Do Surging Margins and Steady Inflation Signal Rotation Risk?

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

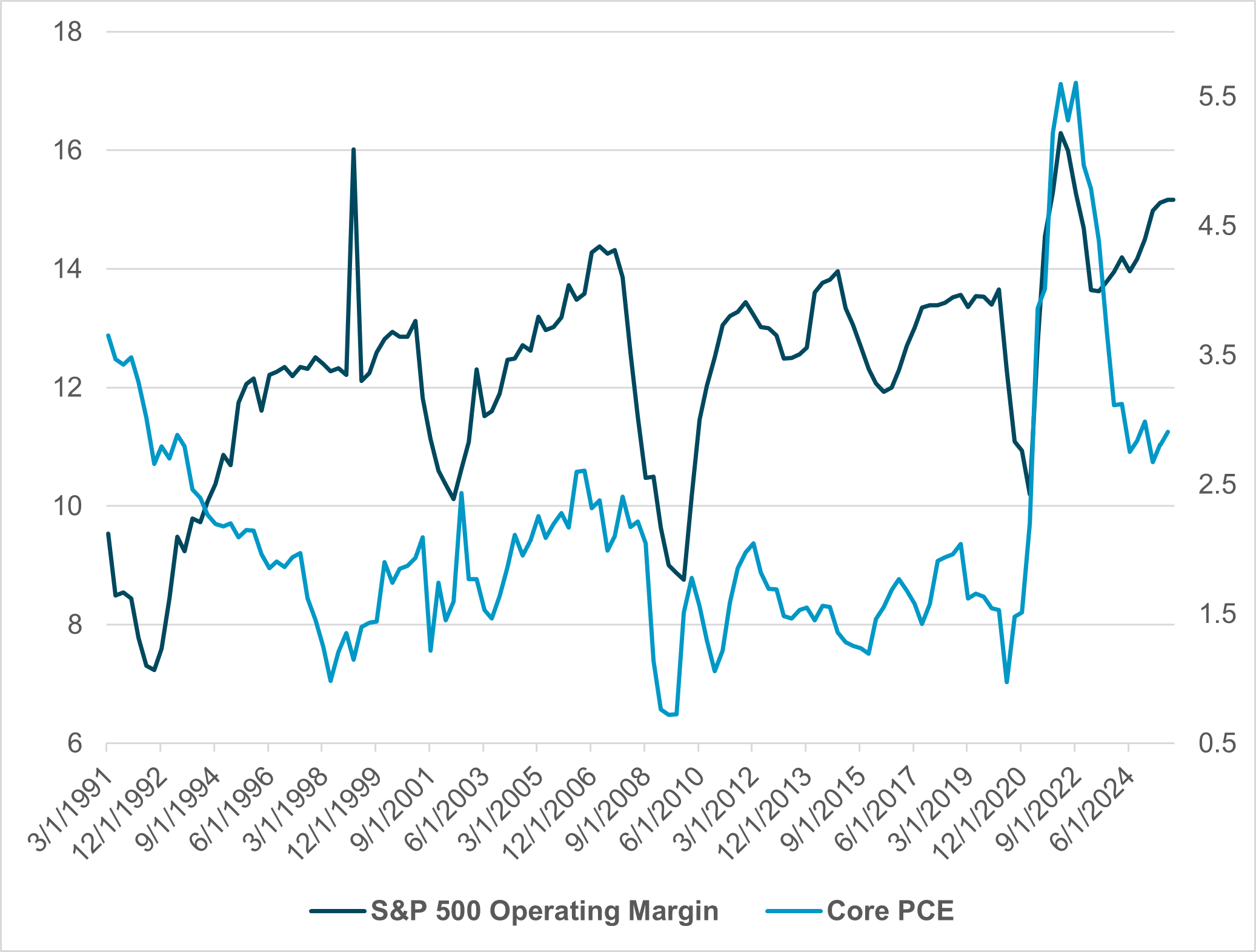

EXHIBIT #1: S&P 500 OPERATING MARGIN VS. U.S. CORE PCE PRICES

Source: BNY, Bloomberg

U.S. Q3 earnings have entered the macro discussion amid the lack of official government data on growth and inflation. The focus on inflation as a potential brake on sustained 2026 easing has been repriced, with Fed speakers and private data pointing to sustained growth. Corporate margins have also played a key role in rethinking the interest rate path. The data show a few key trends: companies in import-dependent businesses are struggling, those using AI for productivity see gains, and foreign-linked revenues trade at a premium. Markets are watching for the usual year-end rush for asset appreciation, linked to available cash and tax mechanics.

