

Investor appetite has diverged sharply between Colombia and Mexico. Since July 2024, holdings of Colombian equities climbed steadily – interrupted only by the “Liberation Day” sell-off over new tariffs in April 2025. That rally reflected two forces working in tandem: Colombia’s commodity exposure and its deep U.S. trade ties. But last week, President Gustavo Petro’s diplomatic clash with Washington threatened to unravel decades of cooperation just as a modest post-election recovery was losing steam. Construction and services growth has slowed, while rising fiscal pressures, policy uncertainty and political noise now weigh heavily on the fragile rebound. As a result, Colombian equity allocations sit well above their long-term average, in stark contrast to Mexico’s, which remain near their five-year norm.

Forward look

Peru and Mexico’s relationships with the U.S. hinge on two landmark trade agreements: Peru’s 2009 Free Trade Agreement and Mexico’s 2018 USMCA. Mexico remains the most deeply integrated – its auto plants, energy projects and agricultural exports flow seamlessly into the U.S. – while Peru’s link is more commodity-centric, with the country shipping copper, gold and fruit to north. Colombia, too, maintains a solid U.S. foothold with exports of oil products, aluminum and coffee. That commodity focus shows up in equity flows: Peru and Colombia are trading at 10–20% premiums to their five- and ten-year averages, whereas Mexico and Brazil sit close to their long-term norms. But with raw materials in the global spotlight, inflationary pressures rising and political risks increasing, Mexico and Brazil’s regional capital dominance could be headed for a turning point.

