Market Movers: Wavering

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 14 minutes

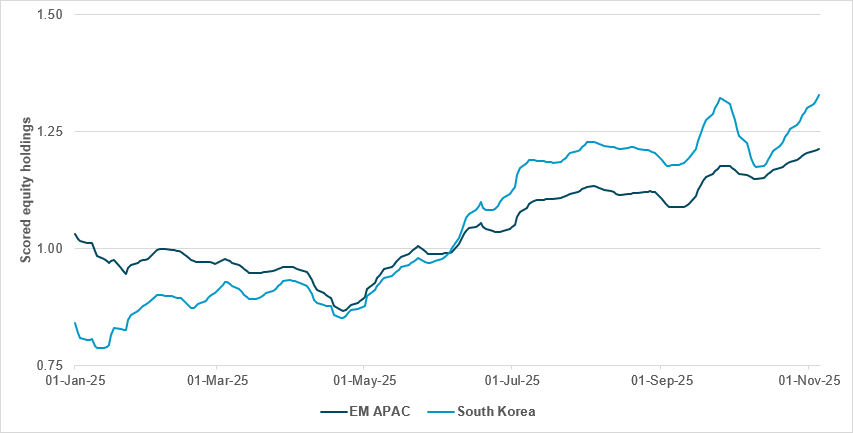

Unwinding of elevated EM APAC equity holdings likely to have knock-on impact on FX

Source: BNY

Equity markets continue to trade in a choppy and uneven fashion, and it has become increasingly evident that the stretched valuations narrative is exerting a deeper and broader influence on global sentiment. While the challenges facing U.S. technology stocks are widely known and have been extensively discussed, similar concerns are now emerging over the sustainability of APAC equity valuations. This is particularly the case for economies tied to the AI narrative, either organically, such as China and Japan, or through their strong supply chain dependence on U.S. demand, notably Taiwan and South Korea. Recent trends in holdings reveal a clear divergence between EM and DM APAC markets over the past few weeks. DM APAC holdings have fallen to roughly 5% above their rolling one-year average, with Japan’s outlook attracting particular concern, while EM APAC holdings have continued to rise, beginning November at their highest levels of the year. This resilience amid ongoing U.S. market volatility is noteworthy, and continued earnings delivery could reinforce the DM-to-EM rotation narrative that appears to be gaining traction heading into 2026. Nevertheless, if EM markets ultimately fail to outperform DM peers within a weaker global cycle, capital outflows could become more entrenched as price action softens. This could have meaningful consequences for associated currency exposures. South Korean equities remain the most overheld in APAC, and although cross-border inflows have risen sharply alongside valuations supportive of KRW appreciation, recent flow dynamics indicate these purchases may reflect hedge unwinding rather than renewed optimism. That underscores the fragile equilibrium between positioning and sentiment across the region.

Risk-off sentiment pervades, as emerging market equities lead the week with their worst performance since August. Behind the wavering of “buying the dip” lie three stories. The first is the drop in Chinese trade, with exports down and imports weak, highlighting the impact of tariffs. Second, the NY Fed President John Williams has admitted that we are close to “ample” reserves and said he sees the Standing Repo Facility playing a critical role. Third, Japanese Prime Minister Sanae Takaichi has been filling government panels with acolytes of Abenomics, known for their loose fiscal policy bias, while polls suggest Japan is in a technical recession.

The global mood for growth has fallen into Q4 “soft patch” thinking, which leaves policy responses from governments key, even as central bankers near the end of easing cycles. In the U.S. session ahead, hopes for a path to reopening the government dominate, as airline disruptions join the list of other troubles from the shutdown. Today would normally bring the U.S. employment report, but instead we have the leftover anxiety from the Challenger layoff report. Investors are also paying close attention to rates and liquidity, with credit markets back in the spotlight. This comes after OpenAI CFO Sarah Friar floated the idea that the U.S. government should provide a “backstop guarantee that allows the financing to happen.” Trump’s AI czar David Sacks yesterday warned “There will be no federal bailout for AI.” Neither question nor answer provides much comfort, with wavering risk-taking across markets. Today’s U.S. flash consumer sentiment may highlight the limits of buying the dip in the face of the pain of sticky inflation and government shutdowns.

We are ending the week much as we started it when it comes to confidence, but with equity prices lower, along with higher bond yields and a flat FX market. Momentum is the key guide for the day; the focus will be on the 8% drop in Bitcoin, which has sent crypto markets into a bear market, erasing almost all 2025’s gains. The implications for retail confidence look different now, and the race to 2026 more difficult.