Our take

Net margins, defined as operating income divided by revenue, have trended higher, which helped explain the ongoing equity bull market. S&P 500 margins increased from 12.2% in Q3 2024 to 12.9% in Q3 2025. Higher operating margins often correlate with higher valuations, as they reflect improved productivity.

Technology has led this trend for the last two years. The sector also led earnings, though this quarter’s earnings surprises also came from Consumer Discretionary and Financials. Share appreciation has driven current valuation concerns, as price gains of over 40% from April lows outpace the current 10.6% blended Q3 earnings growth. This week, corrections around stretched valuations reflect a rethinking of Fed cuts ahead, along with doubts that growth or margins can sustain.

Forward look

The relationship between margins and price pressures has been uneven over the past 40 years. Stable interest rates and modest growth made the 2010 to 2019 period in equities stand out. Notably, S&P 500 volatility averaged 21% during that period of margin stability and modest inflation, with four significant sell-offs. The history of blow-off-top asset prices and underlying inflation is not a good guide for predicting extended corrections or managing risk.

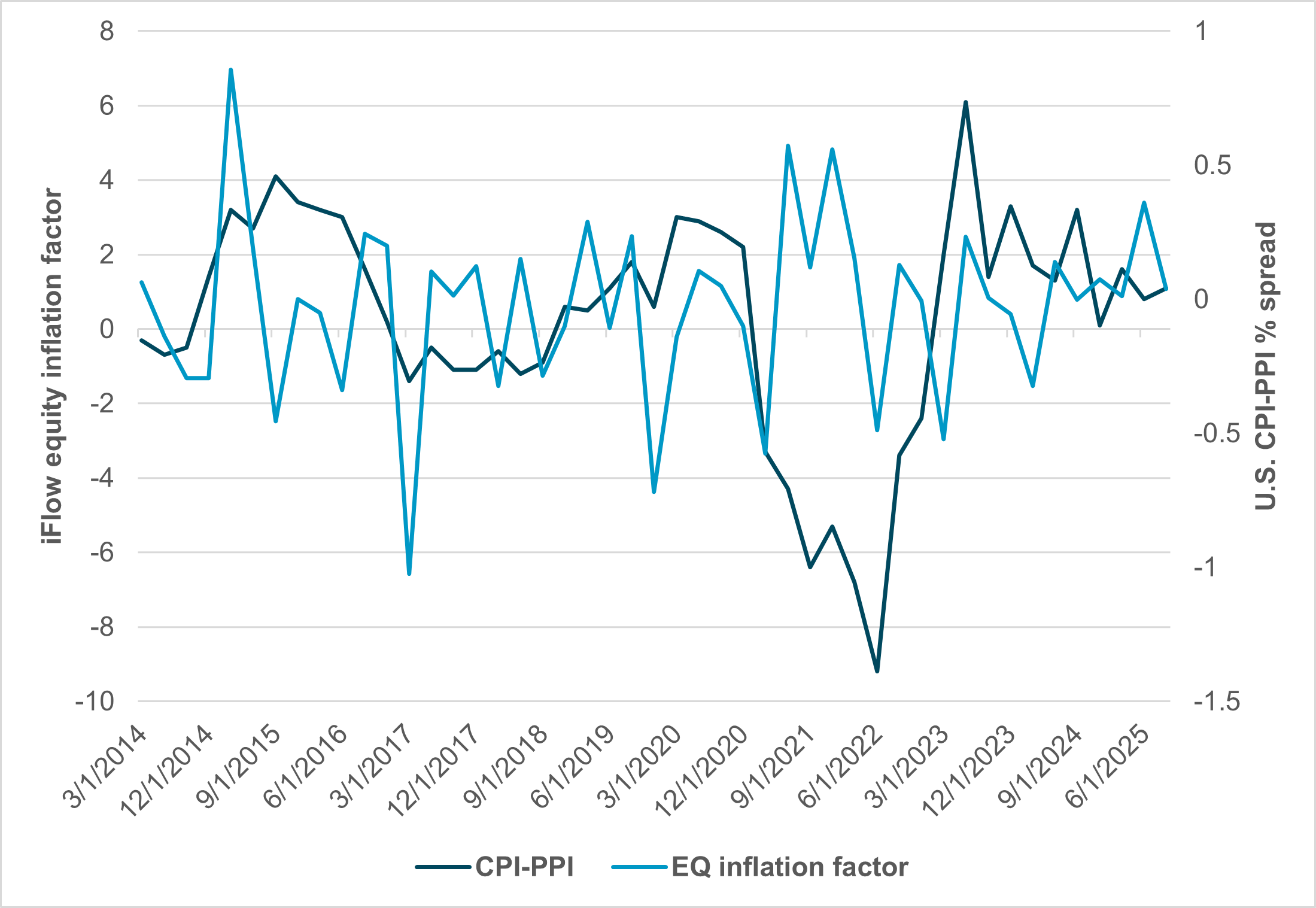

EXHIBIT #2: U.S. CPI-PPI VS. IFLOW U.S. EQUITY INFLATION FACTOR FLOWS

Source: BNY, Bloomberg

Our take

There has been a notable lack of inflation surprises in 2025. Investor flows this year have been tightly correlated to inflation. One surprise Q3 result — margins rising despite core inflation — has helped market sentiment. Inflation has mattered less than other factors, but as 2022 showed, that can change. The Consumer