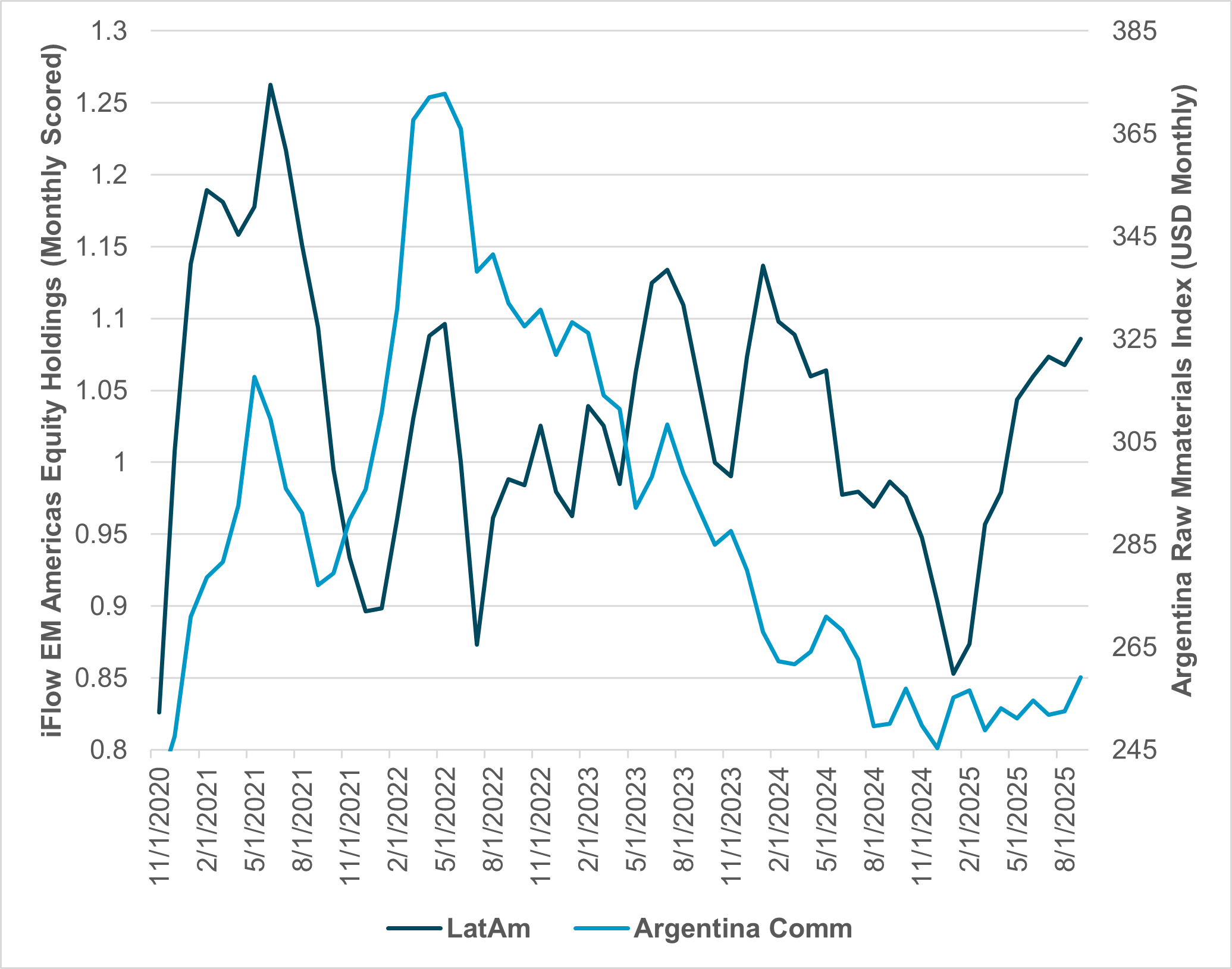

EXHIBIT #2: LATAM EQUITY HOLDINGS VS. REGIONAL COMMODITY INDEX

Source: BNY, Bloomberg

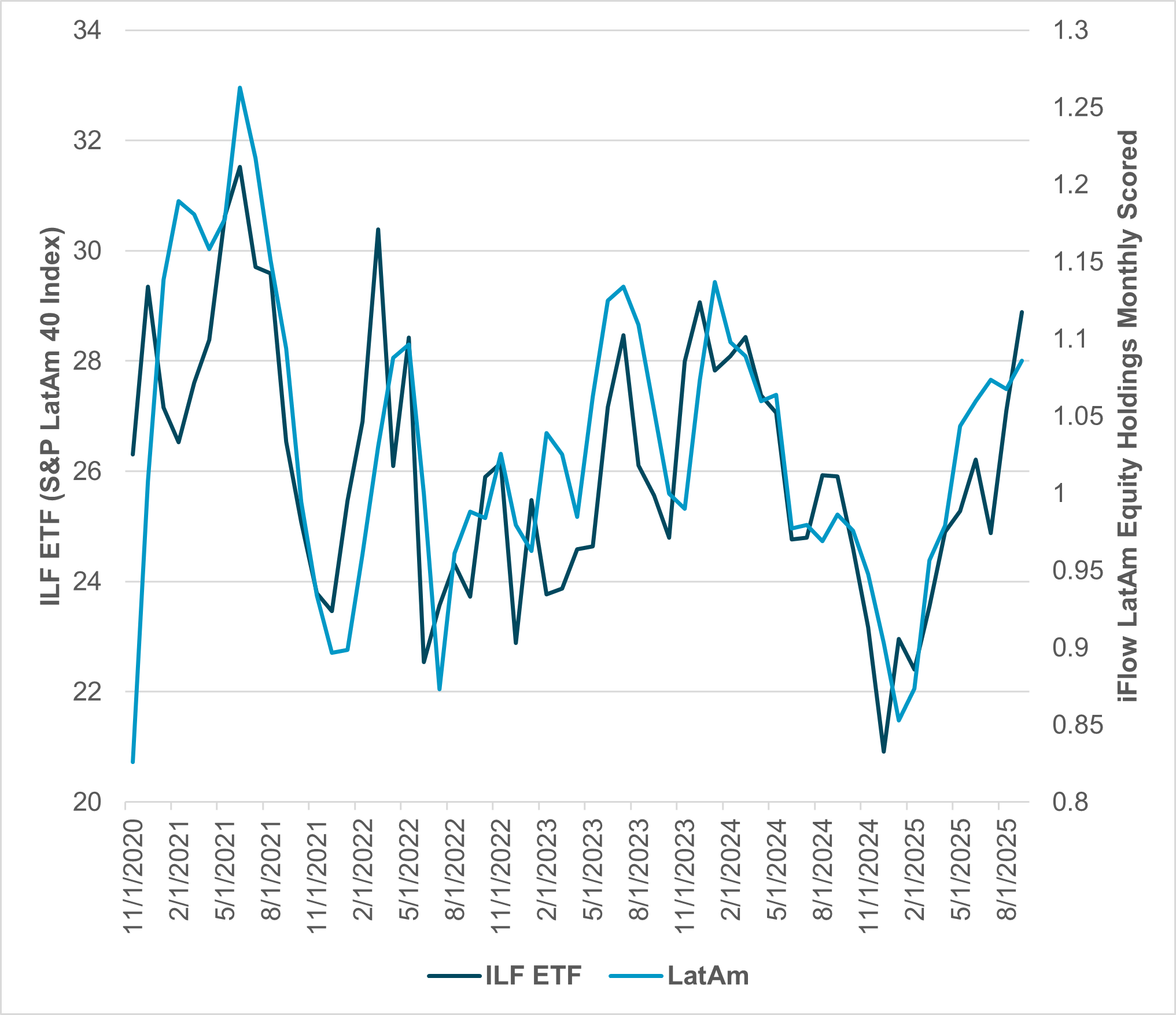

EXHIBIT #3: IFLOW LATAM HOLDINGS AGAINST THE ILF ETF

Source: BNY, Bloomberg

Our take

While commodities were a significant driver of LatAm equity holdings in past cycles, this has not been the case in the current run. The start of the Russia–Ukraine war in 2022 helped spark investments into the region. There is currently a currency-linked runup in LatAm holdings, more as a result of USD weakness in the first half of 2025 than the commodity mix underlying the equity base. Copper and gold are key commodities for Peru and Chile, while Brazil and Argentina exports soybeans and beef, Colombia is an energy story, and Mexico is focused on labor, manufacturing and oil. The key point for LatAm equities has been the carry trade, USD weakness and relative political stability. The problem for tracking commodities to equities to the region is the commodity basket. Brazil and Argentina both have regional indices, but they do not reflect the bigger shift in demand from manufacturing to software..

Forward look

The relationship of our client holdings to the LatAm S&P 40 benchmark is notable and worth considering as well. The index’s $1tn market capitalization is not the region’s entire story, and investors resides can find alpha by picking the right mix for domestic growth and commodity-linked export demand. The index is most heavily weighted in Mexico and Brazil shares. There may be opportunity if Chile, Peru and Colombia outperform depending on the future political situation. Investors are watching this weekend’s elections for clues about the mood of regional voters. The outcome of trade deals and geopolitical events will also be crucial.