U.S. airlines will start cutting flights today, as the nation’s longest government shutdown begins to disrupt air travel across 40 major airports. The Federal Aviation Administration has ordered carriers to reduce domestic flight capacity by 4% from Friday, escalating to 10% by next Friday, citing staffing shortages and safety risks caused by the shutdown. United Airlines plans to cancel about 510 flights between today and Sunday, while Delta, American and Southwest will each remove hundreds more over the coming days. The cuts exclude international routes but coincide with a ban on commercial space launches during certain hours starting Monday. Lawmakers are demanding transparency over the FAA’s decision, as the disruption threatens to worsen ahead of Thanksgiving. S&P Mini +0.207% to 6888.25, DXY +0.108% to 99.911, 10y UST +0.2bp to 4.079%.

According to Reuters, China has begun designing a new rare earth licensing regime that could accelerate shipments, though industry sources say it is unlikely to represent a full rollback of restrictions as anticipated by Washington. The Ministry of Commerce has reportedly informed some rare earth exporters that they will be able to apply for streamlined permits under the forthcoming system and has outlined the necessary documentation in recent industry briefings. After the recent summit between U.S. and Chinese leaders, China agreed to suspend rare earth controls announced in October for one year and to purchase more U.S. agricultural goods. CSI 300 +0.274% to 4653.4, USDCNY +0.03% to 7.1215, 10y CGB -0.5bp to 1.792%.

The Dutch government is reportedly prepared to suspend its order granting it authority to block or alter key corporate decisions at a key semiconductor producer if China resumes exports of critical chips, Bloomberg reported. The suspension could occur as early as next week, pending verification of resumed shipments. A shortage of the company’s chips amid a dispute with China over ownership and control has disrupted automotive supply chains, reduced production and led to staff furloughs. The chips are widely used in industrial, computing, mobile and consumer products. Dutch Economy Minister Vincent Karremans said he expects shipments from the producer to reach customers in Europe and globally within days. AEX +0.46% to 975.93, EURUSD -0.191% to 1.1515, 10y NGB +0.3bp to 2.786%.

South Korea and the U.S. have yet to release their joint fact sheet following the October 29 summit between Presidents Lee Jae Myung and Donald Trump, reportedly due to extended coordination among U.S. agencies. The document, initially expected within days, is set to detail Seoul’s $350bn investment pledge in exchange for a U.S. tariff reduction to 15%, as well as security commitments including U.S. support for South Korea’s pursuit of nuclear-powered submarines. Foreign Minister Cho Hyun confirmed that the U.S. State Department requested more time for internal approvals, while Defense Minister Ahn Gyu-back cited the need for interagency coordination. The delay has also postponed the release of results from recent bilateral security talks in Washington. KOSPI +2.784% to 4221.87, USDKRW +0.032% to 1430.45, 10y KTB +0.3bp to 3.058%.

U.S. preliminary November University of Michigan consumer sentiment forecast to ease to 53 from 53.6, while 1y and 5-10y inflation expectations are expected at 4.6% and 3.8% from 4.6% and 3.9% in October, respectively.

Central bank speakers: Fed Vice Chair Philip Jefferson speaks on AI and the economy; Fed Governor Stephen Miran speaks on stablecoins and monetary policy at the Harvard Club of New York.

Mood: iFlow Mood has normalized slightly, driven by greater selling pressure in core sovereign bonds compared with equity markets. iFlow Mood is at -0.036.

FX: USD and KRW posted strong inflows, against outflows observed in EUR, NZD, PHP, CAD, THB and MXN. Elsewhere, the overall flow bias is on the sell side, including CNY, GBP and JPY vs. light buying in AUD and IDR.

FI: Good-sized cross-border outflows in U.S. Treasurys have continued, followed by light cross-border selling in U.K. gilts and Eurozone government bonds. Elsewhere, notable flows included selling in Chilean, Turkish and Indonesian government bonds, against buying in Colombian and Thai government bonds.

Equities: EM Americas was the only region that posted inflows; outflows elsewhere were led by DM Americas and DM APAC. U.S, U.K and South Korean equities were significantly sold, against large buying in Brazil. Within EM Americas, the financials and utilities sectors posted inflows, against selling in the communication services and material sectors.