Price Index (CPI) minus the Producer Price Index (PPI) has served as a quick way to measure corporate margins. This gauge has broken down since October amid the government shutdown and the lack of official economic data. Reverse logic now supports the narrative that inflation is under control. Whether this proves true for December’s Federal Open Market Committee (FOMC) decision depends on financial conditions. If stocks rally further, prompting consumers to spend on wealth-effect optimism, more easing may not be needed, or helpful, for price stability.

Forward look

Financial conditions affect how policy transmissions work with home equity and 401(k) stock gains playing a key role in how domestic demand drives growth. With the rise of private credit and equity, confidence in monetary aggregates has diminished and using M1 (pure cash) or M2 (cash plus savings) to measure inflation has been less useful in tracking price pressures. For example, U.S. M2 grew 4.5% in Q3, touching $22.2tn, below the 6.3% 25-year average and below the 5.1% nominal GDP growth rate in 2025.

Companies with access to non-bank finance stand out, as leverage and inflation factors are significantly correlated. The Oct. 31 cash squeeze matters in this context and contrasts with the recent focus on gold and Bitcoin as safe-haven cash alternatives. Post-Covid U.S. deficit spending has also become a bigger focus for investors, with budgets seen as limiting factors for inflation risks and corporate margins. For November and the rest of the year, cash squeezes from the government shutdown, expectations of a catch-up infusion after the government reopens, and typical year-end liquidity needs are expected to help consumer-facing U.S. equity sectors.