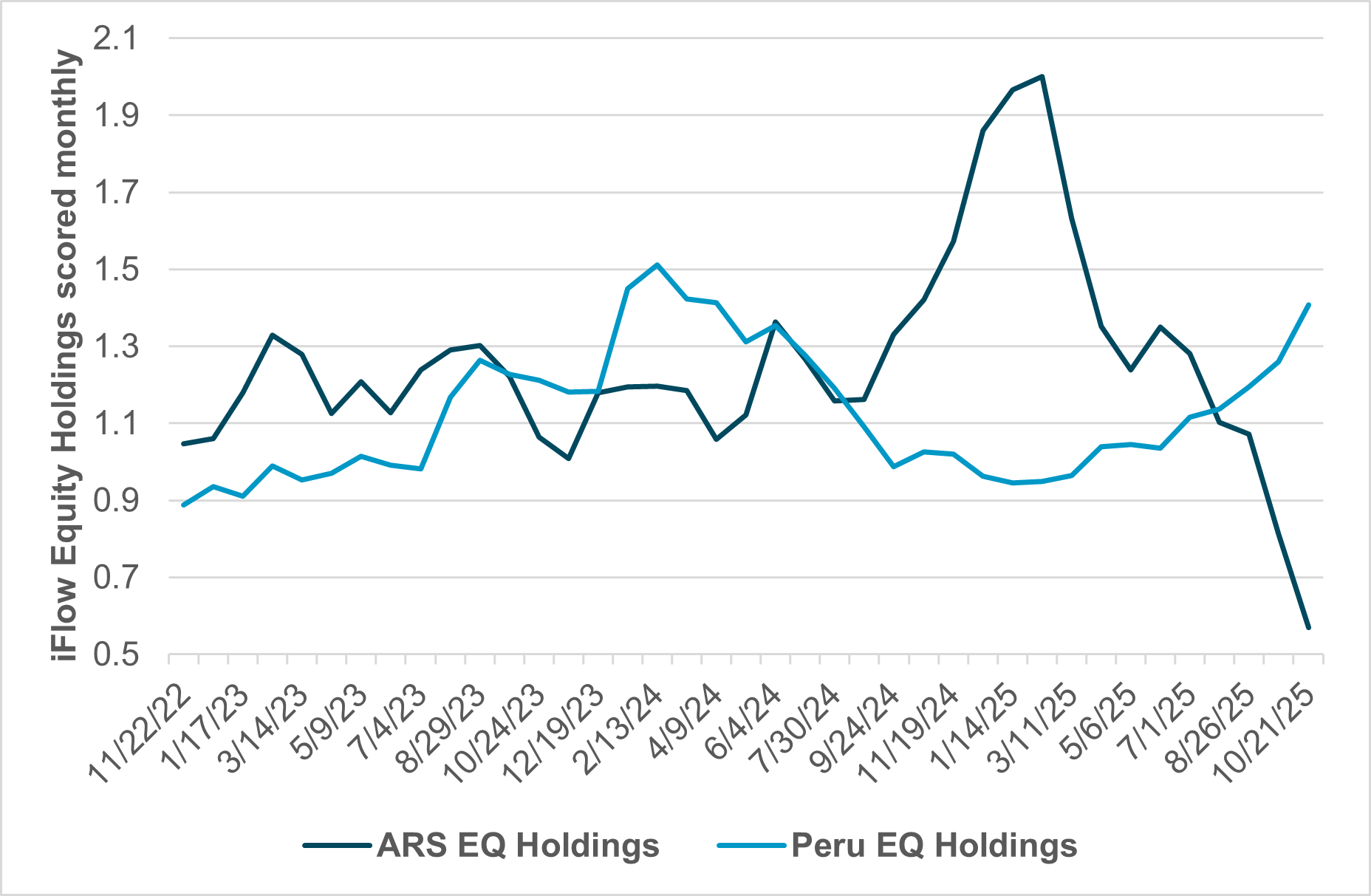

EXHIBIT #4: ARGENTINA AND PERU EQUITY HOLDINGS

Source: BNY, Bloomberg

Our take

Both Peru and Argentina have a political risk premium. The difference is the upcoming mid-term elections in Argentina are seen as a referendum on President Milei’s fiscal reforms, while in Peru the Gen Z movement at the heart the recent Lima anti-corruption protests and frustration with security are the dominant issues. What is clear from our iFlow data is that investors have been returning to Peru regardless of politics while Argentina’s political problems have led to a significant washout. The sector concentration of Argentina shares vs. Peru is also a driver as the rush to invest in industrial metals and gold has been a driver, while oil and agricultural goods have been weaker in 2025. Frustrations with the underlying economy and the need for change show up in the two nations and make the upcoming elections that much more important for both.

Forward look

The risk for LatAm lies in the extreme moves across the region in equities, with Argentina and Mexico clearly underheld against Peru, Colombia and Brazil. The largest regional market capitalization is in Brazil, with its concentration of oil and mining holdings extending across the entire region. Fiscal pressures throughout the region make taxing foreign investment an ongoing political issue. Overweight equity holdings in Brazil display some of this via the utility sector, which has similar payouts to bonds but under a different tax regime. The relationship between FX and the value factors driving flows into the region will continue to be a key part of underlying equity volatility beyond macro expectations that commodities will outperform in 2026.

Latin American markets are navigating a pivotal juncture as the global carry trade unwinds, exposing vulnerabilities in FX and fixed income while highlighting equity opportunities tied to commodities and policy clarity. The coming mid-term elections in Argentina, the general election in Chile and the presidential election in Colombia will shape fiscal trajectories and investor confidence, especially as geopolitical dynamics between the U.S. and China are redefining trade flows. Despite volatility, the region’s structural advantages – demographics, natural resources and integration with both major economies – suggest resilience. Equity allocations in Colombia and Peru remain elevated, signaling optimism around commodities, while Mexico’s positioning near historical averages underscores its manufacturing and U.S.-linked growth base. Looking forward, the region’s equity appeal will hinge on stable governance, credible fiscal policies and sustained demand for raw materials. For investors, selective exposure to economies balancing reform momentum with external trade opportunities offers the most compelling route to alpha amid a re-pricing cycle that rewards patience and diversification.