“The wavering mind is but a base possession” – Euripides

“No man is able to make progress when he is wavering between opposite things.” – Epictetus

Germany’s September exports rose 1.4% m/m and 2.0% y/y to €131.1bn, while imports increased by 3.1% m/m and 4.8% y/y to €115.9bn. This resulted in a seasonally adjusted trade surplus of €15.3bn, down from €16.9bn in August. Exports to EU countries totaled €74.3bn (+2.5% m/m), with euro area exports up 1.4% and those to non-euro EU states up 5.1%. Exports to non-EU countries were stable at €56.8bn, while imports from these countries climbed 5.2%. Exports to the U.S. rose 11.9% m/m to €12.2bn but fell 14.0% y/y, whereas exports to China declined by 2.2%. Imports from China reached €14.6bn (+6.1% m/m) and those from the U.S. €8.7bn (+9.0% m/m). DAX +0.779% to 24144.85, EURUSD -0.191% to 1.1515, 10y Bund +0.4bp to 2.637%.

France’s Q3 trade deficit (FOB/FOB) narrowed by €4.5bn from Q2 to €17.4bn. Exports rose 4.1% q/q to €155.7bn, driven by strong deliveries of aeronautical products and, to a lesser extent, electricity and refined petroleum products, while imports increased 0.9% to €173.1bn, mainly due to higher pharmaceutical and electronic goods purchases. The transport equipment balance improved sharply after a previous decline, and the energy deficit narrowed for the second consecutive quarter. The agricultural balance turned positive for the first time since Q2 2024. France’s trade position improved significantly with non-EU countries, particularly in Asia, Africa and the Middle East, where the surplus reached a record level. CAC40 +0.211% to 8138.18, EURUSD -0.191% to 1.1515, 10y OAT -0.2bp to 3.419%.

France’s Q3 private sector basic hourly wage index (SHBOE) rose 0.4% q/q and 2.1% y/y, maintaining the same annual pace as in Q2. For firms with ten or more employees, the SHBOE increased 0.2% q/q and 2.0% y/y, with a 0.3% rise in services and 0.2% in both industry and construction. The basic monthly wage index (SMB) rose 0.3% q/q and 2.0% y/y. With consumer prices up 1.1% y/y, real SHBOE and SMB grew 0.9%. By sector, real SMB rose 1.0% in industry and 0.8% in construction and services. Across job categories, real wages increased between 0.8% and 0.9%, confirming moderate real income growth in Q3 2025.

The Netherlands’ household spending on goods and services rose 0.8% y/y in September. Consumers spent 1.2% y/y more on services in September, with the increases mainly coming in transport and communication, and recreation and culture. Spending on services accounted for over half of total domestic consumer expenditure. Households spent 0.2% y/y more on durable goods, mainly on electrical appliances and clothing. Spending on food, beverages and tobacco was down by -0.3% y/y. Households spent 0.4% on other goods. AEX +0.46% to 975.93, EURUSD -0.191% to 1.1515, 10y NGB +0.3bp to 2.786%.

U.K. house prices rose 0.6% m/m (£1,647) in October, according to Halifax. This marked the largest monthly gain since January, lifting the average property value to a record £299,862, Annual growth strengthened to 1.9% from 1.3%. Halifax reported that buyer demand remained firm coming into autumn, with mortgage approvals reaching their highest level this year. However, affordability pressures persist, as average fixed mortgage rates hover near 4% and household budgets remain constrained by higher living costs. Many buyers are opting for smaller deposits and longer mortgage terms. Halifax noted that with property prices rising more slowly than incomes for nearly three years, affordability has been gradually improving and is expected to continue doing so. FTSE 100 +0.232% to 9739.78, GBPUSD -0.221% to 1.3123, 10y gilt -0.9bp to 4.4%.

Switzerland’s October consumer sentiment index declined slightly to -36.9 from -36.5 in September, remaining near historically low levels. The index came in 0.1 points higher than a year earlier but well above its 2025 low of -42.4 in April, recorded shortly after global tariff tensions intensified. Following a mid-year recovery to -32.8 in July, sentiment weakened sharply again in August to -39.9. The survey by the State Secretariat for Economic Affairs (SECO), which has been conducted monthly since 1972, reflects household perceptions of the economy and personal finances rather than business conditions, highlighting persistently subdued consumer confidence coming into autumn. SMI +0.352% to 12277.52, EURCHF +0.041% to 0.92868, 10y Swiss GB -0.4bp to 0.13%.