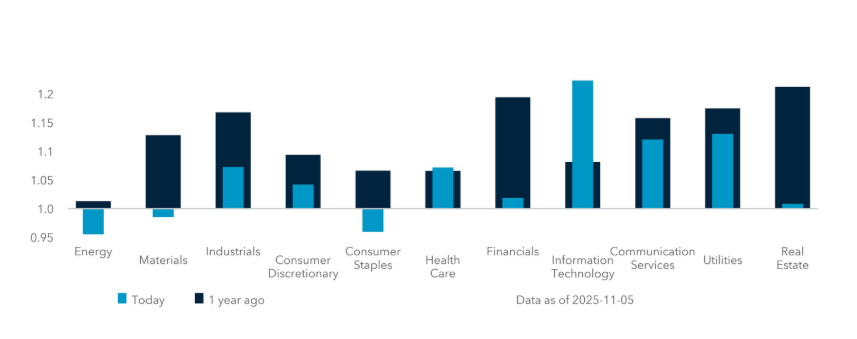

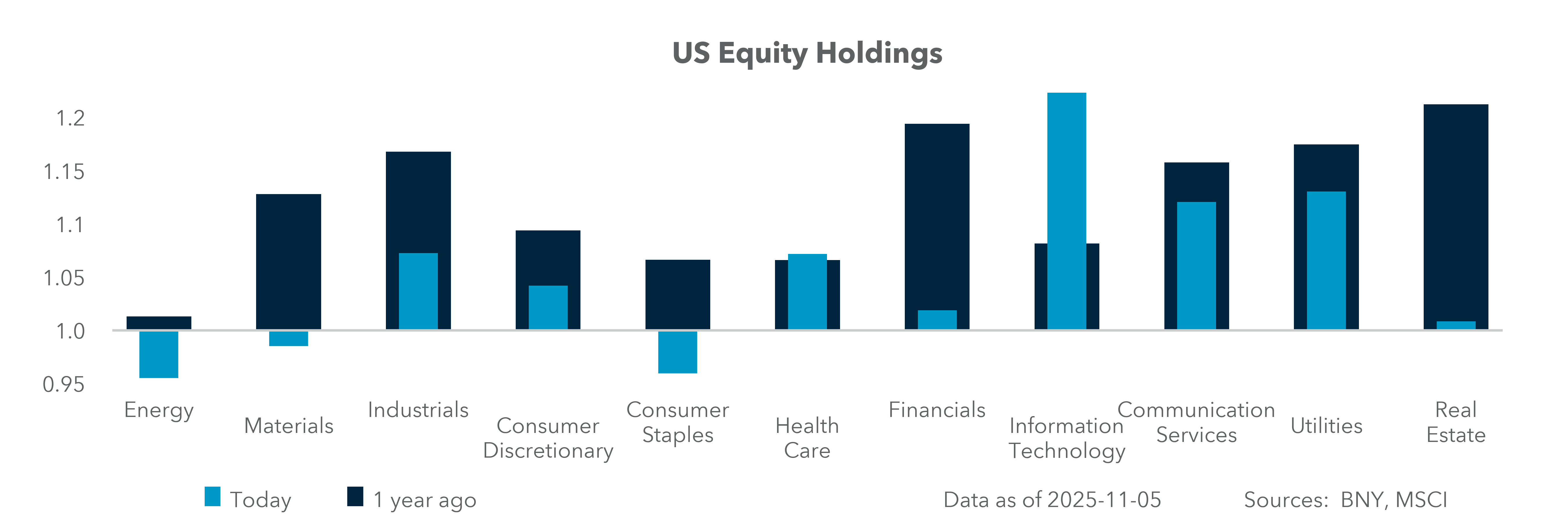

EXHIBIT #3: U.S. IFLOW EQUITY HOLDINGS BY SECTOR

Source: BNY

Our take

Over the past three weeks, the U.S. financial sector has seen a significant reduction in holdings. The market was initially worried about sub-prime auto loan exposure, alongside concerns over net interest income linked to future Fed policy. There are also concerns about deposit pressure from cash equivalents like U.S. Treasury bills. Non-bank financial institutions and stable coins add another layer to how Information Technology (IT) and Financials are competing. Bitcoin’s correlation of with IT equity performance has been a notable theme over the past month.

Forward look

A larger U.S. stock market rotation may be underway. Valuations in the IT sector are stretched but seen as justified given strong margins and earnings growth. The top 10 companies in the S&P 500 now represent 40% of total market capitalization, suggesting significant concentration risks. Investors are overweight IT and underweight Financials. In past bubbles, 1999 centered on Technology, while 2008 centered on Financials. Expectations for rates and growth are at odds with current portfolio positioning. Risk that the Fed delivers less, inflation remains sticky, or growth proves stronger may drive a Q4 broadening of risk across other sectors.

As 2025 winds down, U.S. equity markets face a crossroads between strong corporate margins and concerns about sustained policy support. The balance between price stability and asset inflation will guide both monetary decisions and portfolio positioning. Investors should monitor financial conditions, liquidity dynamics and sector rotation, particularly shifts away from IT toward Financials and Consumer sectors. Stable but elevated valuations favor a selective approach, emphasizing margin-resilient, globally linked firms, as markets navigate year-end liquidity pressures and potential recalibration of rate-cut expectations in early 2026.