Sweden’s October housing data showed condominium prices rising 1.7% m/m while detached house prices decreased by 0.7% m/m, leaving overall prices flat y/y. Condominium prices increased by more than 3% in Greater Stockholm, supported by higher sales in the city center, where prices were up 1%. Meanwhile, prices fell by nearly 2% in Greater Malmö and about 1% in Greater Gothenburg. Detached house prices were broadly unchanged in Stockholm and Gothenburg but decreased by 0.5% in Malmö and 1% outside major cities. Nationally, 16,500 homes were sold in October, down 4% y/y, including 10,600 condominiums (-5%) and 5,900 houses (-2%), though total sales from January to October rose 3% y/y to 143,600. OMX +0.196% to 2772.502, EURSEK -0.096% to 10.9384, 10y Swedish GB 0bp to 2.625%.

Sweden’s central government debt totaled SEK 1,140.6bn at the end of October 2025, an increase of SEK 37.1bn from the previous month. Including on-lending and assets under management, the debt stood at SEK 1,106.3bn, up SEK 15.4bn m/m. Government bonds represented the largest share at SEK 614.9bn, followed by inflation-linked bonds at SEK 212.3bn and treasury bills at SEK 182.8bn. The average time to refixing stood at 4.83 years, within the 3.5-6-year target range. Foreign currency debt was SEK 41.6bn, with exposure continuing to decline ahead of the 2027 phase-out. The debt-to-GDP ratio remained below 40%, indicating stable fiscal conditions.

Norway’s September industrial production rose 3.4% m/m and 20.6% y/y, driven by a 4.5% m/m and 24.4% y/y increase in extraction and related services, while manufacturing output declined 1.7% m/m but rose 2.6% y/y. Within manufacturing, machinery and equipment output grew 1.0% m/m and 8.3% y/y, while refined petroleum, chemical and pharmaceutical products fell 9.7% m/m but edged up 0.7% y/y. Electricity, gas and steam output increased 1.2% m/m but was 0.3% lower y/y. Industrial turnover decreased 0.6% m/m but was up 3.3% y/y at NOK 227.3bn, with extraction nearly flat at 0.1% m/m and manufacturing turnover down 1.1% m/m but up 3.8% y/y. In other figures, Norwegian earnings increased by 0.1% m/m in September. OSE +0.584% to 1621.21, EURNOK -0.246% to 11.6528, 10y NGB +0.4bp to 4.026%.

Czech September retail sales rose 2.6% y/y in real terms but fell 0.2% m/m. Excluding motor vehicles, sales decreased by 0.2% m/m, with food sales down 0.5%, non-food goods down 0.1% and automotive fuel up 0.5%. On a y/y basis, automotive fuel sales grew by 9.5%, and non-food goods by 2.8%, while food sales shrank by 0.2%. The strongest annual increases were in cosmetic and toilet articles (+11.6%), dispensing chemists (+3.1%) and cultural and recreation goods (+2.6%), while sales of information and communication equipment fell 3.4%. Online sales rose 4.2% y/y. Motor vehicle sales, including parts, grew by 3.5% y/y and repairs by 2.3%, though total vehicle trade was down 0.4% m/m. Prague SE +0.354% to 2405.08, EURCZK -0.095% to 24.34, 10y CZGB +1.1bp to 4.509%.

Japan’s September household survey showed average monthly consumption expenditure by two-or-more-person households at ¥303,214, up 5.3% y/y in nominal terms and 1.8% y/y in real terms. Spending rose most sharply for transportation and communication (up 14.8% nominal, 11.5% real) and medical care (up 12.4% nominal, 11.1% real), while clothing and footwear fell 5.1% in nominal terms and 7.4% in real terms. Working households recorded average monthly income of ¥510,935, up 3.4% in nominal terms and flat in real terms. Disposable income rose 2.8% y/y, while consumption expenditure increased 10.2% in nominal terms and 6.6% in real terms, with average propensity to consume at 82.1%, up from 76.6% a year earlier. Nikkei -1.194% to 50276.37, USDJPY +0.189% to 153.46, 10y JGB -0.4bp to 1.681%.

Chinese exports unexpectedly fell -1.1% y/y in October (September: 8.3%), the first year-on-year fall since March 2024. Imports eased to 1.0% y/y from 7.4% y/y, leaving a trade surplus of $90.07bn vs. $90.45bn in September. In YTD y/y terms, export growth is 5.3% (September: 6.1%), with imports -0.9% (-1.1% YTD y/y). Exports were lower to the U.S. (-25.1% y/y), Japan (-5.7% y/y), South Korea (-12.5%) and Russia (-22.5%), while exports were up 11.1% y/y to ASEAN, 1% y/y to the EU and 21.3% to Hong Kong. Overall, ASEAN countries accounted for 17.5% of total Chinese exports, followed by the U.S. (11.4%), the EU (14.4%) and LatAm (7.9%). CSI 300 -0.311% to 4678.79, USDCNY -0.041% to 7.1222, 10y CGB +0.3bp to 1.809%.

Philippines Q3 GDP fell more than expected to 0.4% q/q, 4.0% y/y from 1.5% q/q, 5.5% y/y in Q2 2025. Quarterly GDP growth of 4% y/y is the slowest since Q1 2021 (-3.8% y/y). Key sector contributors included wholesale and retail trade (5.0% y/y), financial and insurance activities (5.5% y/y) and professional and business services (6.2% y/y). All major sectors recorded growth: agriculture, forestry and fishing rose by -2.9% q/q, 2.8% y/y, industry by 0.1% q/q, 0.7% y/y and services by 0.9% q/q, 5.5% y/y. On the demand side, household final consumption expenditure grew 4.1% y/y, government final consumption expenditure rose 5.8% y/y, exports of goods and services increased 7.0% y/y and imports grew 2.6% y/y. However, gross capital formation declined by 2.8% y/y. Gross national income expanded by 5.6% y/y, supported by a 16.9% increase in net primary income from the rest of the world. PSEi -1.306% to 5759.37, USDPHP -0.114% to 59.04, 10y PHGB -6.2bp to 5.785%.

Malaysia September industrial production rose 5.7% y/y from 4.8% in August. Growth was driven by the mining sector at 10.2% y/y (August: 16.8%) and manufacturing at 5.0% y/y (August: 2.8%), while electricity rose 2.8% y/y (August: 1.2%). Month-on-month, industrial production contracted slightly by 0.02%, after a 2.4% increase in August. Within manufacturing, domestic-oriented industries grew 5.3% y/y (August: 3.8%), led by food processing (9.0%), basic metals (6.1%) and fabricated metal products (4.5%). Export-oriented industries rose 4.8% y/y (August: 2.3%), supported by computer, electronic and optical products (8.8%) and vegetable and animal oils and fats (7.4%). On a m/m basis, domestic-oriented and export-oriented industries grew 1.5% and 0.8%, respectively. Mining growth was mainly attributable to crude oil and condensate production increasing by 13.0% y/y (August: 11.4%), with natural gas up 8.5% y/y. Electricity output rose 2.8% y/y (August: 1.2%). KLCI +0.012% to 1619.13, USDMYR +0.12% to 4.178, 10y MGB +1bp to 3.513%.

Malaysia September manufacturing sales grew by 4.3% y/y from 2.7% y/y to MYR 169.3bn, rising 0.6% m/m (August: 0.0%). Growth was led by food, beverages and tobacco (9.1% y/y vs. 3.7% in August), and non-metallic mineral products, basic metal and fabricated metal products (2.7% y/y vs. 3.3% in August). Export-oriented industries, comprising 72.3% of total sales, expanded 3.8% y/y (August: 2.0%), driven by vegetable and animal oils and fats (7.8%), computer, electronics and optical products (6.1%) and machinery and equipment (5.2%). Employment in manufacturing increased by 1.0% y/y to 2.4 million, with a 0.5% m/m rise. Salaries and wages grew 2.0% y/y to MYR 8.4bn, up 1.7% m/m. Sales per employee reached MYR 70,126 (+3.3%), and average wages per employee rose 1.1% y/y to MYR 3,479. KLCI +0.012% to 1619.13, USDMYR +0.12% to 4.178, 10y MGB +1bp to 3.513%.

Taiwan’s October exports surged 49.7% y/y to US$61.8bn, while imports grew 14.6% to US$39.2bn, producing a trade surplus of US$22.6bn. Export growth was led by information, communication and audio-video products (+138.2%), electronic parts (+27.7%) and machinery (+7.7%), partly offset by an 11.6% fall for base metals. Imports rose mainly because of higher purchases of electronic parts (+22.4%), ICT products (+90.0%) and machinery (+17.1%), while mineral and chemical imports fell 12.0% and 6.9%. Exports rose by 144.3% to the U.S., by 40.0% to ASEAN and 26.2% to Europe, while those destined for China and Hong Kong increased by 3.2%. Imports rose 21.8% from ASEAN and 12.1% from South Korea, while imports from Europe were down 8.1%. TAIEX -0.889% to 27651.41, USDTWD -0.306% to 31.045, 10y TGB -1.1bp to 1.27%.